Health insurance policies are designed to cover medical expenses incurred during the period when the policy is active. However, there are exceptions where insurance might cover past medical bills. For instance, certain health insurance plans may offer retroactive coverage under specific circumstances, such as having a gap in coverage during which medical services were received. Additionally, COBRA enrollment can provide retroactive coverage from the date an individual's previous employer-sponsored plan ended. In the case of Medicaid, retroactive eligibility allows for coverage of medical expenses incurred up to 90 days or three months before the application date, providing a safety net for individuals facing unexpected illnesses or injuries.

| Characteristics | Values |

|---|---|

| Can you retroactively apply your insurance to medical bills? | Health insurance typically does not cover past medical bills incurred before the effective date of a policy. |

| Retroactive Coverage | Some health insurance plans may offer retroactive coverage under specific circumstances. |

| COBRA Enrollment | If you lose your job and subsequently enroll in COBRA, your coverage can be retroactive to the date your previous employer-sponsored plan ended. |

| State-Specific Regulations | Some states have regulations that provide additional protections or options for individuals seeking coverage for past medical bills. |

| Retroactive Medicaid Eligibility | Retroactive eligibility allows persons time to apply for Medicaid without stressing over how the bills are going to be paid. |

Explore related products

What You'll Learn

![]()

Retroactive coverage

Health insurance policies typically cover medical expenses incurred during the active period of the policy. This means that medical services received before the policy's effective date are generally not covered retroactively. However, there are a few exceptions and special circumstances where retroactive coverage may apply.

One scenario is when an individual has a gap in coverage during which they receive medical services. In this case, if they had applied for a new insurance policy and were approved, their insurer might cover those expenses once the policy becomes active. This is known as "retroactive coverage" and is offered by some health insurance plans under specific conditions.

Another situation is related to COBRA (Consolidated Omnibus Budget Reconciliation Act) enrollment. If an individual loses their job and enrolls in COBRA, their coverage can be retroactive to the date their previous employer-sponsored plan ended. This means that any medical services received during the gap period may be covered once they enroll in COBRA.

State-specific regulations also play a role in retroactive coverage. Certain states have regulations that offer additional protections or options for individuals seeking coverage for past medical bills. These regulations can vary from state to state, so it is important for individuals to understand the specific rules in their state.

In the case of Temporary Continuation of Coverage (TCC), there is a 31-day temporary extension of coverage at no cost if an individual loses their FEHB coverage (other than by cancellation). If enrollment processing is completed after this period, the coverage is retroactive to the date of separation. However, if the individual waits longer to enroll, they may be billed for the entire period of retroactive coverage.

It is important to note that retroactive coverage is not a standard feature of all insurance policies, and each policy has its own terms and conditions. Individuals should carefully review their insurance policy documents or consult with an experienced insurance agent to understand their specific coverage and whether retroactive coverage is applicable in their situation.

Medicaid and Private Insurance: Michigan's Dual Coverage Option

You may want to see also

Explore related products

![]()

COBRA enrollment

Health insurance policies typically cover medical expenses incurred during the period when the policy is active. This means that if you received medical services before the policy's effective date, those expenses are generally not covered. However, there are a few exceptions where health insurance might cover past medical bills. One such exception is COBRA enrollment.

COBRA (Consolidated Omnibus Budget Reconciliation Act) is a US law that allows employees to keep their group health plan after experiencing a job loss, reduction in hours, divorce, widowhood, or an adult child turning 26 and losing their coverage under their parent's plan. The process of enrolling in COBRA starts with the employer or their benefits administrator. The employer has 30 days to notify the group health plan of the qualifying event and 14 days to notify the employee of their right to continue their work health insurance. In total, the employer has 45 days to send the COBRA election notice, which includes information on the monthly premium and how to apply. Once the employee receives the COBRA enrollment forms, they have 60 days to elect the plan or waive their right to continue.

If you enroll in COBRA after losing your job, your coverage can be retroactive to the date your previous employer-sponsored plan ended. This means that if you received medical services during the gap between your employer-sponsored plan ending and enrolling in COBRA, those expenses might be covered once you enroll. It is important to note that COBRA coverage can be expensive, as the former employer is no longer contributing. Additionally, there may be alternative options available, such as switching to a Marketplace plan or enrolling in Medicaid or CHIP.

While health insurance typically does not cover past medical bills, understanding exceptions like COBRA enrollment can provide options for managing healthcare expenses effectively. Consulting with experts, such as insurance agents, can help individuals navigate the complexities of health insurance and ensure they understand their coverage options fully.

Medical Insurance Options for Diverticulosis Patients

You may want to see also

Explore related products

![]()

State-specific regulations

Health insurance policies typically cover medical expenses incurred during the active period of the policy. This means that medical services received before the policy's effective date are generally not covered. However, there are state-specific regulations and exceptions to this rule that allow for retroactive coverage under specific circumstances.

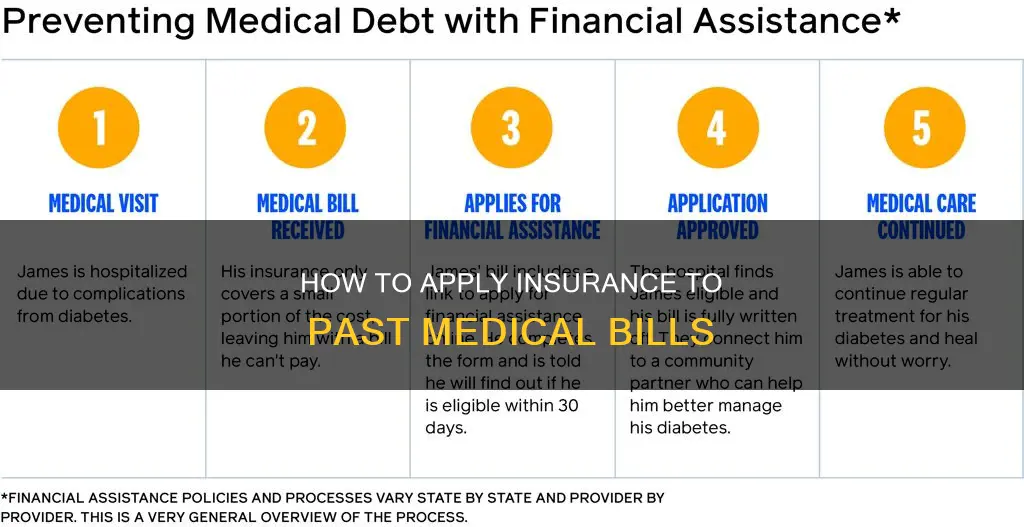

Retroactive coverage is provided in certain states for individuals who qualify for Medicaid. When applying for Medicaid, if approved, some states will cover medical expenses incurred up to 90 days in the past. This is known as Retroactive Medicaid Eligibility and is meant to provide a safety net for financially needy individuals who face unexpected illnesses or injuries. To be eligible, applicants must meet the financial and functional eligibility requirements prior to their application date. For example, Bill, who moves into a nursing home in March but only applies for Medicaid in June, can have his unpaid nursing home expenses for March, April, and May covered by Medicaid.

Some states only cover unpaid medical expenses, while others will reimburse Medicaid recipients for paid bills. Additionally, some states are limiting or restricting retroactive eligibility through Section 1115 Demonstration Waivers, which allow them to disregard certain federal rules.

It is important to note that state-specific regulations may vary, and it is always advisable to consult with experts and stay informed about your rights and coverage details to effectively manage healthcare expenses.

Accessing Weight Loss Medication sans Insurance: Options and Strategies

You may want to see also

Explore related products

![The Guardian [Blu-ray]](https://m.media-amazon.com/images/I/81BzvjroRfL._AC_UY218_.jpg)

![]()

Retroactive Medicaid eligibility

Health insurance policies typically cover medical expenses incurred during the period when the policy is active. This means that medical services received before the policy's effective date are generally not covered. However, there are a few exceptions where health insurance might cover past medical bills.

Retroactive Medicaid is one such example, which allows applicants to receive coverage for up to three months prior to their application date. To be eligible, one must meet the requirements during this retroactive period. This provision acts as a safety net for financially needy individuals who face unexpected illnesses or injuries. It provides a way for them to get their medical bills paid without worrying about immediate eligibility or the lengthy application process. Retroactive eligibility also applies to Regular State Plan Medicaid and Categorically Aged, Blind, and Disabled, and in some states, Home and Community-Based services.

While retroactive eligibility is federally mandated, some states are restricting or limiting it. For instance, some states only cover unpaid medical expenses, while others reimburse Medicaid recipients for paid bills. Additionally, certain states have their own regulations that provide additional protections or options for individuals seeking coverage for past medical bills.

It is important to note that health insurance policies can be complex, and understanding exceptions can provide clarity on managing healthcare expenses effectively. Consulting with experts or experienced insurance agents can help individuals navigate these complexities and ensure they make the best choices for their healthcare needs.

Medical Coverage: One Medical vs Insurance, Who Wins?

You may want to see also

Explore related products

![]()

Medicaid application process

Health insurance typically does not cover medical expenses incurred before the policy's effective date. However, there are a few exceptions where health insurance might cover past medical bills. These include retroactive coverage, COBRA enrollment, and state-specific regulations.

Now, here is a detailed overview of the Medicaid application process:

Medicaid is a joint federal and state program that provides health coverage to millions of Americans, including children, pregnant women, parents, seniors, and individuals with disabilities. The application process for Medicaid can vary depending on your state and category of eligibility. Here are the general steps to apply for Medicaid:

- Find Your State's Medicaid Agency: Contact your state's Medicaid agency to understand the specific requirements and application process for your state. You must be a resident of the state where you are applying for benefits.

- Create an Account with the Health Insurance Marketplace: Visit the Health Insurance Marketplace website and create an account. You will need to provide basic information such as your name, contact details, and household information.

- Fill Out the Application: Complete the Medicaid application form. You may need to provide certain information or documentation, such as income details, information about your household members, and details about any current insurance plans. The requirements may vary depending on your state.

- Review and Enrollment: Once you have submitted your application, your state agency will review it to determine your eligibility for Medicaid. They will contact you if they require additional information. If you are eligible, your coverage will begin either on the date of application or the first day of the month of application. In some cases, benefits may even be applied retroactively for up to three months before the month of application if you would have been eligible during that period.

- Renewal and Updates: Your state may review your information annually to decide if you continue to be eligible for Medicaid. They will contact you about renewing your coverage if needed. It is important to inform your state agency of any changes in your circumstances, such as income or household size, as they may impact your eligibility.

- Finding a Medicaid Provider: Not all medical providers accept Medicaid. You can locate a Medicaid medical provider by checking with your state's Medicaid agency or using their website to search for participating providers in your area.

- Understanding Eligibility: Eligibility for Medicaid is generally based on your income and household size. The Affordable Care Act introduced the use of Modified Adjusted Gross Income (MAGI) to determine financial eligibility. This considers your taxable income and tax filing relationships. Additionally, certain categories of individuals, such as those with disabilities or those who are pregnant, may have specific eligibility criteria and application processes.

- Appeals Process: If you disagree with any decisions regarding your eligibility or application, you have the right to appeal. You can contact your state agency, application counselor, or customer service center to discuss your concerns. Fair hearings and appeals are available in most states to ensure that your case is reviewed thoroughly.

Medicaid as Secondary Insurance: Ohio's Unique Scenario

You may want to see also

Frequently asked questions

Health insurance policies typically cover medical expenses incurred during the period when the policy is active. However, there are a few exceptions where health insurance might cover past medical bills, such as retroactive coverage plans, COBRA enrollment, and state-specific regulations.

Retroactive coverage is when an insurance provider agrees to cover medical expenses incurred during a gap in coverage, once your policy becomes active.

COBRA (Consolidated Omnibus Budget Reconciliation Act) enrollment allows for retroactive coverage if you lose your job and your previous employer sponsored your health insurance plan. This means that if you received medical services during the gap in coverage, they might be covered once you enroll in COBRA.

Yes, some states have regulations that provide additional protections or options for individuals seeking coverage for past medical bills. Additionally, Medicaid offers retroactive coverage for up to 90 days preceding the application date in some states.