Medicare is a US government health insurance program that offers coverage for people over 65. It is not part of the Health Insurance Marketplace, and those with Medicare coverage do not need to make any changes if they are already enrolled. Medicare works with other insurance plans, such as employer or union coverage, military benefits, or Medicaid, and there is a specific order of payment called coordination of benefits to determine which insurance company pays first. Medicare Supplement Insurance, or Medigap, is an additional insurance option that helps pay for costs that Original Medicare does not cover, such as certain vision, hearing, and dental services. If you have other insurance and are approaching 65, you may need to enroll in Medicare, but this depends on the type of insurance you have.

| Characteristics | Values |

|---|---|

| Medicare coverage | Includes benefits like free preventive benefits, cancer screenings, an annual wellness visit, and more |

| Medicare plans | Include a $2,000 cap on what you pay out-of-pocket for Part D drugs |

| Medicare's annual Open Enrollment Period | October 15 – December 7 |

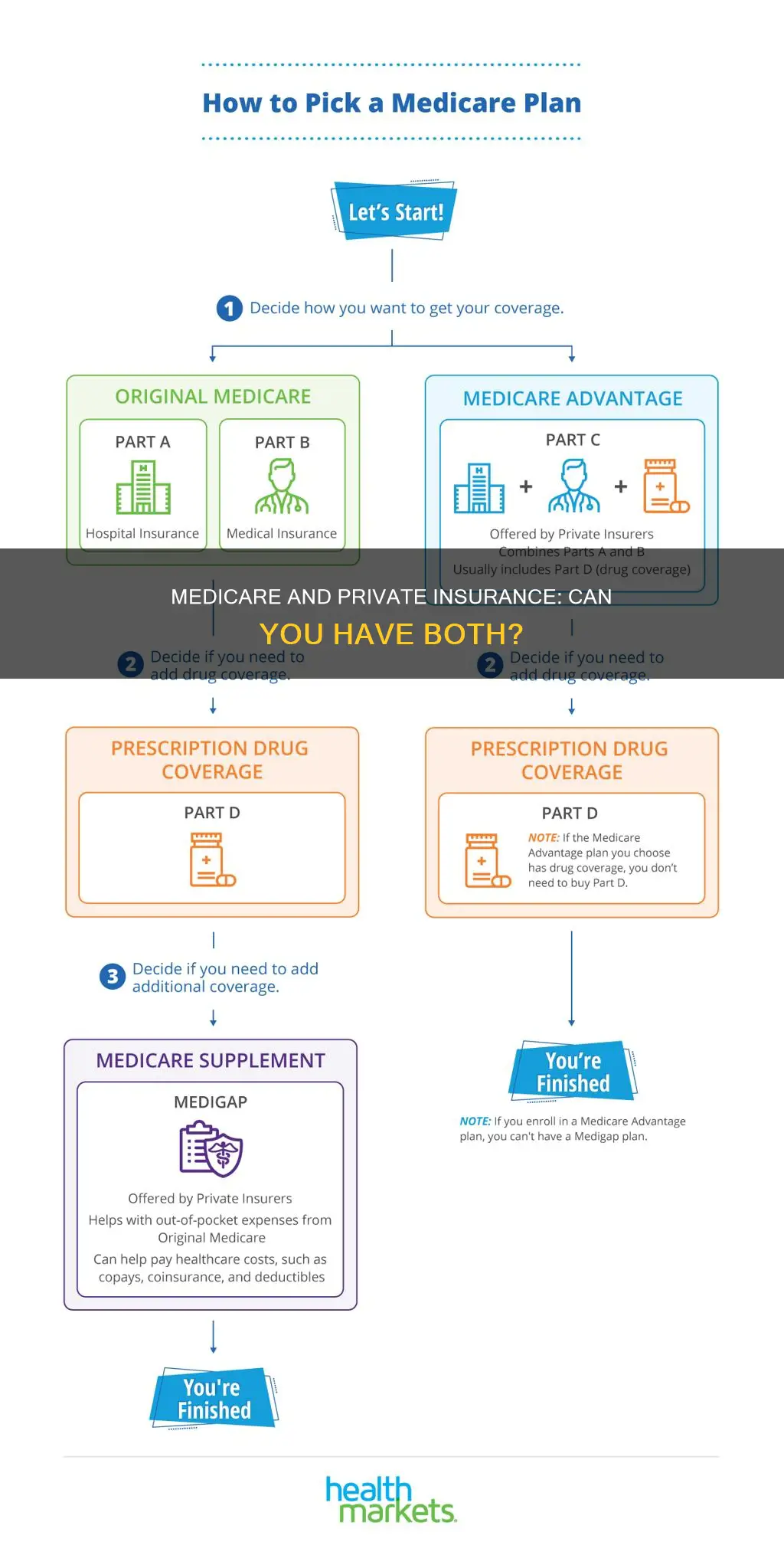

| Medicare Part A | Hospital Insurance |

| Medicare Part B | Medical Insurance |

| Medicare Part D | Drug plan |

| Medicare Advantage | An alternative to Original Medicare for health and drug coverage |

| Medicare Supplement Insurance (Medigap) | Extra insurance to help pay your share of costs in Original Medicare |

| Medicare Secondary Payer rules | Apply to coverage from an employer through the SHOP Marketplace |

| Medicare and other health insurance | Each type of coverage is called a "payer" and follows an order of payment called "coordination of benefits" |

Explore related products

What You'll Learn

![]()

Medicare and other insurance

Medicare is a government-provided health insurance plan that covers free preventive benefits, cancer screenings, an annual wellness visit, and more. Medicare isn't part of the Health Insurance Marketplace, so if you have Medicare coverage, you don't need to do anything. However, if you have other insurance in addition to Medicare, you need to inform your doctor and other healthcare providers. This will help them send your bills to the correct payer and avoid delays.

If you have Medicare and other health insurance, each type of coverage is called a "payer". The "primary payer" pays up to the limits of its coverage and then sends the rest of the balance to the "secondary payer". If the "secondary payer" doesn't cover the remaining balance, you may be responsible for the rest of the costs. This order of payment is called "coordination of benefits". If the insurance company doesn't pay the claim promptly (usually within 120 days), your doctor or other provider may bill Medicare. Medicare may make a conditional payment to pay the bill and then later recover any payments the primary payer should have made.

Medicare Supplement Insurance, or Medigap, is extra insurance you can buy from a private company that helps pay your share of costs in Original Medicare. Generally, you need Part A and Part B to buy a Medigap policy. Some Medigap policies offer coverage when you travel outside the US. Generally, Medigap policies don't cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs. If you're under 65, you might not be able to buy a Medigap policy, or you may have to pay more.

If you have coverage through a Marketplace plan and you turn 65, you should sign up for Medicare and notify your Marketplace plan that you now qualify for Medicare coverage. Your Marketplace coverage will not be canceled automatically when you sign up for Medicare, but if you receive premium tax credits to help pay for your Marketplace plan premium, your eligibility for these tax credits will end when your Medicare Part A coverage begins. If you decide to drop your Marketplace coverage when you become eligible for Medicare, make sure your Medicare coverage has started before you cancel your Marketplace plan to avoid any gaps in coverage.

Dual Coverage: VA Benefits and Private Insurance

You may want to see also

Explore related products

![]()

Medicare and Medicaid

Medicare is a federal insurance program for people aged 65 and above, as well as some people under 65 with certain disabilities or conditions. It is available to anyone who meets the age requirement, regardless of income or health status. Medicare is made up of several parts, including Part A (Hospital Insurance), Part B (Medical Insurance), and Part D (Prescription Drug Coverage).

Medicaid, on the other hand, is a joint federal and state program that provides health coverage for certain individuals and families with low incomes and limited resources. The eligibility requirements and benefits offered by Medicaid vary from state to state. In general, Medicaid covers medical costs for low-income families and children, pregnant women, the elderly, and people with disabilities. It also offers benefits not typically covered by Medicare, such as nursing home care and personal care services.

In some cases, individuals may be eligible for both Medicare and Medicaid, which is referred to as being "'dually eligible." When an individual is dually eligible, Medicare typically pays first for Medicare-covered services, while Medicaid may cover additional costs such as Medicare premiums, deductibles, and co-payments. Additionally, Medicaid may cover certain drugs that are not included in the Medicare drug plan.

To determine eligibility and understand the specific benefits offered, individuals should refer to their state's Medicaid program. For example, in Idaho, there is the Medicare Medicaid Coordinated Plan (MMCP), which combines the services of both programs, and Idaho Medicaid Plus (IMPlus), which provides Medicaid benefits to those enrolled in Medicare.

Asylum Seekers: Accessing Medical Insurance in the USA

You may want to see also

Explore related products

![]()

Medicare and employer-sponsored insurance

Medicare is designed to work alongside employer-sponsored insurance to cover your healthcare needs and help pay for most, if not all, of your medical expenses. If you have both Medicare and employer coverage, you will need to coordinate benefits, which means that either Medicare or the employer plan pays first for covered care. The other insurance is "secondary" and may also pay a portion of the costs. This order of payment is called "coordination of benefits".

If you are still working and have employer insurance when you become eligible for Medicare, you have the option to delay enrolling in Medicare Part B without incurring penalties. However, this only applies if your employer insurance qualifies as "creditable coverage", meaning it provides benefits that are at least as good as those offered by Medicare. If your employer has fewer than 20 employees, you must sign up for Medicare when you're eligible or you may face a late enrollment penalty for Part B when you sign up later. If your employer has 20 or more employees, you can delay signing up without any late enrollment penalties.

Once you retire and give up your employer health benefits, you will have a special enrollment period of eight months to enroll in Part A and B (if you haven’t already). During this period, you can enroll in Medicare Part B without facing late enrollment penalties. To avoid a late enrollment penalty, make sure you apply for Medicare during your Special Enrollment Period.

Before you apply for Medicare, you may have several insurance options. For example, you may be able to drop your employer coverage and enroll in Original Medicare, Part A and Part B. If you choose this option, you might want to consider signing up for prescription drug coverage under Medicare Part D and/or buying a Medicare Supplement Insurance (Medigap) plan. Medigap is extra insurance you can buy from a private company that helps pay your share of costs in Original Medicare. Generally, you need Part A and Part B to buy a Medigap policy.

Medicaid and Medicare: Can I Purchase Both?

You may want to see also

Explore related products

![]()

Medicare and TRICARE

Medicare is a federal health care program for US citizens aged 65 and older, as well as for those under 65 with certain disabilities or end-stage renal disease. TRICARE, on the other hand, is a health care program that serves uniformed service members, retirees, and their families worldwide. It is important to note that these two programs can work together to provide coverage for individuals who are eligible for both.

If you are eligible for both Medicare and TRICARE, it is essential to understand how they interact and coordinate their benefits. TRICARE for Life (TFL) is a specific program that provides expanded medical coverage to Medicare-eligible individuals who are uniformed service retirees aged 65 or older, as well as their eligible family members, survivors, and certain former spouses. To be eligible for TFL, you must have both Medicare Part A (Hospital Insurance) and Medicare Part B (Medical Insurance).

When it comes to prescription drug coverage, Medicare Part D is available to everyone with Medicare. You can enrol during the annual Medicare Part D Open Enrollment period, which typically runs from October 15 to December 7. If you have TRICARE and enrol in Medicare Part D, it is important to note that the TRICARE pharmacy benefit is considered creditable coverage. This means that if you go 63 continuous days or longer without creditable prescription drug coverage, you may have to pay higher premiums for a Medicare drug plan.

In terms of coordination of benefits, if you are on active duty and have both Medicare and TRICARE, TRICARE pays first for Medicare-covered services, and Medicare pays second. Additionally, if you join a Medicare drug plan, TRICARE and your plan may coordinate their benefits if your plan's network pharmacy is also a TRICARE network pharmacy. It is important to keep your doctor and contractor updated on your coverage to ensure proper coordination of benefits and timely payment of claims.

Understanding Insurance Medication Approval: How Long Does It Take?

You may want to see also

Explore related products

![]()

Medicare and drug coverage

Medicare drug coverage helps pay for prescription drugs. There are two main ways to get Medicare drug coverage. The first is to join a Medicare Advantage Plan (Part C) or other Medicare health plan with drug coverage. The second is to join a separate Medicare drug plan.

To join a Medicare Advantage Plan, you must have Medicare Part A (Hospital Insurance) and Medicare Part B (Medical Insurance). You will usually get your drug coverage through this plan. You can only join a separate Medicare drug plan without losing your current health coverage if you're in a Private Fee-for-Service Plan that doesn't include drug coverage. If you're in a Health Maintenance Organization, HMO Point-of-Service Plan, or Preferred Provider Organization and you join a separate drug plan, you'll be disenrolled from your Medicare Advantage Plan and returned to Original Medicare.

Medicare Part D Plans (PDP) are prescription drug plans that cover various brand-name and generic drugs. Generic drugs have the same active ingredients as brand-name drugs but usually cost less and are rated by the Food and Drug Administration (FDA) to be as safe and effective. Medicare Advantage HMO and PPO plans and Part D Prescription Drug Plans are offered by subsidiaries of The Cigna Group in select states and with select State Medicaid programs. Cigna's Medicare Part D Plans offer custom prescription medication, low copays, and large networks. They also offer no-cost programs and services, like savings on LASIK vision correction and acupuncture, as well as pharmacy networks to help you save. If you spend over $2,000 in drug costs each year, you can opt into the Medicare Prescription Payment Plan, which helps spread your prescription drug costs throughout the year.

Travel Insurance: AAA's Medical Coverage Options Explored

You may want to see also

Frequently asked questions

Medicare Supplement Insurance, also known as Medigap, is extra insurance that helps pay your share of costs in Original Medicare.

No, you can buy Medicare Supplement Insurance from a private company.

Yes, you can have Medicare and other health insurance at the same time. In this case, each type of coverage is called a "payer". The "primary payer" pays up to the limits of its coverage and then sends the rest of the balance to the "secondary payer".

The order of payment is called "coordination of benefits". The primary payer pays up to the limits of its coverage, and then the secondary payer pays for any remaining costs.

If you have employer-sponsored health insurance through your job or your spouse's job, you may be able to keep your insurance until you or your spouse retire. You will need to contact your employer's benefits representative to confirm.