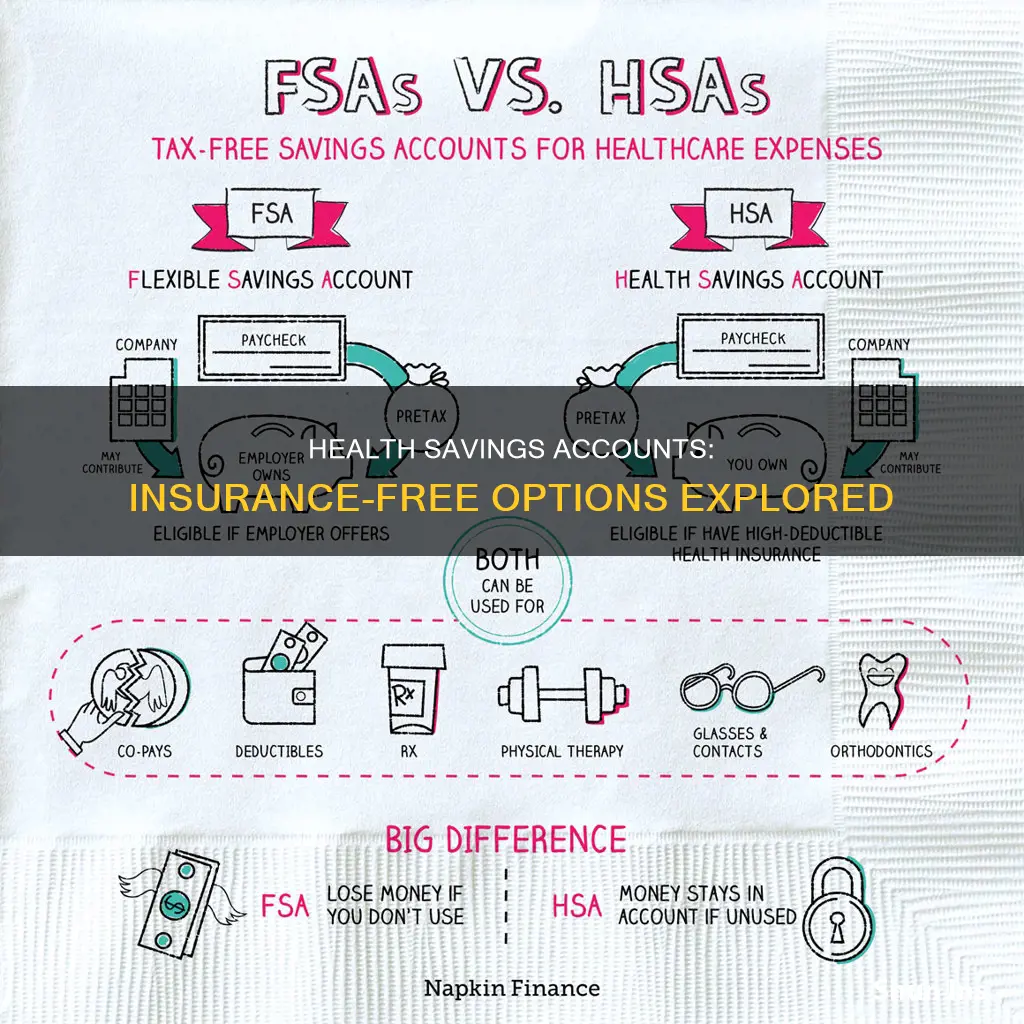

A Health Savings Account (HSA) is a tax-exempt trust or custodial account that individuals can set up with a qualified HSA trustee to pay for or reimburse certain medical expenses. To open an HSA, an individual must be enrolled in a qualified high-deductible health plan (HDHP) and cannot be claimed as a dependent on someone else's tax return. An HSA can be used to pay for qualified medical expenses, including some dental, drug, and vision expenses, that are not covered by an individual's health plan. While an HSA can help save on medical bills, there are rules, requirements, and limits to consider.

| Characteristics | Values |

|---|---|

| Can you have a health savings account (HSA) with no medical insurance? | You can only contribute to an HSA if you have an HSA-eligible plan (also called a High Deductible Health Plan (HDHP)). |

| How does an HSA work? | An HSA lets you set aside pre-tax money to pay for medical costs. The money grows tax-free as well. |

| What are the benefits of an HSA? | HSAs can help you save on medical bills, and provide tax advantages. |

| What are the limitations of an HSA? | You can't use HSA funds to pay premiums, except for long-term care insurance, COBRA, or other types of health insurance received while unemployed, and Medicare. |

| Can I use my HSA after I turn 65? | Yes, you can use the money in your HSA for anything you want after turning 65. If you don't use it for qualified medical expenses, it counts as income when you file your taxes. |

| Can I use my HSA with other types of medical coverage? | You cannot contribute to an HSA if you have disqualifying additional medical coverage, such as a general-purpose health flexible spending account (FSA). |

Explore related products

What You'll Learn

![]()

HSAs are tax-exempt

A Health Savings Account (HSA) is a tax-exempt trust or custodial account that you can set up with a qualified HSA trustee to pay or reimburse certain medical expenses. It is a powerful tool for managing healthcare costs and saving for future medical expenses. An HSA can be particularly useful if you have a High Deductible Health Plan (HDHP) as it provides a tax-advantaged way to save for future medical expenses.

HSA contributions are made by you or your employer and cannot exceed the HSA contribution limit each tax year. These contributions are tax-deductible, as are the account's earnings and withdrawals for eligible expenses. The money deposited into the HSA is not subject to federal income tax when the deposit is made. You can claim a tax deduction for contributions made to your HSA even if you don't itemize your deductions on Schedule A (Form 1040). Additionally, if you are 55 or older, you can make catch-up contributions of up to $1,000 per year.

It is important to note that if you use an HSA to pay for eligible medical expenses, you cannot itemize medical deductions for the same expenses on your tax return. However, if you have enough medical expenses that are not paid with the HSA, you may be able to claim them as an itemized deduction. Furthermore, if you withdraw money from your HSA for non-medical purposes, you may face penalties. Such withdrawals are taxed as regular income, and there is an additional 20% tax on the amount withdrawn.

To summarise, an HSA offers tax advantages for those with a high-deductible health plan, allowing them to save for future medical expenses while reducing their taxable income. However, it is essential to understand the rules and limitations to maximise the tax benefits of an HSA.

Breast Implants: Are They Covered by Medical Insurance?

You may want to see also

Explore related products

![]()

HSAs are for qualified medical expenses

A Health Savings Account (HSA) is a tax-exempt trust or custodial account that you can set up with a qualified HSA trustee to pay or reimburse certain medical expenses. An HSA can be established through a trustee that is different from your health plan provider. A qualified HSA trustee can be a bank, an insurance company, or anyone already approved by the IRS to be a trustee of individual retirement arrangements (IRAs) or Archer MSAs.

You can contribute to an HSA only if you have an HSA-eligible plan, also called a High Deductible Health Plan (HDHP). An HDHP combines an HSA or Health Reimbursement Arrangement (HRA) with traditional medical coverage. It provides insurance coverage and a tax-advantaged way to help save for future medical expenses. The funds can be used to cover qualified medical expenses that are not covered by your health plan.

Qualified medical expenses include some dental, drug, and vision expenses. They also include some special education expenses, such as tutoring for a child with learning disabilities caused by mental impairments, and weight-loss programs if they are a treatment for a specific disease diagnosed by a physician.

Money from your HSA can be used to pay for all qualified medical expenses. You can deduct the amount you deposit in an HSA from your taxable income. Unspent HSA funds roll over from year to year. You can hold and add to the tax-free savings to pay for medical care later. HSAs may earn interest that can’t be taxed. Generally, you can't use HSA funds to pay premiums. Once you turn 65, you can use the money in your HSA for anything you want. If you don't use it for qualified medical expenses, it counts as income when you file your taxes.

Missouri Medical Insurance: Are Premiums Wages for Work Comp?

You may want to see also

Explore related products

![]()

HSAs are for dental, drug, and vision expenses

A Health Savings Account (HSA) is a tax-advantaged account that can be used to pay for qualified healthcare expenses, while also reducing your taxable income. HSAs can be used to cover certain dental, drug, and vision expenses for yourself, your spouse, or eligible dependents.

Dental expenses that are typically covered by HSAs include orthodontic expenses, such as braces and Invisalign, which are considered medically necessary rather than cosmetic. Other dental procedures covered by HSAs include root canals and emergency treatments. However, it's important to note that general dental maintenance and self-care items, such as toothpaste, toothbrushes, and dental floss, are not typically covered by HSAs.

Drug expenses that are eligible for reimbursement through an HSA include over-the-counter medications and drugs purchased after January 1, 2020. This change was implemented due to the CARES Act, which eliminated the requirement for a prescription to seek reimbursement for over-the-counter drugs.

Vision care expenses that qualify for reimbursement through an HSA can include fees for optometrist visits and related treatments. Additionally, expenses for oral syringes used to dispense medication are also reimbursable under an HSA.

It is always advisable to consult your HSA provider to clarify which specific treatments, products, or procedures are eligible for coverage under your plan. Additionally, keeping a record of expenses paid for with your HSA is important in case proof of eligibility is ever required by your HSA provider or the IRS.

Understanding Tax Deductions on Large Medical Insurance Premiums

You may want to see also

Explore related products

![]()

HSAs are for a spouse's expenses

A Health Savings Account (HSA) is a tax-exempt trust or custodial account that you can set up with a qualified HSA trustee to pay or reimburse certain medical expenses. HSAs are a great way to save for future medical expenses, as they are tax-advantaged and provide flexibility in how you use your healthcare dollars.

If you and your spouse are both eligible—meaning you're both covered under a qualifying high-deductible health plan (HDHP)—then you can each open your own HSAs. You can then use the funds from either HSA to pay for each other's medical expenses. This is a great way to reduce your tax bill, especially if one spouse falls into a higher tax bracket than the other. It's important to note that there is no such thing as a joint HSA; HSAs are individual accounts, even if you and your spouse are both covered by a family HDHP.

If you have two separate HSAs, you can't combine the annual contribution limits. For 2024, the self-only maximum contribution limit is $4,150, and the family contribution limit is $8,300. These limits increase in 2025 to $4,300 and $8,550, respectively. If one or both spouses are 55 or older, you may be eligible for additional catch-up contributions of $1,000 to your HSAs.

You can use your HSA funds to pay for the medical expenses of any dependent children claimed on your income tax return, even if your spouse has individual-only coverage under a traditional medical plan. This includes expenses for items like home testing for COVID-19 and personal protective equipment, which are considered qualified medical expenses.

Understanding CMS: Medicare and Medicaid Simplified

You may want to see also

Explore related products

![]()

HSAs are for dependent expenses

A Health Savings Account (HSA) is a tax-exempt trust or custodial account that you can set up with a qualified HSA trustee to pay or reimburse certain medical expenses. It is intended to help you save pre-tax or tax-deductible dollars to pay for qualified medical expenses that are not covered by insurance. HSAs are for dependent expenses, but it is important to note that dependents are defined differently for HSAs than for traditional health coverage.

The IRS breaks dependent status into two categories: qualifying child and qualifying relative. To be considered a dependent for an HSA, one must meet the requirements for one of these categories. For example, a qualifying child cannot be 19 or older (or 24 or older if enrolled in college) and must share a primary residence with the claimant for at least half of the calendar year. The IRS has strict rules regarding who is considered a dependent, and it is important to consult their guidelines to determine if a dependent's medical expenses are eligible for HSA funds.

Account holders can use their HSA funds to cover out-of-pocket medical expenses for themselves and their dependents, including medical, dental, and vision care. HSAs can also be used to pay for a spouse's qualified medical expenses and those of any other person claimed as a dependent on the account holder's tax return. It is important to note that HSA funds cannot be used to pay for health insurance premiums, except in certain situations, such as when the account holder's dependent has a qualifying high-deductible health plan (HDHP).

HSAs offer tax advantages, such as lower premiums and tax savings, and provide flexibility in how individuals use their healthcare dollars. They can be a great way to save for future medical expenses and ensure that loved ones have access to the care they need.

Insurance Options at Advocate Medical Group: What You Need to Know

You may want to see also

Frequently asked questions

A health savings account (HSA) lets you set aside pre-tax money to pay for medical costs. The money grows tax-free and can be used to pay for qualified medical expenses that are not covered by your health plan.

An HSA can be paired with an HDHP to provide insurance coverage and a tax-advantaged way to save for future medical expenses. HDHPs typically have lower premiums but higher deductibles, so an HSA can help cover significant medical expenses.

HSA funds can generally only be used for qualified medical expenses, which include some dental, drug, and vision expenses. These expenses must not be covered by your insurance plan. Some exceptions include premiums paid for long-term care insurance, COBRA, or Medicare.