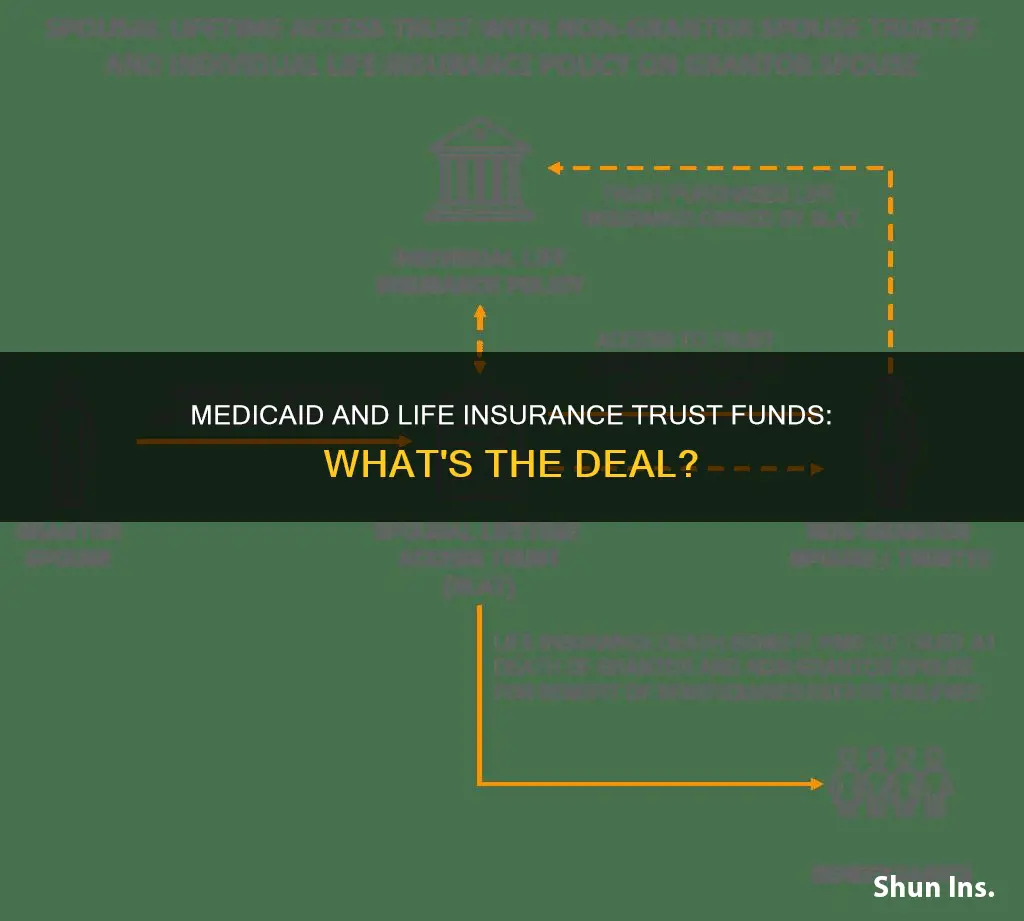

Life insurance policies can impact Medicaid eligibility. While term life insurance is automatically exempt, whole life insurance is only exempt if the total face value of all combined policies is not more than $1,500. Medicaid cannot take one's life insurance policy while they are still alive, but based on the face value of the policy, the cash surrender value may be counted towards Medicaid's asset limit, rendering one ineligible for Medicaid. Medicaid Asset Protection Trusts (MAPT) are a way to protect assets from being counted for Medicaid eligibility. MAPTs are irrevocable trusts, meaning that once any assets are placed in the trust, the grantor loses control of the assets.

| Characteristics | Values |

|---|---|

| Medicaid Asset Protection Trusts (MAPT) | Enable someone who would otherwise be ineligible for Medicaid to become eligible and receive the long-term care they require |

| MAPT | Must be created at least five years before needing long-term care to avoid the Medicaid look-back period |

| MAPT | Must not include the trustmaker as a beneficiary |

| MAPT | Must be irrevocable, i.e., once any assets are placed in the trust, the grantor loses control of the assets |

| Life insurance policies | May impact one’s eligibility for Medicaid depending on the type of policy and the value |

| Whole life insurance policies | Exempt if the face value of all policies is under a state-specific value |

| Term life insurance | Automatically exempt |

| Whole life insurance | Exempt if the total face value of all combined policies is not more than $1,500 |

| Medicaid | Cannot take one’s life insurance policy while they are still living |

| Medicaid | May take the proceeds of the death benefit to recover costs it paid for one’s long-term care |

Explore related products

What You'll Learn

![]()

Medicaid eligibility and life insurance policies

Life insurance policies can impact Medicaid eligibility, depending on the type of policy and its value. Medicaid is designed for low-income Americans, and its eligibility requirements include strict income and asset limits.

Term life insurance, which covers a limited period, typically between 10 and 30 years, does not impact Medicaid eligibility. It is not counted towards the asset limit because it does not accumulate a cash value and cannot be cashed out while the policyholder is alive. Whole life insurance, on the other hand, can impact eligibility. This type of permanent life insurance includes an investment component that gives it a cash value, which may be considered an asset under Medicaid guidelines. Burial insurance, a type of whole life insurance that covers burial or cremation costs, does not impact eligibility as it is exempt from the asset limit.

The asset limit for Medicaid varies by state, but generally, for single applicants, it is $2,000, although this can vary from \$1,600 in Connecticut to $32,396 in New York. If the total value of an elder's life insurance policies exceeds $1,500, they may need to devise a spend-down strategy. One option is to transfer ownership of the policy to a family member, but this may trigger a penalty period. Another option is to set up an irrevocable trust, where a designated trustee controls the assets, and they are not counted as part of the estate. However, this can be a risky venture, as the trustee may spend the funds for their own gain, and there is no legal recourse.

Life Insurance: Can It Cover a Spouse's Medical Bills?

You may want to see also

Explore related products

![]()

Medicaid Asset Protection Trusts (MAPT)

Various assets can be put into a MAPT, including one's home, real estate, checking and savings accounts, stocks and bonds, mutual funds, and CDs. Retirement accounts (401ks and IRAs) are generally not recommended due to tax implications. If income-producing assets are placed in the trust, the trustmaker can collect the income while the principal remains protected. The trustmaker can also continue to live in their home and even sell it for the trust to purchase another one. However, in Michigan, a home is considered a countable asset when placed in a MAPT.

The individual who creates the MAPT is called a grantor, trustmaker, or settlor. There is also a trustee, who manages the trust and controls the assets within it. The trustee must be someone other than the trustmaker or their spouse, such as an adult child or another relative. The trustee must follow specific rules regarding how trust funds can be used and should not use the funds for themselves. A beneficiary is also named and will benefit from the trust after the trustmaker passes away. For the trust to be Medicaid-exempt, the beneficiary cannot be the trustmaker.

MAPTs are not suitable for those needing Medicaid immediately or within a short period. In most states, the MAPT needs to be created at least five years before needing long-term care to avoid the Medicaid look-back period. After this five-year period, as long as the trust owns the assets, Medicaid cannot count them, and they cannot be seized to reimburse long-term costs.

While MAPTs offer protection, there are some potential downsides. Creating a MAPT involves relinquishing ownership and control of assets, and there is a risk that the trustee may spend the funds for their own gain. Additionally, income generated from the trust may cause the trustmaker to exceed the state's income limit.

Grandparents and Medical Insurance: Deducting Premiums

You may want to see also

Explore related products

![]()

Irrevocable trusts and long-term financial plans

Trusts are commonly used for wealth planning, and irrevocable trusts can be a valuable tool for long-term financial planning. An irrevocable trust is a legal entity created by a grantor to hold some of their assets during their lifetime. The grantor gives up certain rights to the trust, and a designated trustee manages the trust and its assets. Irrevocable trusts can hold real property, such as a home, bank accounts, and other investment vehicles.

One of the main benefits of an irrevocable trust is that it can protect assets from creditors and lawsuits. This type of trust can also reduce the value of the grantor's estate, minimising estate taxes. In the context of Medicaid planning, an irrevocable trust can protect assets from being counted for eligibility purposes. This is because assets in an irrevocable trust are no longer considered owned by the grantor but by the trust itself.

Additionally, irrevocable trusts can be useful for long-term care planning. They can help individuals become eligible for Medicaid and receive the necessary care, either at home or in a nursing home. However, it is important to note that there are potential downsides to creating an irrevocable trust, such as the risk of the trustee spending funds for their own gain and the loss of direct access to the trust principal.

When considering an irrevocable trust as part of long-term financial planning, it is essential to understand the tax implications. While irrevocable trust distributions can be completely tax-free, they may also be taxable at the highest marginal tax rates or even higher. In the case of an irrevocable grantor trust, the grantor is responsible for paying income taxes on the trust's income, rather than using the trust's assets. This additional expense should be carefully considered and planned for.

In conclusion, irrevocable trusts can be a powerful tool for long-term financial planning, offering asset protection, tax advantages, and eligibility for Medicaid. However, it is crucial to carefully weigh the benefits against the potential drawbacks and to seek professional advice to ensure the trust aligns with one's financial goals and expectations.

Cleveland Clinic's Accepted Insurance Plans: What You Need to Know

You may want to see also

Explore related products

![]()

Medicaid recovery and countable assets

To qualify for Medicaid, applicants must pass strict tests on the amount of assets they can keep. These assets are divided into two categories: exempt and non-exempt (or countable) assets. Exempt assets are those that Medicaid does not take into account when determining eligibility, while non-exempt assets are counted towards Medicaid's asset limit. Generally, exempt assets include an individual's residence, personal belongings, household goods, one essential vehicle, burial spaces, a burial fund, and certain types of life insurance policies.

Countable assets, on the other hand, are all money and property, as well as any item that can be valued and turned into cash, such as cash, savings and checking accounts, stocks, bonds, and real estate other than the primary residence. To meet Medicaid's asset limit, individuals can consider strategies such as "spending down" countable assets on exempt ones or utilising trusts. Trusts, specifically irrevocable trusts, can be used to protect assets from Medicaid recovery and enable individuals who would otherwise be ineligible for Medicaid to become eligible.

Medicaid Asset Protection Trusts (MAPTs) are a type of irrevocable trust that allows individuals to protect their assets from being counted for eligibility purposes. In a MAPT, the assets are no longer considered owned by the individual, and they can continue to live in their home even if it is placed in the trust. However, it is important to note that not all trusts are created equally, and certain trusts, such as revocable trusts, may be considered countable assets by Medicaid. Additionally, there are risks associated with MAPTs, including the potential for the trustee to spend funds for their own gain and the lengthy timeframes required to become eligible for Medicaid coverage.

Upon an individual's death, Medicaid may seek to recover funds paid on their behalf, even going after assets that were not initially countable. However, states cannot recover from the estate if the deceased is survived by a spouse, a child under 21, or a blind or disabled child of any age. Irrevocable trusts can protect assets from Medicaid estate recovery, as assets in such trusts are not owned by the individual and are therefore not part of the probated estate. Overall, while trusts can be a valuable planning strategy, it is recommended to consult with an attorney specialising in elder law and Medicaid estate planning due to the complexity of Medicaid rules.

Geico's Medical Insurance: What You Need to Know

You may want to see also

Explore related products

$12.49 $16.99

![]()

Medicaid planning and long-term care insurance

Medicaid and long-term care insurance are not equal, and it is important to understand the differences between the two. Long-term care insurance is private insurance available to anyone who can afford to pay for it. It covers all or part of nursing home care, home healthcare, and personal or adult day care for individuals aged 65 or older, or with a chronic condition that needs constant care. It offers more flexibility and options than Medicaid, and because you pay for it, there are no income and asset limits.

Medicaid, on the other hand, is primarily state-run, resulting in varying degrees and types of long-term care coverage. While Medicaid covers nursing home care in all states, it does not cover all care facilities, and it may not offer the choices, benefits, and coverage options provided by long-term care insurance. Additionally, there are income and asset limits for Medicaid eligibility, and applicants may need to employ planning strategies to meet the financial criteria.

One such strategy is to turn countable assets into non-countable assets. This can be done through trusts, such as Medicaid Asset Protection Trusts (MAPTs). MAPTs enable someone who would otherwise be ineligible for Medicaid to become eligible by protecting their assets from being counted for eligibility purposes. Assets placed in a MAPT are no longer considered owned by the applicant, and the income generated can be collected by the trustmaker while the principal remains protected. However, it is important to note that MAPTs need to be created at least five years before needing long-term care to avoid the Medicaid look-back period. Additionally, the income generated from a MAPT may cause the recipient to exceed the income limit permitted in their state.

Another option for Medicaid planning is to utilize the Community Spouse Resource Allowance, which allows a greater portion of a couple's assets to be allocated to the non-applicant spouse without impacting the applicant spouse's long-term care Medicaid eligibility. Additionally, certain states offer Home and Community-Based Services through the Regular State Plan Medicaid program, which provides home health care and personal care assistance to eligible individuals.

How to Access Your Medical Insurance Statement

You may want to see also

Frequently asked questions

Yes, you can protect your assets with a trust fund. A Medicaid Asset Protection Trust (MAPT) is a valuable planning strategy to meet Medicaid’s asset limit when an applicant has excess assets. MAPTs enable someone who would otherwise be ineligible for Medicaid to become eligible and receive the long-term care they require.

With a revocable trust, you retain access to your assets and control to change or cancel provisions. Medicaid will consider this a countable asset. An irrevocable trust, on the other hand, is managed by a designated trustee and cannot be altered by the grantor. Irrevocable trusts are not considered countable assets.

Yes, you can use a life insurance policy as a trust fund. However, the type of policy and its value may impact your eligibility for Medicaid. Term life insurance is automatically exempt, while whole life insurance is only exempt if the total face value of all combined policies is not more than $1,500.

Medicaid cannot take your life insurance policy while you are still living. However, if you are a Medicaid recipient and your estate is the beneficiary of your life insurance policy, Medicaid may take the proceeds of the death benefit to recover costs it paid for your long-term care.