Medicaid is a federal-state program that provides health coverage for low-income individuals, families, and children, as well as pregnant women, the elderly, and people with disabilities. Medicare, on the other hand, is a federal program that primarily supports people aged 65 and over and those with qualifying disabilities. Medicare Supplement Insurance, or Medigap, is extra insurance that can be purchased to fill the gaps in Original Medicare coverage, such as copayments, deductibles, and coinsurance. It is important to carefully assess your healthcare needs and eligibility for Medicaid and Medicare Supplement Insurance to avoid unnecessary duplication of coverage and optimize your benefits.

| Characteristics | Values |

|---|---|

| Medicaid eligibility | Income, household size, state-specific rules and categories of beneficiaries |

| Medicaid coverage | Hospital and doctor visits, prescription drugs, preventive care, nursing home care, personal care services, and other necessary medical services |

| Medicare Supplement Insurance | Extra insurance to cover out-of-pocket costs in Original Medicare; sold by private companies |

| Medicare Supplement Insurance purchase | Available from any licensed insurance company in your state; monthly premium varies |

| Medicare Supplement Insurance and Medicaid | Assess healthcare needs to avoid unnecessary duplication; consider Medicaid Long-Term Care programs and their specific coverages |

Explore related products

What You'll Learn

![]()

Medicaid and Medicare Supplement Insurance: how they work together

Medicaid and Medicare are two different healthcare insurance options in the US. While Medicare primarily supports people aged 65 and over and those with qualifying disabilities, Medicaid is a joint federal and state program that provides health coverage for low-income individuals, families, children, pregnant women, and the elderly.

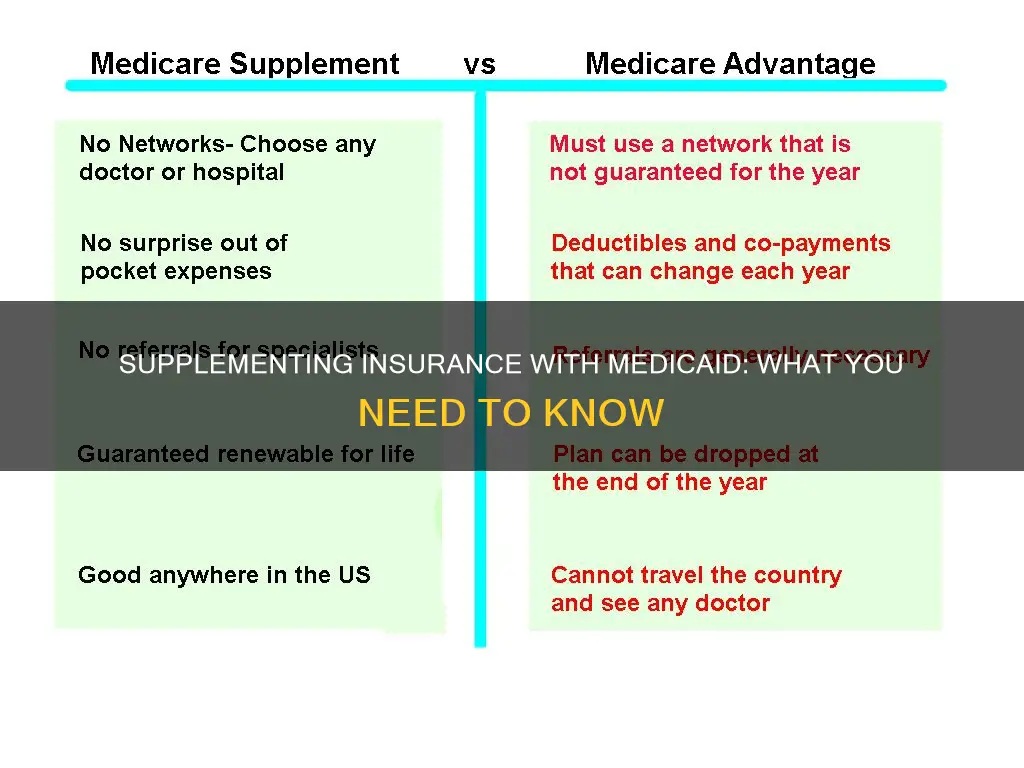

Medicare Supplement Insurance, also known as Medigap, is an additional insurance policy that can be purchased from a private health insurance company to help pay for out-of-pocket costs in Original Medicare (Parts A and B). Medigap plans are standardized and labeled with letters, each offering distinct benefits. These plans are designed to fill the gaps left by Original Medicare, such as copayments, deductibles, and coinsurance.

When considering Medicaid and Medicare Supplement Insurance together, it is important to recognize their different use cases. Having both is known as being "dual eligible". In this case, Medicare pays first for Medicare-covered services, and Medicaid pays last, after Medicare and any other health insurance. If you are dually eligible, Medicare will cover your prescription drugs.

The decision to keep your Medicare Supplement Insurance while on Medicaid depends on the specific Medicaid Long-Term Care program you have. For example, if you have a Medicare A and B plan with Medicare Supplement Insurance and qualify for Nursing Home Medicaid, it may not make sense to continue paying for the supplement insurance, as Nursing Home Medicaid will cover all your healthcare costs. On the other hand, if you are receiving long-term care benefits through Home and Community-Based Services (HCBS) Waivers Medicaid, you may need to determine how your needs are covered by both options and whether the Medicare Supplement Insurance provides sufficient savings to justify the cost.

Understanding Medical Insurance Copay Tax Deductibility

You may want to see also

Explore related products

![]()

Income-based eligibility for Medicaid

Medicaid is a federal and state-funded program that provides health coverage for low-income individuals. The eligibility criteria for Medicaid are based on income and household size, with variations between states and beneficiary categories. For instance, in Utah, adults whose annual income is up to 138% of the federal poverty level ($17,608 for an individual or $36,156 for a family of four) are eligible for Medicaid.

Medicaid generally offers comprehensive healthcare coverage, including hospital and doctor visits, prescription drugs, preventive care, and other necessary medical services. It is important to note that not all nursing homes accept Medicaid, and there may be waitlists for long-term care services.

Medicare, on the other hand, is a federal program that primarily supports individuals 65 and older and those with qualifying disabilities. Medicare Supplement Insurance, or Medigap, is private insurance that can be purchased to fill the gaps in Original Medicare coverage, such as copayments, deductibles, and coinsurance.

When considering Medicaid and Medicare Supplement Insurance together, it is essential to assess your healthcare needs and maximize benefits without unnecessary duplication. For example, if you have Medicare A and B and qualify for Nursing Home Medicaid, it may not be necessary to keep paying for Medicare Supplement Insurance, as Nursing Home Medicaid covers all healthcare costs.

Additionally, it is worth noting that Medicare Supplement Insurance plans are standardized and labeled with letters, each offering distinct benefits. These plans are sold by private companies and vary by state, but they are designed to fit into the "gaps" of Medicare A and B plans.

Medicaid Lien on Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Comprehensive healthcare coverage under Medicaid

Medicaid is a federal and state-funded program that provides comprehensive healthcare coverage to individuals and families who meet certain income and household size requirements. The specific eligibility criteria and benefits offered can vary from state to state, but generally, Medicaid offers extensive coverage, including hospital and doctor visits, prescription drugs, preventive care, and other necessary medical services.

Medicaid is designed to provide broad coverage for a wide range of healthcare services, and it is an essential safety net for those who may not be able to afford private insurance or qualify for other government-sponsored programs like Medicare. In fact, for those who are "dual eligible", having both Medicare and Medicaid can ensure that all healthcare costs are covered, including skilled and non-skilled care, medications, supplies, and durable goods.

While Medicaid typically provides comprehensive coverage, there are some instances where individuals may choose to supplement their Medicaid coverage with additional insurance. This may occur if an individual requires long-term care services, such as nursing home care or Home and Community-Based Services (HCBS), which can have waitlists or limited availability under Medicaid. In these cases, individuals may opt for a Medicare Supplement Insurance plan, also known as Medigap, which is private insurance designed to fill gaps in Original Medicare coverage.

It is important to note that Medicare Supplement Insurance plans do not cover everything, and they may not be necessary or cost-effective for everyone. For example, these plans do not typically cover vision, dental, hearing aids, private nurses, or doctors' services. Additionally, any Medicare Supplement Insurance plan sold after January 1, 2006, will not cover prescription medication. As such, it is crucial for individuals to carefully assess their healthcare needs and understand the specific benefits offered by their Medicaid plan before deciding to purchase additional insurance.

Overall, Medicaid is designed to provide comprehensive healthcare coverage, and for many individuals and families, it is a vital source of accessible and affordable healthcare services.

Understanding Medical Insurance Expiry and Validity Periods

You may want to see also

Explore related products

![]()

Enrollment in Medicare Supplement Insurance plans

Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from a private insurance company to help pay for out-of-pocket costs in Original Medicare (Parts A and B). Medigap policies are standardized and labelled with letters, each offering distinct standard benefits. The primary goal of a Medigap plan is to help cover some of the out-of-pocket costs of Original Medicare, such as copayments, deductibles, and coinsurance.

You can only buy Medigap if you have Original Medicare, which means signing up for Medicare Part A (Hospital Insurance) and Part B (Medical Insurance). Once you have Medicare Part B and are 65 or older, you will have a 6-month Medigap Open Enrollment period, during which you can enrol in any Medigap policy and the insurance company cannot deny you coverage due to pre-existing health problems. After this period, you may not be able to buy a Medigap policy, or it may cost more. It is important to note that Medigap policies are generally a one-time enrollment and do not repeat every year like the Medicare Open Enrollment Period.

Medigap policies can be purchased from any licensed insurance company in your state. The price is the only difference between plans with the same letter sold by different insurance companies. In some states, you may be able to purchase a Medigap policy called Medicare SELECT, which allows you to change your mind within 12 months and switch to a standard Medigap policy.

It is important to carefully consider your healthcare needs when contemplating a Medicare Supplement Insurance plan alongside Medicaid to ensure that you maximize benefits without unnecessary duplication. Additionally, it is worth noting that having both Medicare and Medicaid at the same time is known as being "dual eligible." For example, if you have Medicare A and B and qualify for Nursing Home Medicaid, it may not make financial sense to keep paying for your Medicare Supplement Insurance, as Nursing Home Medicaid will cover all your healthcare costs.

Understanding Copayment: Your Medical Insurance Cost Explained

You may want to see also

Explore related products

![]()

Medigap plans and their benefits

Medicare Supplement Insurance, also known as Medigap, is extra insurance that you can buy from a private health insurance company. It helps to pay your share of out-of-pocket costs in Original Medicare, which includes Part A (Hospital Insurance) and Part B (Medical Insurance). Medigap policies are designed to fill the "gaps" in Original Medicare Plan coverage and help pay for some of the healthcare costs that the Original Medicare Plan doesn't cover. For example, Medicare Part B generally covers about 80% of Part B expenses, and you are responsible for the remaining 20%. A Medigap policy can help pay this remaining amount.

Medigap policies must follow Federal and state laws, and the front of the policy must clearly identify it as "Medicare Supplement Insurance." Insurance companies can only sell standardized Medigap policies, and these policies must provide the same benefits, regardless of the company selling them. The only difference between Medigap policies sold by different insurance companies is the cost. It's important to compare Medigap policies, as costs can vary. Additionally, you and your spouse must buy separate Medigap policies, as your policy will not cover any healthcare costs for your spouse.

Some Medigap policies also offer additional benefits that aren't covered by Medicare. For example, some plans, such as Plans G, C6, or F6, offer high levels of coverage and pay up to 100% of your out-of-pocket costs for many Medicare-approved services. These plans typically have a higher premium. On the other hand, if you prefer a lower monthly premium, you can choose a plan with fewer out-of-pocket costs.

Medigap policies are guaranteed renewable as long as you pay your premium. This means that your coverage will continue year after year, as long as you make your payments. However, in some states, insurance companies may refuse to renew a Medigap policy purchased before 1992.

Cancer Medication: Are You Covered by Your Insurance?

You may want to see also

Frequently asked questions

Medicaid is a joint federal and state program that provides health coverage for low-income individuals, families, children, pregnant women, the elderly, and people with disabilities.

Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from a private health insurance company to help cover out-of-pocket costs in Original Medicare (Part A and B).

Yes, it is possible to have both Medicaid and Medicare Supplement Insurance, known as being "dual eligible." However, it is important to carefully assess your healthcare needs and ensure that there is no unnecessary duplication of coverage.

Enrollment in Medicaid depends on meeting your state's eligibility requirements, which typically include income and residency rules. For Medicare Supplement Insurance, you can purchase a plan from any licensed insurance company in your state, but you must already have Original Medicare (Part A and/or B).

Medicaid offers benefits not typically covered by Medicare, such as nursing home care and personal care services. Medicare Supplement Insurance can help fill gaps in Original Medicare coverage, such as copayments, deductibles, and coinsurance.