It is possible to have both Medicaid and Marketplace insurance at the same time, as some individuals may be eligible for both. However, having Medicaid as a qualifying health coverage means you no longer qualify for the premium tax credit or extra savings to lower the cost of your Marketplace plan. If you have a Marketplace plan and become eligible for Medicaid, you must notify your state agency, and you may have to pay back some or all of the premium tax credit you received.

| Characteristics | Values |

|---|---|

| Can you have Medicaid and Marketplace Insurance at the same time? | Yes, but only if you qualify for the Marketplace. |

| Who qualifies for the Marketplace? | People whose incomes are just above the level to qualify for Medicaid. |

| How to apply for Medicaid and Marketplace Insurance? | By phone, online, in person, or by mail. |

| When to apply for Marketplace Insurance? | During the annual Open Enrollment Period (OEP) or during a Special Enrollment Period (SEP) if certain circumstances are met. |

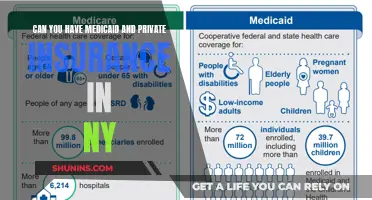

| Who is eligible for Medicaid? | Low-income people, families, children, pregnant women, the elderly, and people with disabilities. |

| How to check if you qualify for Medicaid? | Enter your household size and state on the HealthCare.gov website. |

| Can you have both Medicaid and Marketplace Insurance if you are self-employed? | Yes, but you may have to pay back the advance tax credit for the months you had both. |

Explore related products

What You'll Learn

![]()

Enrollment in Medicaid and Marketplace insurance

Medicaid is a federal and state-funded program that provides free or low-cost health coverage to eligible individuals. Enrollment in Medicaid can be done at any time, and individuals can apply by phone, online, in person, or by mail. The application process has been streamlined, and individuals do not need to provide past medical records or lengthy documents. Additionally, Medicaid may cover medical expenses incurred up to 90 days before enrollment, even if the individual was not yet enrolled in the program. This makes it a crucial safety net for those facing unexpected medical costs.

The Health Insurance Marketplace, on the other hand, is a platform where individuals can shop for and enroll in private health insurance plans. Enrollment in the Marketplace is typically restricted to the annual Open Enrollment Period (OEP) or during a Special Enrollment Period (SEP) if an individual experiences qualifying circumstances, such as losing current medical coverage, marriage, divorce, or obtaining citizenship. While Marketplace plans tend to be more expensive than Medicaid, they can be a good option for those who do not qualify for Medicaid but still need financial assistance with healthcare costs.

It is possible to have both Medicaid and Marketplace insurance simultaneously, as seen in some cases where individuals accidentally had both. However, it is important to note that having Medicaid as a primary insurance usually means that Marketplace coverage becomes secondary. This can have implications on tax deductions for self-employed individuals, and they may need to pay back advance premium tax credits received during the period of dual coverage.

When assisting individuals with enrollment, it is essential to use plain language, focus on the benefits of health insurance for the individual, and be mindful of any past negative experiences with the application process. By simplifying the process and highlighting the advantages of coverage, more individuals can be empowered to access the healthcare services they need.

Navigating Insurance Appeals: Can You Challenge an Appeal Decision?

You may want to see also

Explore related products

![]()

Tax implications of having both

It is possible to have both Medicaid and Marketplace insurance at the same time, but there are tax implications to consider. Firstly, if you have qualifying health coverage through Medicaid, you are no longer eligible for the premium tax credit or extra savings on your Marketplace plan. This means that you will have to pay the full price for your Marketplace plan premium and covered services. If you do not end your Marketplace coverage when your Medicaid coverage starts, you may be required to pay back some or all of the premium tax credit when filing your federal taxes.

On the other hand, if your Medicaid program does not count as qualifying health coverage, you may be eligible for lower costs on your Marketplace plan based on your income and other factors. This is because financial eligibility for the premium tax credit is determined using a tax-based measure of income called modified adjusted gross income (MAGI). It is important to note that the MAGI methodology for calculating income differs from previous Medicaid rules, and some types of income that were previously considered are no longer counted.

Additionally, if you have enrolled in insurance coverage through the Marketplace, you should report any changes in your circumstances, such as changes to your household income or family size, as this may affect your advance payments of the premium tax credit. By reporting these changes, you may become eligible for a special enrollment period, allowing you to purchase health care insurance through the Marketplace outside of the open enrollment period.

Furthermore, if advance payments of the premium tax credit were made on your behalf or a family member's behalf, and you do not file a tax return reconciling those payments, you will be responsible for the full cost of your monthly premiums and covered services in the next year. You may also be contacted to pay back some or all of the advance payments of the premium tax credit. To avoid this, it is essential to electronically file your tax return with Form 8962 by the due date.

Lastly, if you have more than 50 employees, you may be able to use the SHOP Marketplace to offer health and dental coverage to your employees. Businesses that offer health coverage through the SHOP Marketplace may be eligible for the small business health care tax credit.

Medical Marijuana Insurance Coverage: What's the Deal?

You may want to see also

Explore related products

![]()

Applying for Medicaid and Marketplace insurance

Medicaid and the Children's Health Insurance Program (CHIP) provide free or low-cost health coverage for some low-income people, families, and children, pregnant women, the elderly, and people with disabilities. Some states have expanded their Medicaid programs to cover all people below certain income levels. To apply for Medicaid, you must first check your eligibility. Enter your household size and state to determine if you qualify for Medicaid or savings on a Marketplace plan. Even if you don't qualify for Medicaid based on income, you should still apply, as you may qualify for your state's program, especially if you have children, are pregnant, or have a disability.

You can apply for Medicaid and CHIP any time of year. If anyone in your household qualifies for Medicaid or CHIP, your information will be sent to your state agency, and they will contact you about enrollment. When you submit your Marketplace application, you will also find out if you qualify for cost savings on a Marketplace plan. You can apply for coverage for both Medicaid and Marketplace insurance by phone, online, in person, or by mail. The National Health Insurance Marketplace call center can assist you in English and 150 other languages.

If you have limited Medicaid coverage, you can fill out an application through the Marketplace and find out if you qualify for full-benefit coverage through either Medicaid or a Marketplace insurance plan with savings based on your income. If your state has not expanded Medicaid, you may still qualify based on your state's existing rules, which vary from state to state and may consider income, household size, family status, disability, age, and other factors. Generally, if your income is just above the level to qualify for Medicaid, you can pay very low premiums and out-of-pocket costs for private health insurance through the Marketplace.

Remember, Medicaid and Marketplace insurance have different enrollment periods. Individuals eligible for Medicaid can enroll at any time, while Marketplace insurance typically has an annual Open Enrollment Period (OEP) and Special Enrollment Periods (SEP) for qualifying life events such as losing current medical coverage, marriage, or gaining access to Medicaid.

How to Submit Your Own Medical Insurance Claim

You may want to see also

Explore related products

![]()

Eligibility criteria for Medicaid and Marketplace insurance

Medicaid and the Children's Health Insurance Program (CHIP) provide free or low-cost health coverage to some low-income people, families, and children, pregnant women, the elderly, and people with disabilities. Some states have expanded their Medicaid programs to cover all adults below a certain income level.

Eligibility rules differ among states. However, in all states, Medicaid provides health coverage to some individuals and families, including children, parents, people who are pregnant, elderly people with certain incomes, and people with disabilities. Some states have established a ""medically needy program"" for individuals with significant health needs whose income is too high to qualify for Medicaid under other eligibility groups. These individuals can become eligible by ""spending down"" the amount of income that is above a state's medically needy income standard.

To participate in Medicaid, federal law requires states to cover certain groups of individuals. Low-income families, qualified pregnant women and children, and individuals receiving Supplemental Security Income (SSI) are examples of mandatory eligibility groups. The Affordable Care Act established a new methodology for determining income eligibility for Medicaid, which is based on Modified Adjusted Gross Income (MAGI). MAGI is used to determine financial eligibility for Medicaid, CHIP, and premium tax credits and cost-sharing reductions available through the health insurance marketplace.

Individuals can apply for coverage for both Medicaid and the Marketplace by phone, online, in person, or by mail. Enrollments in or changes to a Health Insurance Marketplace plan can only take place during the annual Open Enrollment Period (OEP) or during a Special Enrollment Period (SEP) if the individual meets qualifying circumstances. Members of a federally recognized Indian tribe or Alaska Native shareholders can sign up for or change plans once per month throughout the year. Individuals eligible for Medicaid can enroll at any time.

Combining Medical and Private Insurance: Is It Possible?

You may want to see also

Explore related products

![]()

Coverage provided by Medicaid and Marketplace insurance plans

Medicaid and the Children's Health Insurance Program (CHIP) provide free or low-cost health coverage to millions of Americans. This includes low-income people, families and children, pregnant women, the elderly, and people with disabilities. Some states have expanded their Medicaid programs to cover all adults below a certain income level.

Medicaid programs must follow federal guidelines, but coverage and costs vary from state to state. Some programs pay for care directly, while others use private insurance companies to provide coverage. Importantly, Medicaid may cover medical care costs incurred up to three months before enrolment in the program.

The Health Insurance Marketplace is a federal service that helps people, families, and small businesses compare health insurance plans, enroll in or change a plan, and find out about tax credits and health programs like Medicaid and CHIP. Enrolling in a Marketplace plan can only take place during the annual Open Enrollment Period (OEP) or during a Special Enrollment Period (SEP) if certain circumstances are met.

If you have Marketplace coverage and become eligible for Medicaid, you should consider ending your Marketplace coverage. This is because, once eligible for Medicaid, you no longer qualify for premium tax credits or extra savings on your Marketplace plan. However, if your Medicaid program does not count as qualifying health coverage, you may qualify for lower costs on your Marketplace plan based on your income and other factors.

It is important to note that if you do not end your Marketplace coverage when your Medicaid coverage starts, you may have to pay back some or all of the premium tax credit when filing your federal taxes.

How to Add Your Mother to Your Medical Insurance

You may want to see also

Frequently asked questions

Yes, you can apply for both Medicaid and Marketplace Insurance. You can apply by phone, online, in person, or by mail.

Yes, it is possible to have both at the same time. However, if you have Medicaid, you won't be eligible for savings on a Marketplace plan.

Medicaid provides free or low-cost health coverage to some low-income people, families, and children, pregnant women, the elderly, and people with disabilities. You can check your eligibility by entering your household size and state.

Enrollments in a Health Insurance Marketplace plan can only take place during the annual Open Enrollment Period (OEP) or during a Special Enrollment Period (SEP) if you meet certain circumstances. Individuals eligible for Medicaid can enroll at any time.