In the US, young adults can remain on their parent's health insurance plan until they turn 26. After this, they must seek their own health insurance coverage. If you are unemployed or your job does not offer health insurance, you may be able to get free or low-cost health insurance through Medicaid. Each state has different income requirements for Medicaid eligibility.

| Characteristics | Values |

|---|---|

| Losing coverage from a parent's insurance plan | In most states, individuals lose coverage from their parent's insurance plan when they turn 26. |

| Coverage end date | If the insurance is job-based, coverage usually ends at the end of the month when the individual turns 26. If the insurance is an ACA marketplace plan, coverage usually ends at the end of the calendar year in which the individual turns 26. |

| Special cases | In eight states (Florida, Illinois, Nebraska, New Jersey, New York, Pennsylvania, South Dakota, and Wisconsin), individuals can stay on their parent's insurance plan past the age of 26. |

| Qualifying for Medicaid | A 26-year-old with a low income may qualify for Medicaid. |

| Other options | A 26-year-old can get their own health insurance through their employer or through a state health care marketplace. |

Explore related products

What You'll Learn

![]()

Losing health coverage when you turn 26

It is important to note that some states and plans have different rules, so it is always a good idea to check with the employer or plan provider to confirm the exact date your coverage will end. If your parent's plan is through the Marketplace, you can stay on their application and don't need to create a separate account. Your parent can enroll you in your own Marketplace plan during Open Enrollment, and your coverage will typically end during or shortly after the month you turn 26.

If you are about to age off your parent's health insurance, there are several options to consider for your own health coverage. Firstly, if your employer offers health insurance, you can qualify to enroll outside of their yearly Open Enrollment period. This is known as a Special Enrollment Period, which occurs when you experience certain life events such as losing health coverage, moving, getting married, or having a baby. You may have a limited time to enroll, so it is recommended to contact your job's human resources representative before turning 26 to understand your options and next steps.

Additionally, you can explore health insurance plans offered by organizations like Kaiser Permanente, either individually or through your state's health benefit exchange. Depending on your income and family size, you may be eligible for federal financial assistance or reduced out-of-pocket costs. You can also consider applying for Medicaid, which provides free or low-cost health coverage for individuals below certain income levels. Many states have expanded their Medicaid programs, and you can apply for this at any time without time restrictions. Other options include COBRA, which allows for the continuation of coverage under your parent's employer-sponsored plan.

Changing Medical Insurance While Pregnant: Is It Possible?

You may want to see also

Explore related products

![]()

Getting your own health insurance plan

If you are about to turn 26 and are currently on your parent's health insurance plan, you will need to take action to get your own health insurance coverage. If you do not, you may lose your health coverage. Depending on your situation, there are several options for getting your own health insurance plan.

Job-based health insurance plan

If your employer offers health insurance, you can qualify to enroll outside of their yearly Open Enrollment Period. You may have a limited time to enroll in job-based coverage, so be sure to contact your job's human resources representative before you turn 26 to learn about your next steps. If your employer offers health insurance that is considered "affordable" and you decide not to enroll in it, you generally won't qualify for a tax credit to lower your monthly insurance payment.

Health Insurance Marketplace Plan

The federal government operates the Health Insurance Marketplace, and some states run their own Marketplaces. You can apply at HealthCare.gov or your state's Marketplace website. During the application process, you will find out if you are eligible for Medicaid or the Children's Health Insurance Program (CHIP). If you have a limited income or are pregnant, you may qualify. These plans are independent of your employer, so you will have to pay the premium on your own. When you apply, you may qualify for subsidies. If someone claims you as a tax dependent, you can buy a plan through the federal or state Marketplace, but you won't qualify for savings based on your income.

Catastrophic health plan

You can also pick a "Catastrophic" health plan, which is a way to protect yourself mainly from worst-case scenarios.

Student health plan

If you are in school, you may be able to enroll in a student health plan and meet the requirement for having coverage under the health care law.

Employee Insurance and Medicaid: Can Spouses Mix Coverage?

You may want to see also

Explore related products

$35.18 $210

![]()

Qualifying for savings and discounts

In the United States, if you are under 26 and have a parent's health insurance plan that covers dependents, you can usually be added to their plan and remain on it until you turn 26. If you are covered by a parent's job-based plan, your coverage usually ends when you turn 26, but it is important to check with the employer or plan as some states and plans have different rules.

If you are turning 26 and are no longer covered by your parent's health insurance plan, you will need to take action to ensure you have health coverage. If your employer offers health insurance, you can qualify to enroll outside of their yearly Open Enrollment period if you lost your parent's coverage because you turned 26. You may have a limited time to enroll in job-based coverage, so it is important to contact your job's human resources representative before turning 26 to learn about your options.

If your employer offers health insurance that is considered "affordable" and you decide not to enroll in it, you generally won't qualify for a tax credit to lower your monthly insurance payment when you enroll in a plan through the Health Insurance Marketplace. However, you may still be able to get Marketplace coverage and qualify for a premium tax credit or other cost savings for a Marketplace plan. Four in five customers are able to find health coverage for $10 or less per month.

If you have limited Medicaid coverage, you can fill out an application through the Marketplace and find out if you qualify for full-benefit coverage through either Medicaid or a Marketplace insurance plan with savings based on your income. All states must offer former foster children uninterrupted Medicaid coverage until they turn 26, provided they meet certain requirements, such as being in the foster care system and receiving Medicaid benefits on their 18th birthday.

Additionally, some states have expanded their Medicaid programs to cover all people below certain income levels, so it is worth checking if your state offers this. Even if your state has not expanded Medicaid, you may still qualify based on your state's existing rules. You can apply for Medicaid and CHIP at any time of the year, and if it appears that anyone in your household qualifies, your information will be sent to your state agency, and they will contact you about enrollment.

If you are a qualifying government assistance recipient, you may also be eligible for a discounted Amazon Prime membership, known as Prime Access. To be eligible, you must provide verification of your participation in government assistance programs such as Supplemental Security Income, SNAP, Medicaid, or Temporary Assistance for Needy Families (TANF), among others.

Pet Owner's Guide to Medical Insurance Expenses

You may want to see also

Explore related products

![]()

State-specific rules for Medicaid eligibility

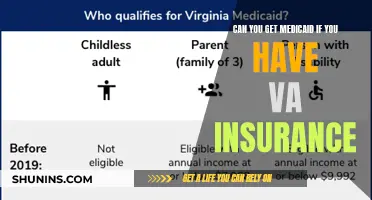

Medicaid is a federal-state partnership, with each state running its own program and setting eligibility rules. While the Affordable Care Act established a new methodology for determining income eligibility for Medicaid, based on Modified Adjusted Gross Income (MAGI), states have different income eligibility rules. In most states, children up to age 19 with a family income of up to $80,000 per year (for a family of four) may qualify for Medicaid. In many states, family income can be higher, and children can still qualify. Young people up to age 21 may be eligible for Medicaid, and those who have "aged out" of foster care can be covered until age 26; there is no income limit for these youth.

Additionally, youth with disabilities who receive Supplemental Security Income (SSI) can continue to receive Medicaid coverage while they work, attend post-secondary education, or receive job training. In most states, SSI recipients automatically qualify for Medicaid, but they must be significantly disabled and have low income and low assets.

In all states, Medicaid gives health coverage to some individuals and families, including children, parents, people who are pregnant, elderly people with certain incomes, and people with disabilities. States that have expanded Medicaid coverage allow individuals to qualify based on their income alone. If a household income is below 133% of the federal poverty level (which is effectively 138%), they qualify. A few states use a different income limit.

Some state-specific rules for Medicaid eligibility include:

- Michigan: The Michigan Department of Health and Human Services (MDHHS) determines eligibility for most health care programs administered by the state. All of the health care programs in Michigan have an income test, except for Children's Special Health Care Services, and some programs also have an asset test. The Plan First program is a health coverage program administered by the MDHHS that offers limited benefits related to family planning services. Individuals eligible for Plan First include those with income at or below 195% of the Federal Poverty Level, residents of Michigan, and those who meet Medicaid citizenship requirements.

- Michigan also has the MI Choice waiver, which provides home and community-based health care services for adults aged 65 or older and adults with disabilities.

Travel Medical Insurance: Income Tax Claim Benefits Explained

You may want to see also

Explore related products

![]()

Health insurance options for unemployed 26-year-olds

If you are unemployed and turning 26, you will no longer be covered by your parent's health insurance plan. You should take action to get your own health coverage. If you are unemployed, you may get health insurance through the Health Insurance Marketplace, which is run by the federal government. The marketplace can help you compare plans and choose the right one based on the cost, benefits, and coverage. Many states have their own insurance marketplaces, too.

Your income and household size may qualify you for savings through premium tax credits that reduce your monthly payments, or cost-sharing reductions that lower your out-of-pocket costs for care. You'll have to fill out an application to determine your eligibility for any cost savings. Being unemployed doesn't guarantee you any discounts. Anyone can apply for coverage during the open enrollment period, which runs from November 1 to January 15. If you want your coverage to begin on January 1, you must enroll by December 15. Coverage begins on February 1 if you enroll by January 15.

If you are unemployed, you may qualify for income-based government programs, including Medicaid and the Children's Health Insurance Program (CHIP). Both programs offer coverage to millions of people. Medicaid is a joint healthcare program between the federal and state governments. The program is designed for families (parents and children) with low incomes, as well as qualified pregnant women, some people living with disabilities, and others. Qualifications differ by state. You may be eligible in most states if your income falls under 133% of the federal poverty line (FPL). You must also live in the state where you receive coverage. CHIP is designed for children whose family incomes are too high to qualify for Medicaid but too low to buy private insurance. In some states, CHIP covers pregnant women. You can apply for both programs through a health insurance marketplace or your state's Medicaid website.

If your parent claims you as a tax dependent for the year after you turn 26, you may qualify for savings based on your parent's income and anyone else on their federal tax return. You can stay on your parent's application for Marketplace coverage and don't need to create a separate account. Your parent can enroll you in your own Marketplace plan during Open Enrollment. Your coverage will usually end during or shortly after the month you turn 26. Check with the plan or your parent’s employer for the exact date you'll lose coverage. When you age out of your parent’s job-based plan, you qualify for a Special Enrollment Period. This is a period of time outside of Open Enrollment when you can enroll in or change Marketplace plans. Your Special Enrollment Period starts 60 days before you lose coverage and ends 60 days after. If you enroll before you lose coverage, your new Marketplace plan can start as soon as the first day of the month after you lose coverage.

The High Cost of Medical Insurance: Why So Expensive?

You may want to see also

Frequently asked questions

In most states, you will be removed from your parent's health insurance plan when you turn 26. This health insurance rule was established by the Affordable Care Act (ACA).

You will need to take action if you have health coverage under a parent's plan. Contact your employer's human resources representative to learn about your next steps.

You can apply for your own health insurance plan through the Health Insurance Marketplace. If you are unemployed or your job does not offer health insurance, you may qualify for Medicaid. You may also qualify for a Special Enrollment Period.

A Special Enrollment Period is a period of time outside of Open Enrollment when you can enroll in or change Marketplace plans. Your Special Enrollment Period starts 60 days before you lose coverage and ends 60 days after.

In eight states (Florida, Illinois, Nebraska, New Jersey, New York, Pennsylvania, South Dakota, and Wisconsin), you can stay on your parent's health insurance plan after turning 26. In these states, you can stay on your parent's plan indefinitely if you have a qualifying disability.