Cato, a diligent and health-conscious individual, recently embarked on a quest to secure comprehensive health insurance coverage. As someone who values well-being and financial security, Cato understood the importance of finding a plan that aligns with their needs and budget. Navigating the complex landscape of health insurance options, Cato meticulously researched various providers, compared policies, and sought advice from trusted sources. Their journey highlights the challenges and considerations many face when trying to find the right health insurance, from understanding deductibles and premiums to evaluating network coverage and additional benefits. Cato’s experience serves as a relatable example for anyone seeking to make informed decisions about their healthcare protection.

| Characteristics | Values |

|---|---|

| Organization | Cato Institute |

| Focus | Health Insurance, Healthcare Policy |

| Key Findings | Cato's research highlights issues with government-run healthcare systems, advocates for free-market solutions, and critiques the Affordable Care Act (ACA). |

| Publications | Numerous policy papers, articles, and studies on healthcare reform, insurance mandates, and market-based alternatives. |

| Stance on Individual Mandate | Opposes government mandates requiring individuals to purchase health insurance. |

| Support for Free-Market Solutions | Advocates for consumer-driven healthcare, Health Savings Accounts (HSAs), and deregulation to increase competition and lower costs. |

| Criticism of ACA | Argues that the ACA has increased premiums, reduced choice, and failed to control healthcare costs effectively. |

| Alternative Proposals | Supports reforms like allowing interstate insurance sales, expanding HSAs, and transitioning to a more market-oriented system. |

| Recent Data (as of latest research) | Continues to publish studies showing the inefficiencies of government-heavy healthcare systems and the benefits of market-based reforms. |

| Notable Researchers | Scholars like Michael F. Cannon and others contribute to Cato's healthcare policy analysis. |

| Impact | Influences libertarian and conservative policy debates on healthcare reform in the U.S. |

Explore related products

What You'll Learn

- Cato's stance on health insurance mandates and individual responsibility in healthcare coverage

- Analysis of Cato's research on free-market solutions for health insurance systems

- Cato's critique of government-run health insurance programs and their inefficiencies

- How Cato addresses the role of employer-based health insurance in the U.S?

- Cato's perspective on health insurance affordability and consumer choice in the market

![]()

Cato's stance on health insurance mandates and individual responsibility in healthcare coverage

The Cato Institute, a libertarian think tank, staunchly opposes health insurance mandates as a violation of individual liberty. They argue that forcing individuals to purchase a product—even one as essential as health insurance—infringes on personal autonomy. This stance aligns with their broader philosophy of minimizing government intervention in personal decisions. Cato scholars contend that mandates distort the insurance market, driving up costs and reducing consumer choice. For instance, they highlight how the Affordable Care Act’s individual mandate led to inflated premiums, particularly for younger, healthier individuals who might have preferred less comprehensive, more affordable plans.

To address the issue of uninsured individuals, Cato advocates for a market-based approach centered on individual responsibility. They propose removing regulatory barriers that limit the availability of low-cost, high-deductible plans, which could appeal to those who currently forgo coverage. Additionally, they suggest expanding health savings accounts (HSAs) to empower individuals to save for medical expenses tax-free, fostering a culture of personal financial responsibility in healthcare. Cato also emphasizes the role of charitable care and community-based solutions, arguing that these mechanisms can provide a safety net without coercive mandates.

A critical aspect of Cato’s argument is their comparison of health insurance mandates to other compulsory purchases. They draw parallels to hypothetical scenarios, such as mandating the purchase of gym memberships to promote public health, to illustrate the slippery slope of government overreach. By framing mandates as an assault on freedom, Cato seeks to persuade readers that individual responsibility, not coercion, should drive healthcare decisions. This comparative approach underscores their belief that personal choice, even with its risks, is preferable to centralized control.

Practically, Cato’s stance offers a roadmap for policymakers seeking alternatives to mandates. For example, they recommend deregulating the insurance market to allow for more innovative, consumer-friendly products. They also advocate for tort reform to reduce defensive medicine costs and propose block-granting Medicaid to states, giving them flexibility to design programs that better meet local needs. These steps, Cato argues, would lower costs and increase access without compromising individual liberty. However, critics caution that such an approach could leave vulnerable populations uninsured, highlighting the tension between freedom and equity in healthcare.

In conclusion, Cato’s position on health insurance mandates and individual responsibility is rooted in a deep commitment to libertarian principles. While their proposals offer a vision of a more market-driven healthcare system, they also raise important questions about societal obligations to ensure access to care. For those considering Cato’s ideas, the key takeaway is balancing personal freedom with the collective goal of a healthier population—a challenge that requires careful consideration of both philosophical and practical implications.

Dave Ramsey's Recommended Medical Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Analysis of Cato's research on free-market solutions for health insurance systems

Cato's research on free-market solutions for health insurance systems reveals a consistent emphasis on deregulation, consumer choice, and competition as the primary drivers of affordability and quality. By examining historical examples, such as the pre-1960s U.S. healthcare market, Cato argues that government intervention—through mandates, subsidies, and third-party payer systems—has inflated costs and reduced transparency. For instance, the rise of employer-sponsored insurance, incentivized by tax breaks in 1943, disconnected consumers from the true cost of care, leading to overutilization and price distortion. Cato’s analysis suggests that restoring a direct payer-provider relationship, coupled with health savings accounts (HSAs), could empower individuals to make cost-conscious decisions, thereby driving market efficiency.

One of Cato’s key recommendations is the elimination of state and federal insurance mandates, which currently dictate minimum coverage requirements. These mandates, while well-intentioned, often force consumers to purchase comprehensive plans they neither need nor want, particularly younger, healthier individuals. Cato cites data showing that states with fewer mandates have lower premiums—for example, a 2018 study found that removing just four common mandates could reduce premiums by up to 20%. The think tank advocates for a shift toward customizable, à la carte policies, allowing consumers to prioritize coverage based on personal risk profiles and financial circumstances.

Cato also highlights the potential of association health plans (AHPs) and interstate insurance sales to expand competition. By permitting small businesses and individuals to band together across state lines, AHPs could negotiate lower rates and bypass restrictive state regulations. However, Cato cautions that such reforms must avoid creating new dependencies on government oversight. Instead, they propose a framework where private entities, such as professional associations or trade groups, act as intermediaries, ensuring accountability through market forces rather than bureaucratic intervention.

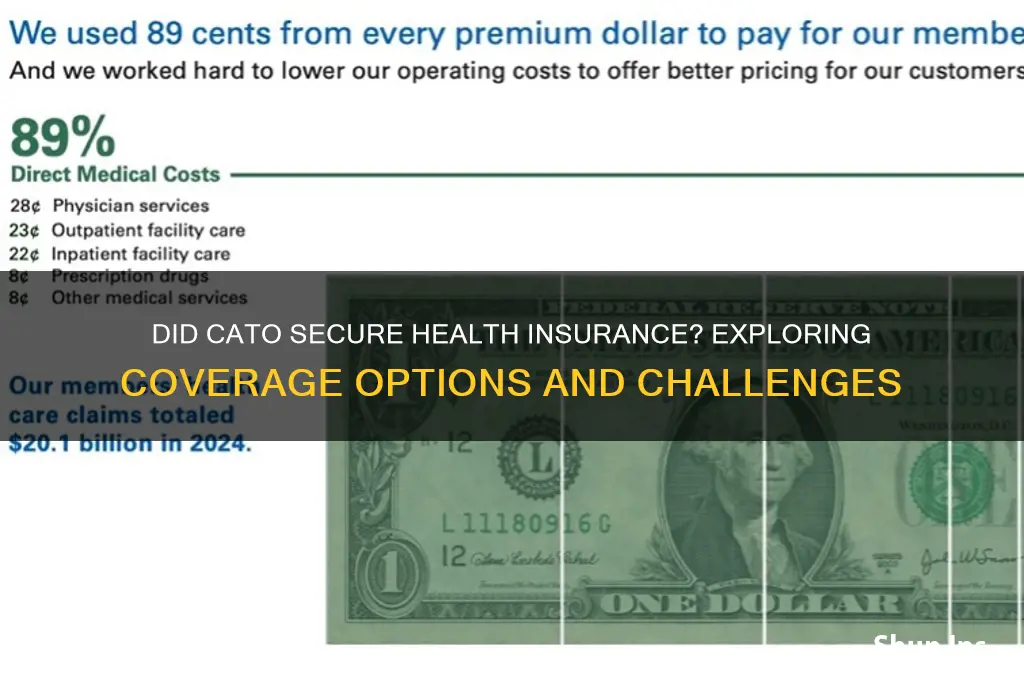

A critical takeaway from Cato’s research is the role of price transparency in a free-market health insurance system. The current lack of clear pricing information prevents consumers from making informed decisions, perpetuating a cycle of high costs. Cato points to successful examples like surgery centers in Oklahoma, which post prices online and offer bundled payments, resulting in costs 30-50% lower than traditional hospitals. Implementing similar transparency measures across the industry, Cato argues, would incentivize providers to compete on price and quality, ultimately benefiting consumers.

While Cato’s free-market approach offers a compelling alternative to the status quo, it is not without challenges. Critics argue that deregulation could leave vulnerable populations without adequate coverage, particularly those with pre-existing conditions. Cato counters by proposing targeted safety nets, such as high-risk pools funded by a combination of state and private resources, rather than broad-based subsidies. Practical implementation would require careful balancing of market freedoms with safeguards to ensure access for all, a delicate task that Cato’s research acknowledges but does not fully resolve.

Understanding Medical Insurance Rebates and Government Returns

You may want to see also

Explore related products

![]()

Cato's critique of government-run health insurance programs and their inefficiencies

Cato's critique of government-run health insurance programs hinges on their inherent inefficiencies, which stem from bureaucratic rigidity and misaligned incentives. Unlike private markets, where competition drives innovation and cost control, government programs often operate under one-size-fits-all mandates that stifle flexibility. For instance, Medicare’s fee-for-service model incentivizes quantity over quality, leading to unnecessary procedures and inflated costs. Cato argues that this structural flaw not only wastes taxpayer dollars but also compromises patient care by limiting personalized treatment options.

Consider the example of wait times in single-payer systems, a common inefficiency Cato highlights. In Canada, patients often face months-long delays for specialist referrals or elective surgeries, a direct consequence of centralized resource allocation. While proponents argue this ensures universal access, Cato counters that such delays can exacerbate health conditions, ultimately negating the program’s intended benefits. For Americans aged 65 and older, who rely heavily on Medicare, similar inefficiencies could mean delayed diagnoses or suboptimal care, particularly in rural areas with fewer providers.

To address these inefficiencies, Cato advocates for market-based reforms that empower consumers and providers. One practical tip is to introduce Health Savings Accounts (HSAs) paired with high-deductible plans, which encourage individuals to make cost-conscious healthcare decisions. For families, this could mean allocating $2,000–$3,000 annually into an HSA to cover routine expenses while ensuring catastrophic coverage. Cato also suggests expanding telemedicine and removing state licensing barriers to increase provider competition, a move that could reduce costs by up to 30% for common services like consultations.

A comparative analysis further underscores Cato’s point. Switzerland’s healthcare system, which relies on private insurers regulated by the government, achieves universal coverage without the inefficiencies of fully government-run models. Premiums are high, but subsidies for low-income individuals ensure affordability, and wait times are minimal. This hybrid approach aligns with Cato’s emphasis on leveraging market forces while maintaining a safety net, offering a blueprint for reform that avoids the pitfalls of centralized systems.

In conclusion, Cato’s critique is not merely ideological but grounded in observable inefficiencies that hinder government-run health insurance programs. By focusing on bureaucratic rigidity, misaligned incentives, and practical alternatives, their argument provides a roadmap for improving healthcare delivery. For policymakers and consumers alike, the takeaway is clear: market-driven solutions, when properly regulated, can offer both efficiency and accessibility, addressing the shortcomings of centralized systems.

Understanding CDHP Health Insurance: Benefits, Costs, and How It Works

You may want to see also

Explore related products

![]()

How Cato addresses the role of employer-based health insurance in the U.S

The Cato Institute, a libertarian think tank, critiques employer-based health insurance as a distortion of the free market. They argue that this system, which covers roughly half of Americans, emerged not from consumer preference but from a World War II-era tax loophole. By excluding employer-sponsored health benefits from taxable income, the government inadvertently created a system where individuals are locked into plans chosen by their employers, limiting choice and portability. This historical accident, Cato contends, has led to inefficiencies, reduced wage growth, and a disconnect between consumers and the true cost of healthcare.

Cato proposes a radical shift: decoupling health insurance from employment. Their solution involves eliminating the tax exclusion for employer-sponsored insurance and replacing it with a universal tax credit for individuals to purchase coverage on the private market. This, they argue, would empower consumers to select plans tailored to their needs, fostering competition among insurers and driving down costs. Imagine a scenario where a 35-year-old software engineer, currently tied to her employer's high-deductible plan, could use a tax credit to purchase a more comprehensive policy directly from an insurer, potentially saving money and gaining greater control over her healthcare decisions.

Understanding Your Medical Insurance: Policy Numbers and More

You may want to see also

Explore related products

![]()

Cato's perspective on health insurance affordability and consumer choice in the market

Consider the impact of government intervention on premiums. Cato's research suggests that mandates requiring coverage for specific services, regardless of individual need, artificially inflate costs. For instance, a healthy 25-year-old male might be forced to purchase a plan covering maternity care, driving up his premium by 15-20%. Cato advocates for allowing insurers to offer stripped-down, catastrophic coverage plans, which could reduce premiums for this demographic by up to 50%, making insurance more accessible to those who currently opt out due to cost.

Implementing such a system would require a multi-step approach. First, repeal the Affordable Care Act's individual mandate, freeing individuals to choose whether to purchase insurance. Second, eliminate essential health benefits requirements, enabling insurers to design plans tailored to specific consumer segments. Third, expand Health Savings Accounts (HSAs), allowing individuals to save pre-tax dollars for medical expenses, fostering price sensitivity and encouraging cost-conscious decisions.

Critics argue that deregulation could lead to inadequate coverage and leave vulnerable populations uninsured. However, Cato counters that a truly free market would incentivize insurers to compete on price and quality, driving innovation and accessibility. For example, telemedicine and direct primary care models could emerge as affordable alternatives, providing basic care at a fraction of the cost of traditional insurance.

Ultimately, Cato's vision for health insurance affordability and consumer choice hinges on unleashing market forces and empowering individuals to make informed decisions. While this approach may not be without challenges, it offers a compelling alternative to the status quo, potentially expanding access and reducing costs for millions of Americans. By embracing free-market principles, policymakers can create a system that prioritizes individual liberty and fosters a more dynamic, responsive healthcare market.

Medical Exams for Children's Life Insurance: Are They Necessary?

You may want to see also

Frequently asked questions

Yes, Cato successfully found health insurance after researching various plans and comparing options.

Cato found health insurance by using online marketplaces, consulting with insurance brokers, and comparing quotes from multiple providers.

Cato found a comprehensive health insurance plan that includes coverage for preventive care, prescription drugs, and emergency services, tailored to their specific needs.