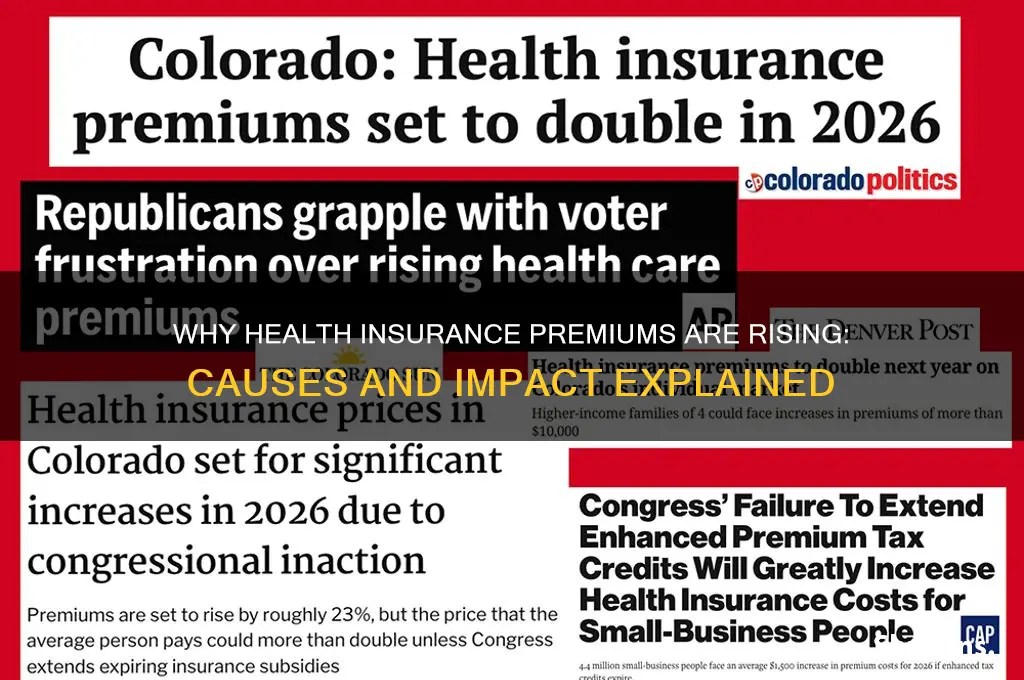

Health insurance costs have been a growing concern for many individuals and families in recent years, with premiums, deductibles, and out-of-pocket expenses seemingly on the rise. The question of whether health insurance has gone up is a pressing one, as it directly impacts household budgets and access to healthcare. Factors such as inflation, rising medical costs, and changes in government policies have all contributed to the increasing financial burden of health insurance. As a result, many people are struggling to keep up with the escalating costs, leading to a closer examination of the trends and drivers behind these increases. Understanding the reasons behind the rise in health insurance costs is essential for individuals, policymakers, and industry stakeholders to develop effective strategies to mitigate the impact and ensure affordable access to healthcare for all.

| Characteristics | Values |

|---|---|

| Trend in Premiums (2023) | Average premiums for employer-sponsored health insurance increased by 7% in 2023, reaching $23,968 annually for family coverage (Kaiser Family Foundation). |

| Individual Market Premiums (2023) | Premiums on the Affordable Care Act (ACA) marketplaces rose by an average of 4% in 2023, though increases varied by state and plan type (Centers for Medicare & Medicaid Services). |

| Key Drivers of Increases | Rising healthcare costs, inflation, increased utilization of services post-pandemic, and drug price hikes. |

| Impact of Inflation | General inflation has contributed to higher administrative and operational costs for insurers. |

| Policy Changes | Some states implemented rate caps or subsidies to mitigate premium increases, while others saw larger hikes due to regulatory changes. |

| Employer Contributions | Employers absorbed a portion of the premium increases, with workers seeing an average 5% rise in their share of premiums in 2023. |

| Medicare Advantage Premiums (2023) | Premiums for Medicare Advantage plans remained stable, with an average monthly premium of $18.50, partly due to government subsidies. |

| State Variations | Premium increases ranged from 2% to 12% across states, with higher increases in states with fewer insurers or higher healthcare costs. |

| Future Outlook (2024) | Early projections suggest premiums may rise by 6-8% in 2024, driven by ongoing economic and healthcare cost pressures. |

Explore related products

What You'll Learn

![]()

Impact of Inflation on Premiums

Inflation’s relentless climb has a domino effect on nearly every sector, and health insurance premiums are no exception. As the cost of medical services, pharmaceuticals, and administrative expenses rise, insurers are forced to adjust their rates to maintain profitability. For instance, between 2021 and 2023, the average annual premium for employer-sponsored family coverage increased by over 4%, outpacing the general inflation rate. This trend isn’t isolated; it reflects a broader economic pressure where rising wages for healthcare workers, expensive medical technology, and higher facility maintenance costs contribute to the upward spiral.

Consider the mechanics of this relationship: inflation drives up the price of everything from hospital supplies to malpractice insurance. Providers then charge more for their services, leaving insurers with higher claims payouts. To offset these costs, premiums must rise. For individuals and families, this means a larger chunk of their budget is allocated to health insurance, often at the expense of other necessities. For example, a 50-year-old nonsmoker might have seen their monthly premium increase from $450 to $520 in just two years, a 15.5% jump that mirrors inflationary pressures.

However, the impact isn’t uniform. Age, location, and plan type play significant roles. Younger individuals, particularly those in their 20s and 30s, may experience smaller premium hikes compared to older adults, who typically require more healthcare services. Similarly, states with higher costs of living, like California or New York, often see steeper premium increases. Practical tip: if you’re shopping for insurance, consider high-deductible health plans (HDHPs) paired with health savings accounts (HSAs). While premiums may still rise, HDHPs generally have lower monthly costs, and HSAs offer tax advantages to offset out-of-pocket expenses.

To mitigate the impact, policyholders should review their plans annually during open enrollment. Look for opportunities to switch to a more cost-effective plan or negotiate with employers for better group rates. Additionally, leveraging preventive care services—often fully covered—can reduce long-term healthcare costs, indirectly easing the burden of rising premiums. For instance, a 40-year-old who regularly uses covered preventive screenings may avoid costly treatments later, effectively lowering their overall healthcare spend.

In conclusion, inflation’s grip on health insurance premiums is both direct and multifaceted. While the trend is unlikely to reverse, understanding its drivers and adopting strategic measures can help individuals navigate this financial challenge. Whether through plan adjustments, employer negotiations, or proactive health management, staying informed and proactive is key to minimizing the impact of inflation on your healthcare costs.

Aetna vs. Humana: Which Medicare Insurance is Better?

You may want to see also

Explore related products

![]()

Policy Changes and Rate Hikes

Health insurance premiums have been on a steady upward trajectory, leaving many policyholders wondering about the driving forces behind these rate hikes. A significant contributor to this trend is the evolving landscape of healthcare policies, which often triggers a ripple effect on insurance costs. When governments introduce new regulations or mandates, insurers must adapt, and these adjustments frequently translate to higher premiums. For instance, the expansion of essential health benefits under the Affordable Care Act (ACA) in the United States required insurers to cover a broader range of services, from maternity care to mental health treatment. While this improved access to care, it also increased the overall cost structure for insurance providers, who then passed these expenses on to consumers.

Consider the impact of policy changes on specific demographics. For young adults aged 26 and under, the ACA’s provision allowing them to remain on their parents’ insurance plans delayed their entry into the individual market, reducing the number of healthy, low-cost enrollees. This shift altered the risk pool, as older, sicker individuals became a larger proportion of policyholders, driving up average costs. Similarly, mandates requiring coverage for pre-existing conditions, while essential for equity, have contributed to rate increases as insurers account for higher expected claims. Understanding these dynamics is crucial for policyholders to grasp why their premiums rise, even when their personal health status remains unchanged.

From a practical standpoint, policyholders can take proactive steps to mitigate the impact of rate hikes. First, review your plan annually during open enrollment to ensure it still meets your needs at the best available price. Insurers often adjust their offerings, and a plan that was cost-effective last year might not be this year. Second, consider high-deductible health plans (HDHPs) paired with health savings accounts (HSAs), which can lower premiums while offering tax advantages. For example, in 2023, the maximum HSA contribution for individuals is $3,850, providing a substantial cushion for out-of-pocket expenses. However, this strategy works best for those with relatively low healthcare needs, as high deductibles can be financially burdensome if major medical issues arise.

A comparative analysis of state-level policies reveals how regulatory environments influence premium trends. States with robust marketplaces and strong competition among insurers, such as California, have seen more moderate rate increases compared to states with fewer options. For instance, California’s active oversight and negotiation with insurers have kept average premium hikes below the national average in recent years. Conversely, states with less regulatory intervention, like Texas, often experience sharper increases due to limited competition and higher administrative costs. This highlights the importance of state-level policy decisions in shaping the affordability of health insurance.

Finally, it’s essential to recognize that policy changes and rate hikes are not isolated phenomena but part of a broader healthcare ecosystem. As medical costs continue to rise—driven by factors like drug price inflation and advanced technology—insurers face pressure to maintain profitability. Policymakers must balance the need for comprehensive coverage with the imperative to keep insurance affordable. For consumers, staying informed about legislative developments and understanding how they translate to premium changes is key to navigating this complex landscape. While rate hikes may feel inevitable, a combination of policy awareness and strategic plan selection can help mitigate their financial impact.

LensCrafters Insurance: What Medical Plans Are Accepted?

You may want to see also

Explore related products

![]()

Rising Healthcare Costs Influence

Healthcare costs have surged dramatically over the past decade, outpacing inflation and wage growth. This trend directly impacts health insurance premiums, as insurers adjust rates to cover escalating expenses. For instance, between 2010 and 2020, average annual premiums for employer-sponsored family coverage rose from $13,770 to $21,342, according to the Kaiser Family Foundation. Such increases strain household budgets, forcing individuals to choose between comprehensive coverage and affordability. Understanding the drivers behind rising healthcare costs is crucial for navigating this complex landscape.

One major factor influencing healthcare costs is the advancement of medical technology. While innovations like targeted therapies and robotic surgeries improve outcomes, they come with hefty price tags. For example, a single dose of a gene therapy treatment can cost upwards of $2 million. Insurers must account for these expenses, often passing them on to policyholders. Additionally, the aging population increases demand for chronic care, further driving up costs. As medical technology continues to evolve, balancing access to cutting-edge treatments with cost containment remains a critical challenge.

Pharmaceutical pricing also plays a significant role in rising healthcare costs. Prescription drug prices in the U.S. are among the highest globally, with some specialty medications costing thousands of dollars per month. Insurers often negotiate discounts, but these savings are not always passed on to consumers. For instance, a 2021 study found that list prices for insulin nearly doubled over the past decade, despite minimal changes in production costs. Policymakers and insurers must address pricing transparency and competition to mitigate this burden.

Another often-overlooked influence is administrative inefficiency within the healthcare system. The U.S. spends significantly more on administrative costs than other developed nations, with estimates ranging from 8% to 25% of total healthcare expenditures. Streamlining billing processes, reducing redundant paperwork, and adopting standardized electronic health records could yield substantial savings. For example, countries like Canada and the UK achieve lower administrative costs through centralized systems, offering a model for potential reforms.

Practical steps can help individuals mitigate the impact of rising healthcare costs. First, compare insurance plans annually during open enrollment, focusing on premiums, deductibles, and out-of-pocket maximums. High-deductible plans paired with health savings accounts (HSAs) can be cost-effective for those with minimal healthcare needs. Second, utilize preventive care services, such as annual check-ups and screenings, to avoid costly treatments later. Finally, explore generic medications and patient assistance programs to reduce prescription expenses. By staying informed and proactive, individuals can navigate the challenges posed by rising healthcare costs more effectively.

Get Medical Insurance in Oklahoma: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Market Competition and Pricing Trends

Health insurance premiums have been on a steady upward trajectory, but the reasons behind this trend are multifaceted and deeply intertwined with market competition. A key driver is the consolidation within the healthcare industry, where larger insurers and provider networks dominate the landscape. This consolidation reduces competition, giving these entities greater leverage to set higher prices. For instance, in regions where one or two insurers control a significant market share, premiums tend to be higher due to the lack of competitive pressure to keep prices in check. This dynamic underscores the inverse relationship between market concentration and consumer affordability.

To illustrate, consider the impact of mergers and acquisitions in the health insurance sector. When insurers merge, they often justify the move by promising cost efficiencies, but these savings rarely translate into lower premiums for consumers. Instead, the reduced competition allows the newly formed entity to raise prices without fear of losing customers to competitors. A 2021 study by the American Medical Association found that hospital consolidation led to higher prices for services, which insurers then pass on to policyholders in the form of increased premiums. This ripple effect highlights how market competition—or the lack thereof—directly influences pricing trends.

However, it’s not all bleak. In markets with robust competition, insurers are compelled to innovate and offer more affordable plans to attract customers. For example, in states with active health insurance marketplaces, such as California and New York, the presence of multiple insurers has led to more competitive pricing and a wider range of plan options. Consumers in these areas often benefit from lower premiums and better coverage, demonstrating that competition can act as a counterbalance to rising costs. Policymakers can take note: fostering a competitive environment through regulation and market oversight is essential to mitigating premium increases.

Another critical factor is the role of provider reimbursement rates. Insurers negotiate contracts with hospitals and physicians, and these rates directly impact the cost of coverage. In highly competitive markets, insurers have more negotiating power to secure lower reimbursement rates, which can help keep premiums stable. Conversely, in less competitive markets, providers can demand higher rates, forcing insurers to raise premiums to cover the increased costs. This interplay between insurers and providers reveals how competition at multiple levels of the healthcare ecosystem affects pricing trends.

Practical steps can be taken to address these issues. Consumers should actively compare plans during open enrollment periods, leveraging tools like healthcare.gov to identify the most cost-effective options. Employers, too, can play a role by offering a variety of insurance plans to employees, encouraging competition among insurers. Policymakers must prioritize antitrust enforcement to prevent further consolidation and promote market entry for new insurers. By understanding the link between market competition and pricing trends, stakeholders can work together to create a more affordable health insurance landscape.

Fender Warehouse Scottsdale: Medical Insurance Provision?

You may want to see also

Explore related products

![]()

Government Regulations and Premium Adjustments

Government regulations play a pivotal role in shaping health insurance premiums, often acting as a double-edged sword. On one hand, policies like the Affordable Care Act (ACA) mandate essential health benefits, ensuring coverage for pre-existing conditions and preventive services. This broadens access but can increase costs for insurers, who then pass these expenses onto consumers. For instance, the ACA’s elimination of lifetime coverage limits and the inclusion of maternity care have contributed to premium hikes, particularly for younger, healthier individuals who may not utilize these benefits extensively. On the other hand, regulations like the Medical Loss Ratio (MLR) rule, which requires insurers to spend at least 80% of premiums on healthcare claims, aim to curb administrative waste and profiteering. However, compliance with such rules often necessitates higher premiums to maintain profitability, illustrating the delicate balance between consumer protection and cost control.

Consider the impact of state-specific regulations, which can exacerbate or mitigate premium increases. States with robust insurance mandates, such as requiring coverage for fertility treatments or acupuncture, tend to see higher premiums due to the expanded scope of benefits. For example, New York’s extensive mandates contribute to its residents paying some of the highest premiums in the nation. Conversely, states with fewer mandates, like Idaho or Wyoming, often have lower premiums but may offer less comprehensive coverage. This variation underscores the importance of understanding local regulations when evaluating premium trends. Policyholders in highly regulated states should scrutinize their plans to ensure they’re not paying for unnecessary benefits, while those in less regulated areas might consider supplemental policies to fill coverage gaps.

A critical yet overlooked aspect of government regulations is their role in stabilizing premiums through risk-sharing mechanisms. Programs like the ACA’s risk adjustment program redistribute funds from insurers with healthier enrollees to those with sicker populations, fostering market stability. However, this can inadvertently incentivize insurers to attract low-risk individuals, potentially leading to adverse selection and higher premiums for those with greater health needs. For consumers, this means that while regulations aim to prevent price gouging, they can also create unintended consequences. To navigate this, individuals should compare plans during open enrollment, focusing on both premiums and out-of-pocket costs, and consider switching insurers if their current plan no longer aligns with their health needs or budget.

Finally, the interplay between government regulations and premium adjustments highlights the need for proactive consumer engagement. For instance, the recent Inflation Reduction Act (IRA) caps insulin copays at $35 for Medicare beneficiaries, a regulation that directly reduces out-of-pocket costs but may indirectly influence premiums for other covered services. Similarly, the IRA’s extension of ACA subsidies through 2025 provides immediate relief for marketplace enrollees but could lead to premium increases once these subsidies expire. To mitigate such impacts, individuals should stay informed about legislative changes, utilize premium tax credits if eligible, and explore health savings accounts (HSAs) to offset rising costs. By understanding how regulations shape premiums, consumers can make more informed decisions and advocate for policies that balance affordability with comprehensive coverage.

Contract and Insurance Applications: A Step-by-Step Guide

You may want to see also

Frequently asked questions

Yes, health insurance premiums increased in 2023 for many plans due to factors like rising healthcare costs, inflation, and increased demand for medical services.

Health insurance rates often rise due to higher medical costs, prescription drug prices, inflation, and changes in healthcare utilization patterns.

No, increases vary by location, plan type, insurer, and individual factors like age, coverage level, and health status.

While you can’t completely avoid increases, you can shop around for plans, consider higher deductibles, or explore subsidies through the Affordable Care Act (ACA) marketplace.

The ACA has both stabilized and increased premiums for some, depending on factors like subsidies, pre-existing conditions coverage, and market regulations.