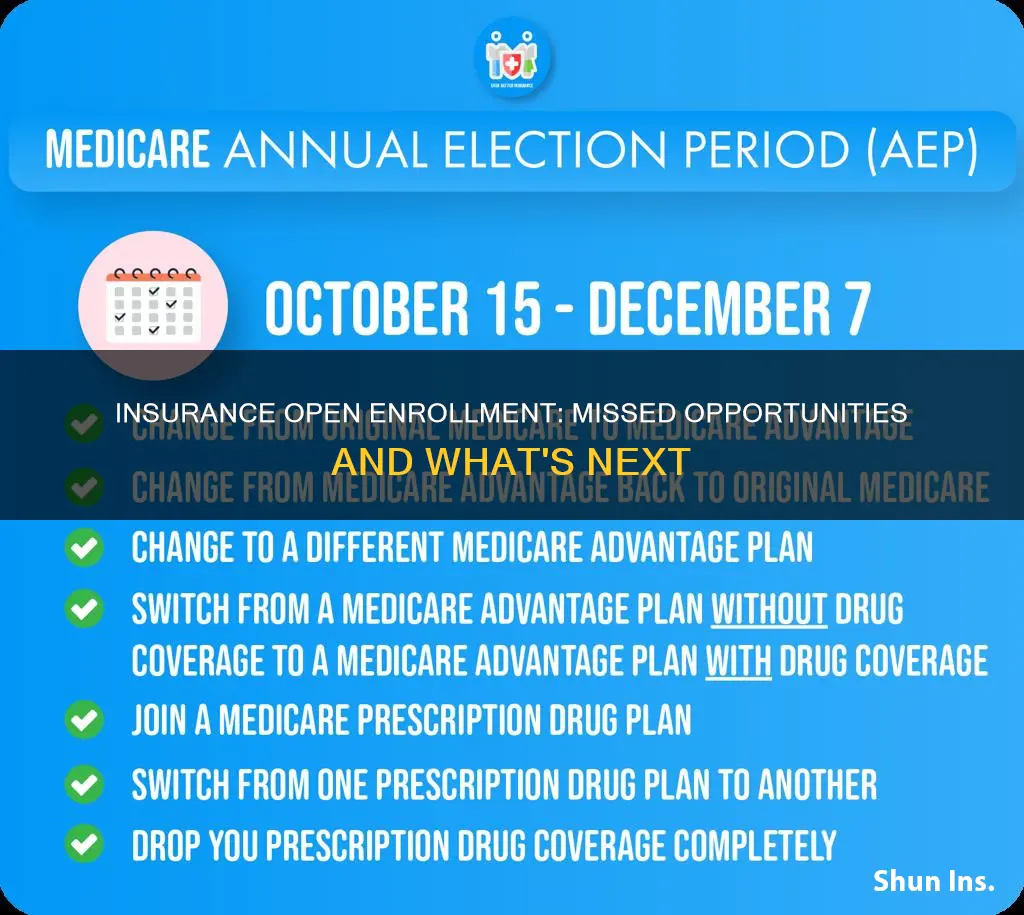

If you missed the open enrollment period for health insurance, you may be worried about your coverage options. While it's true that open enrollment is the only time of year when you can freely opt in or out of plans or make changes to your health benefits, there are still options available to you outside of this window. Firstly, it's important to confirm your benefits enrollment dates, as these differ depending on where you get your coverage. If you missed the standard enrollment window, you may still be able to enroll through your employer, who can advise on special enrollment periods. You may also qualify for a Special Enrollment Period if you've had certain life events, including losing health coverage, moving, getting married, having a baby, or adopting a child, or if your household income is below a certain amount. Additionally, you could explore other options like short-term health insurance, Medicaid, or CHIP, although these options may not provide comprehensive coverage.

| Characteristics | Values |

|---|---|

| Open enrollment period | Typically once a year |

| Missed open enrollment | Limited options for coverage |

| Coverage options | Policies not regulated by the Affordable Care Act (ACA), supplemental coverage, short-term plans, Medicaid, Children's Health Insurance Program (CHIP), accident supplements, critical illness policies, fixed indemnity plans, dental/vision plans, medical discount plans |

| Special Enrollment Period | Qualifying life events such as losing health coverage, moving, getting married, having a baby, adopting a child, decrease in household income, death of someone on the Marketplace plan |

| ACA-compliant plans | Available during open enrollment or with a Special Enrollment Period |

Explore related products

What You'll Learn

![]()

Qualifying for a Special Enrollment Period

If you missed the Open Enrollment Period, you can still qualify for a Special Enrollment Period. This is a period of time outside of the yearly Open Enrollment when you can enrol in or change your health insurance plan. This is typically available if you've experienced certain life events or if your household income is below a certain amount.

Firstly, you may qualify for a Special Enrollment Period if you've had certain life changes, including losing health coverage, moving, getting married, having a baby, or adopting a child. For example, if you lose your health coverage because your individual plan is discontinued or you are no longer a dependent on a parent or guardian's plan. You may also qualify if you lose your coverage due to a serious medical condition, natural disaster, or other emergencies.

Secondly, you may qualify for a Special Enrollment Period if your household income is below a certain amount. This could be due to a decrease in household income, making you eligible for savings on a Marketplace plan.

It's important to note that if you lose your coverage because you didn't provide the required documents or chose to drop your coverage, you typically won't qualify for a Special Enrollment Period.

If you missed your employer's open enrollment window, you should contact your benefits team to discuss your options and determine if you qualify for a Special Enrollment Period. Additionally, you may consider enrolling in individual supplemental insurance plans directly through an insurance provider, although you may lose out on discounted rates offered by your employer.

Healthcare Insurance: Unaffordable for Many

You may want to see also

Explore related products

![]()

Short-term health insurance

If you missed the open enrollment period and couldn't afford insurance, you may still have options for coverage outside of the Affordable Care Act (ACA). Short-term health insurance, also known as temporary health insurance, can be an option to consider. Here are some key things to know about short-term health insurance:

Coverage and Eligibility

Duration and Availability

Cost and Affordability

Enrollment and Effectiveness

In summary, short-term health insurance can be a viable option if you missed the open enrollment period and need temporary coverage. These plans offer flexibility and affordability but may have limitations in terms of benefits and eligibility. Be sure to carefully review the terms and conditions of any short-term health insurance plan before enrolling to ensure it meets your specific needs and requirements.

Unveiling the NCB: A Rewarding Feature of Insurance Policies

You may want to see also

Explore related products

![]()

Medicaid and CHIP

If you missed the open enrollment period for health insurance, you may still have options for coverage outside of the Affordable Care Act (ACA) marketplace. One option is Medicaid, which provides free or low-cost health coverage to eligible low-income individuals, including families and children, pregnant women, the elderly, and people with disabilities. The federal poverty level (FPL) is used to determine eligibility for Medicaid, and this varies from state to state. For example, some states have expanded their Medicaid programs to cover all people with household incomes below a certain level, while others have not. Even if your income is too high to qualify for Medicaid, you may still be able to get coverage through the Children's Health Insurance Program (CHIP). CHIP provides low-cost health coverage to children and, in some cases, pregnant women in families that earn too much money to qualify for Medicaid but cannot afford private coverage. Like Medicaid, CHIP is managed by states according to federal requirements and is funded jointly by states and the federal government.

You can apply for Medicaid and CHIP at any time of year, and there are no limited enrollment windows. However, certain qualifications must be met, and these vary depending on the state. For example, in some states, CHIP only provides coverage to children, while in others it may also cover pregnant women. To find out if you qualify for Medicaid or CHIP, you can enter your household size and state to determine if you might be eligible. If it appears that you qualify, your information will be sent to your state agency, who will contact you about enrollment.

If you miss the open enrollment period for health insurance and are not eligible for Medicaid or CHIP, your options for coverage are limited. You may be able to purchase a short-term plan, but these are not ACA-compliant, and your eligibility would depend on your medical history. Alternatively, you may be able to enroll in individual supplemental insurance plans directly through an insurance provider, although you may lose out on discounted rates offered by some employers.

Self-Insured in Texas: Steps to Take for Financial Freedom

You may want to see also

Explore related products

![]()

Employer-sponsored coverage

If you missed the open enrollment period for employer-sponsored coverage, you may still have options to secure health insurance. Firstly, it's important to understand that open enrollment periods occur annually and are typically offered by employers or the insurance marketplace. If you already have employer-sponsored coverage, your existing plan may automatically continue into the next benefits period. However, if you don't have existing coverage, you might enter the next period without insurance. Therefore, it is crucial to confirm your benefits enrollment dates with your employer.

If you missed the open enrollment period, you can explore the following options:

- Contact your benefits team: Speak to your benefits team at work to discuss other available options. They can guide you through the terms and qualifications associated with a special enrollment period. This is a time outside the yearly open enrollment period when you can sign up for health insurance under specific circumstances.

- Special enrollment periods: Special enrollment periods allow employees to make changes to their coverage, including enrolling in a plan, adding or removing family members, or switching plans. These periods are often linked to qualifying life events, such as losing health coverage, moving, getting married, having a baby, or adopting a child.

- Individual supplemental insurance plans: If you are unable to enroll in a spouse's plan, you can consider individual supplemental insurance plans directly through an insurance provider. However, you may lose out on discounted rates typically associated with employer-provided plans.

- Short-term health insurance: You may be able to purchase short-term health insurance from a private insurance provider. However, note that not all states offer short-term coverage, and your eligibility will depend on your medical history.

- Medicaid or CHIP: Explore options like Medicaid or the Children's Health Insurance Program (CHIP). While they don't have limited enrollment windows, you will need to meet certain qualifications to be eligible.

Remember, it is essential to understand the specific rules and regulations surrounding employer-sponsored coverage and special enrollment periods. These rules can vary from one employer to another, and it's important to stay informed about your benefits and enrollment dates to make informed decisions regarding your health insurance coverage.

The Legal Definition of Common Carrier and Its Impact on Insurance Policies

You may want to see also

Explore related products

![]()

Non-ACA-compliant coverage

If you missed the open enrollment period, you may still have several options for obtaining health insurance. However, these options are typically limited to policies that are not regulated by the Affordable Care Act (ACA) and are thus not considered minimum essential coverage. These non-ACA-compliant plans are offered outside the ACA marketplaces and may be cheaper, but they come with significant risks. Insurers selling these plans can ask about your health history, exclude benefits like prescription drugs or mental health services, drop you if you get sick, or increase your premiums due to pre-existing conditions.

- Short-term health insurance (exempt from ACA rules as it is not considered individual health insurance).

- Accident supplements.

- Fixed-dollar indemnity plans.

- Dental/vision plans.

- Critical illness insurance policies.

- Travel insurance.

- Medical discount plans.

- Limited-benefit plans.

- Critical/specific-illness policies.

- Fixed indemnity plans.

It is important to note that these non-ACA-compliant plans do not fulfill the mandate requiring individuals to have health insurance, and there may be state-imposed penalties for not having minimum essential coverage. Additionally, short-term health insurance is not available in states like DC, New Jersey, California, Massachusetts, and Rhode Island.

If you missed the open enrollment period, you may also qualify for a Special Enrollment Period if you experience certain life events, such as losing health coverage, moving, getting married, having a baby, or adopting a child. Additionally, if your household income is below a certain level, you may qualify for Medicaid or CHIP, which have enrollment options throughout the year.

Humana Insurance: Understanding Your Policy and Coverage Status

You may want to see also

Frequently asked questions

Your options for coverage are limited to policies that are not regulated by the Affordable Care Act (ACA) and are thus not considered minimum essential coverage. These include short-term health insurance, fixed indemnity plans, critical illness plans, health care sharing ministry plans, accident supplements, and more. These plans are available year-round but may not provide comprehensive coverage.

You may qualify for a Special Enrollment Period if you have experienced certain life events, such as losing health coverage, moving, getting married, having a baby, or adopting a child. Additionally, if your household income is below a certain amount, you may also be eligible for a Special Enrollment Period.

Some alternatives include short-term health insurance, Medicaid, or the Children's Health Insurance Program (CHIP). Faith-based health-sharing plans and concierge medicine (direct primary care) are other options that provide a communal way to share healthcare costs or offer affordable routine health services without comprehensive coverage.