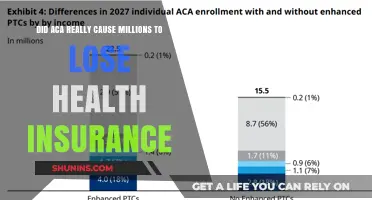

The debate surrounding the public option in healthcare has sparked intense discussions about its potential impact on the private insurance market. Proponents argue that a public option could increase competition, drive down costs, and provide a safety net for those underserved by private plans. However, critics warn that it could undermine private insurers by offering a more affordable alternative, potentially leading to market consolidation or even the collapse of private health insurance. This raises critical questions about the balance between accessibility and sustainability in the healthcare system, as well as the role of government intervention in a traditionally private sector.

Explore related products

What You'll Learn

- Impact on Premiums: Lower costs may attract more consumers, undercutting private insurers' pricing models

- Market Competition: Increased competition could force private insurers to improve services or exit

- Provider Networks: Public option may limit access to top-tier providers, affecting private plans

- Employer-Sponsored Plans: Businesses might shift to public options, reducing private insurance demand

- Financial Sustainability: Public option’s long-term funding could determine its threat to private insurers

![]()

Impact on Premiums: Lower costs may attract more consumers, undercutting private insurers' pricing models

The introduction of a public health insurance option could significantly disrupt the market dynamics, particularly in terms of premium pricing. By offering lower-cost alternatives, a public option may attract price-sensitive consumers, forcing private insurers to reevaluate their pricing models. This shift could lead to a competitive environment where private insurers must either lower their premiums or risk losing market share. For instance, if a public option reduces premiums by 20-30%, as some studies suggest, private insurers might need to cut their rates by a similar margin to remain competitive, especially among younger, healthier individuals who are less likely to require extensive medical services.

Consider the potential ripple effects on consumer behavior. Lower premiums from a public option could incentivize individuals to switch from private plans, particularly those who are currently uninsured or underinsured due to high costs. This migration could create a healthier risk pool for the public option, further stabilizing its costs and enabling additional premium reductions. Conversely, private insurers might face an adverse selection problem, where their remaining policyholders are older or sicker, driving up their costs and necessitating higher premiums. This vicious cycle could accelerate the erosion of private insurers' market share, particularly in regions where the public option gains strong traction.

To mitigate these risks, private insurers might adopt strategies such as narrowing provider networks, increasing cost-sharing through higher deductibles or copays, or focusing on niche markets like supplemental insurance. However, these measures could alienate consumers, further driving them toward the public option. For example, a family of four earning $70,000 annually might find a public option with a $1,200 monthly premium and $2,000 deductible more appealing than a private plan costing $1,600 monthly with a $4,000 deductible, even if the private plan offers a broader network. This comparison underscores the challenge private insurers face in balancing affordability with comprehensive coverage.

A critical takeaway is that the impact on premiums extends beyond immediate cost reductions. It influences long-term market sustainability and consumer choices. Policymakers must carefully design the public option to avoid unintended consequences, such as destabilizing the private insurance market. For consumers, understanding these dynamics can help in making informed decisions, such as comparing not just premiums but also out-of-pocket costs, network adequacy, and coverage limits. Ultimately, the interplay between public and private options will shape the future of health insurance affordability and accessibility.

Affordable Medical Insurance in NJ: Where to Get Covered

You may want to see also

Explore related products

![]()

Market Competition: Increased competition could force private insurers to improve services or exit

The introduction of a public option in health insurance markets would inject a formidable competitor into an industry often criticized for high costs and limited consumer choice. Private insurers, accustomed to operating within a relatively insulated market, would face direct pressure to enhance their offerings or risk losing market share. This dynamic mirrors the effects of competition in other sectors, where the presence of a robust alternative forces incumbent players to innovate, reduce prices, or improve customer service to remain viable. For instance, the entry of generic drugs into pharmaceutical markets has historically driven down prices and expanded access, demonstrating how competition can catalyze positive change.

Consider the mechanics of this competitive pressure. A public option, backed by government resources and potentially lower administrative costs, could offer more affordable premiums and comprehensive coverage. Private insurers, to avoid being undercut, might need to streamline their operations, negotiate lower provider rates, or eliminate unnecessary fees. For example, if a public plan offers a premium that is 20% lower than the private market average, insurers might be compelled to reduce their administrative overhead from the current industry average of 12-18% to a more competitive 8-10%. Such adjustments would not only benefit consumers but also push the industry toward greater efficiency.

However, the outcome of this competition is not guaranteed to favor consumers uniformly. Smaller or less capitalized insurers might struggle to adapt, leading to market consolidation or exits. While this could reduce choice in the short term, the remaining insurers would likely operate under heightened scrutiny and competitive pressure, ensuring sustained improvements. For instance, in states with robust Medicaid programs, private insurers have often responded by expanding their networks and reducing out-of-pocket costs to retain customers. This suggests that even the threat of competition from a public option could spur proactive changes.

To maximize the benefits of this competitive dynamic, policymakers should design the public option with clear benchmarks for affordability and quality. For example, tying public option premiums to a percentage of regional income levels (e.g., 8% of median household income) could create a tangible standard for private insurers to meet. Additionally, requiring transparency in pricing and service quality would empower consumers to make informed choices, further intensifying competitive pressures. Without such safeguards, private insurers might resort to tactics like narrowing provider networks or increasing deductibles, undermining the intended benefits of competition.

Ultimately, the public option’s impact on private insurance hinges on its ability to reshape market incentives. By forcing private insurers to compete on price, quality, and accessibility, it could drive systemic improvements that benefit all consumers. However, success requires careful implementation and ongoing oversight to ensure that competition translates into tangible gains rather than unintended consequences. As with any market intervention, the devil is in the details—but when executed thoughtfully, increased competition has the potential to transform health insurance for the better.

Aetna Insurance: Accepted at Hershey Medical Center?

You may want to see also

Explore related products

![]()

Provider Networks: Public option may limit access to top-tier providers, affecting private plans

A public option could inadvertently reshape the healthcare landscape by altering the dynamics of provider networks, potentially limiting access to top-tier providers for both public and private plan holders. This shift would occur as high-demand specialists and hospitals, facing lower reimbursement rates from the public option, might opt to exclude themselves from its network. Such a scenario could create a ripple effect, where private insurers, struggling to maintain competitive networks, are forced to either reduce their own provider lists or increase premiums to retain access to these top-tier providers. For patients, this could mean fewer choices, longer wait times, and a fragmented care experience, particularly for those with complex or chronic conditions requiring specialized care.

Consider the practical implications for a 45-year-old patient with a rare autoimmune disorder. Under the current system, they might have access to a renowned rheumatologist through their private plan. However, if the public option drives down reimbursement rates, this specialist could decide to limit their practice to private-pay or high-end private insurance patients, leaving public option enrollees—and potentially those on lower-tier private plans—with fewer options. This stratification of care could exacerbate existing health disparities, as those with means continue to access top-tier providers while others face barriers to critical care.

To mitigate this risk, policymakers could implement tiered reimbursement models that incentivize providers to participate in the public option without compromising their financial viability. For instance, offering higher reimbursement rates for providers who agree to accept a minimum percentage of public option patients could balance access and sustainability. Additionally, private insurers could be required to maintain a baseline level of top-tier providers in their networks, ensuring that competition from the public option doesn’t lead to a race to the bottom in terms of provider quality.

A comparative analysis of countries with mixed public-private healthcare systems, such as Germany or Switzerland, reveals that strong regulatory oversight and transparent reimbursement policies can prevent provider network fragmentation. In Germany, for example, providers are required to treat both public and private patients, ensuring broad access to high-quality care. Adopting similar safeguards in the U.S. context could preserve access to top-tier providers while allowing the public option to fulfill its intended role of expanding coverage and reducing costs.

Ultimately, the success of a public option hinges on its ability to coexist with private insurance without undermining provider networks. By addressing reimbursement disparities, implementing regulatory safeguards, and fostering collaboration between public and private sectors, policymakers can ensure that the introduction of a public option enhances, rather than diminishes, access to top-tier care. Patients deserve a system where the choice of insurance doesn’t dictate the quality of care they receive—a goal achievable through thoughtful design and proactive measures.

Navigating Dual Coverage: Medicaid and ACA Insurance Options

You may want to see also

Explore related products

![]()

Employer-Sponsored Plans: Businesses might shift to public options, reducing private insurance demand

Employer-sponsored health insurance has long been a cornerstone of the American healthcare system, covering approximately 157 million workers and their families. However, the introduction of a robust public option could incentivize businesses to reevaluate their commitment to private plans. For small and medium-sized enterprises (SMEs), which often struggle with rising premiums, the public option might offer a cost-effective alternative. A 2020 Kaiser Family Foundation survey revealed that 49% of SMEs reported difficulty affording health insurance, suggesting a ripe environment for such a shift. If businesses opt for the public option, private insurers could lose a significant portion of their customer base, potentially destabilizing their market dominance.

Consider the financial calculus for employers. Private health insurance premiums have increased by 55% over the past decade, outpacing inflation and wage growth. In contrast, a public option could cap premiums at a percentage of income or offer standardized, lower-cost plans. For instance, a mid-sized tech company with 200 employees might save upwards of $500,000 annually by transitioning to a public option, assuming a 20% reduction in per-employee costs. Such savings could be reinvested in wages, benefits, or business growth, creating a compelling case for businesses to make the switch. However, this transition would require careful planning to ensure employees maintain comparable coverage levels.

Critics argue that a mass exodus from private insurance could lead to adverse selection, where healthier individuals opt for the public option, leaving private insurers with a sicker, costlier population. Yet, this concern overlooks the role of employer mandates and employee preferences. Many workers value the comprehensiveness of employer-sponsored plans, which often include dental, vision, and wellness benefits not typically covered by public options. Businesses might therefore adopt a hybrid approach, offering the public option as one of several choices, allowing employees to decide based on their needs. This flexibility could mitigate risks while still reducing private insurance demand.

The implications for private insurers are profound. If large employers, which account for 60% of the private insurance market, begin to shift toward public options, insurers would need to adapt by diversifying their product offerings or reducing administrative costs. Some might focus on supplemental plans, such as those covering elective procedures or premium care, to remain competitive. However, smaller insurers with limited resources could face existential threats, potentially leading to industry consolidation. Policymakers must therefore balance the benefits of expanded public options with measures to ensure a stable, competitive insurance market.

In practical terms, businesses considering this transition should follow a structured approach. First, conduct a cost-benefit analysis comparing private plans to the public option, factoring in employee contributions and coverage differences. Second, engage with employees through surveys or focus groups to gauge their preferences and concerns. Third, consult legal and financial advisors to navigate regulatory requirements and potential tax implications. Finally, implement a phased rollout, starting with voluntary enrollment periods to monitor uptake and adjust strategies accordingly. By taking these steps, businesses can make informed decisions that benefit both their bottom line and their workforce.

Accident Insurance: Is It Pre-Tax?

You may want to see also

Explore related products

![]()

Financial Sustainability: Public option’s long-term funding could determine its threat to private insurers

The financial sustainability of a public health insurance option hinges on its funding model, which could either complement or undermine private insurers. A well-structured public option, funded through a mix of premiums, taxes, and government subsidies, could operate efficiently without relying on profit margins. For instance, Medicare in the U.S. has maintained solvency for decades by leveraging economies of scale and negotiating lower provider rates. If a public option replicates this model, it could offer competitive premiums, attracting price-sensitive consumers without destabilizing private markets. However, if funding is inadequate or subject to political whims, the public option might require bailouts, creating an uneven playing field that could drive private insurers out of the market.

Consider the funding mechanisms critically. A public option funded solely through premiums might struggle to cover costs for high-risk populations, necessitating cross-subsidies from healthier enrollees. This could lead to adverse selection, where private insurers retain only the healthiest (and most profitable) customers. Alternatively, a hybrid funding model, such as a payroll tax combined with premiums, could ensure stable revenue while mitigating political risks. For example, Switzerland’s public-private hybrid system uses cantonal taxes and premiums to fund basic coverage, allowing private insurers to compete for supplemental plans. Such a model balances financial sustainability with market competition, reducing the threat to private insurers.

Long-term funding stability is not just about revenue sources but also cost control. A public option could reduce administrative overhead by streamlining billing and claims processing, potentially saving 10-15% of total costs compared to private insurers. However, without robust mechanisms to control provider reimbursement rates or drug pricing, costs could spiral. For instance, if a public option pays providers at Medicare rates (typically 20-30% below private rates), hospitals might shift costs to private insurers, raising their premiums and making the public option more attractive by default. This cost-shifting dynamic could erode private insurers’ market share over time.

To ensure financial sustainability without destroying private insurance, policymakers must design funding mechanisms that align incentives. One approach is to cap public option enrollment or limit its availability to specific populations, such as the uninsured or those in underserved areas. Another strategy is to require private insurers to participate in a risk-adjustment pool, redistributing profits from low-risk plans to high-risk ones. For example, the Affordable Care Act’s risk corridor program (though flawed in execution) aimed to stabilize markets during transitions. By combining such measures with transparent funding formulas, a public option can compete fairly, preserving choice while addressing affordability.

Ultimately, the threat a public option poses to private insurers depends on its financial design, not its mere existence. A sustainably funded public option could drive innovation and efficiency in the private sector by setting benchmarks for cost and quality. Conversely, an underfunded or poorly structured program could create market distortions, leading to private insurer exits. Policymakers must therefore prioritize long-term fiscal responsibility, ensuring the public option neither crowds out private competition nor becomes a financial burden on taxpayers. Striking this balance is key to achieving universal coverage without dismantling the private insurance market.

Understanding Medical Unemployment Insurance Appeal Requirements

You may want to see also

Frequently asked questions

The public option is a government-run health insurance plan that would compete alongside private insurance plans, offering an alternative for individuals and businesses.

While the public option could reduce the market share of private insurers, it is unlikely to "destroy" them entirely. Private insurance may adapt by offering specialized plans or additional services to remain competitive.

Critics argue that a public option, with lower administrative costs and government backing, could outcompete private insurers, potentially driving them out of the market over time.

Not necessarily. The public option is a step toward expanding coverage, but it does not eliminate private insurance. A single-payer system would replace private insurance entirely, which is a separate policy proposal.

Private insurers could survive by offering supplemental plans, better customer service, or specialized coverage options that the public option does not provide, ensuring they remain relevant in the market.