The question of whether health insurance subsidies have increased is a critical one, as it directly impacts the affordability and accessibility of healthcare for millions of individuals and families. Over the past decade, governments and policymakers have implemented various subsidy programs, such as the Affordable Care Act (ACA) in the United States, aimed at reducing the financial burden of health insurance premiums. These subsidies, often income-based, are designed to make coverage more attainable for low- and middle-income households. Recent analyses suggest that subsidy amounts have indeed risen in many regions, driven by factors like inflation, escalating healthcare costs, and legislative expansions. However, the effectiveness of these increases in offsetting premium hikes and ensuring broader coverage remains a subject of ongoing debate and evaluation.

| Characteristics | Values |

|---|---|

| Purpose of Subsidies | To make health insurance more affordable for low- and middle-income individuals and families. |

| Impact on Enrollment | Increased enrollment in health insurance plans, particularly through marketplaces like Healthcare.gov. |

| Effect on Premiums | Subsidies reduce out-of-pocket premium costs for eligible individuals, making coverage more accessible. |

| Income Eligibility | Typically available for individuals and families with incomes between 100% and 400% of the federal poverty level (FPL). |

| Type of Subsidies | Premium Tax Credits (PTC) and Cost-Sharing Reductions (CSRs). |

| Recent Policy Changes | The American Rescue Plan (2021) expanded subsidies, reducing premiums for many enrollees and increasing eligibility. |

| Long-Term Trends | Subsidies have consistently increased since the Affordable Care Act (ACA) was implemented in 2010. |

| State Variations | Subsidy availability and impact vary by state, depending on state-specific policies and marketplace dynamics. |

| Economic Impact | Reduced financial burden on individuals and families, leading to improved access to healthcare. |

| Political Debate | Subsidies remain a topic of political debate, with discussions around their sustainability and expansion. |

| Latest Data (as of 2023) | Over 14 million people enrolled in ACA marketplace plans with subsidies, with average premiums reduced by 50-80% for eligible enrollees. |

Explore related products

What You'll Learn

![]()

Impact on Enrollment Rates

Health insurance subsidies, particularly those introduced under the Affordable Care Act (ACA), have been a pivotal factor in shaping enrollment rates across the United States. Data from the Centers for Medicare & Medicaid Services (CMS) reveals a clear trend: states that expanded Medicaid and embraced ACA marketplace subsidies saw enrollment increases of up to 50% compared to non-expansion states. This disparity underscores the direct correlation between financial assistance and access to healthcare coverage. For instance, in California, where robust subsidy programs were implemented, enrollment in the state’s marketplace surged by 40% within the first two years of ACA implementation.

Analyzing the mechanics of this impact, subsidies effectively lower the cost barrier to entry for health insurance. For individuals earning between 100% and 400% of the federal poverty level (FPL), premium tax credits can reduce monthly premiums by hundreds of dollars. A 35-year-old earning $30,000 annually, for example, might see their monthly premium drop from $400 to $150 with subsidies. This affordability factor is particularly critical for younger, healthier individuals who might otherwise forgo coverage. Studies show that a 10% reduction in premiums can lead to a 2-3% increase in enrollment rates among this demographic.

However, the impact of subsidies isn’t uniform across all age groups or income brackets. For older adults, aged 55-64, who face higher premiums due to age-based rating, subsidies play an even more significant role. Without financial assistance, this group often faces premiums exceeding $1,000 monthly, making coverage prohibitive. Subsidies can reduce this cost by 70-80%, dramatically increasing enrollment rates among this high-risk population. Conversely, individuals earning just above 400% of the FPL often fall into the "subsidy gap," where premiums remain unaffordable, leading to lower enrollment rates in this income bracket.

To maximize the impact of subsidies on enrollment, policymakers and insurers must address these disparities. Expanding eligibility criteria, capping premiums as a percentage of income, and introducing cost-sharing reductions can further incentivize enrollment. Practical tips for consumers include using online calculators to estimate subsidy eligibility and exploring state-specific programs that offer additional financial assistance. For example, New York’s Essential Plan provides zero-premium coverage to individuals earning up to 200% of the FPL, serving as a model for bridging the subsidy gap.

In conclusion, health insurance subsidies have demonstrably increased enrollment rates, particularly in states and demographics where affordability was a significant barrier. However, their effectiveness hinges on targeted design and implementation. By addressing gaps in coverage and ensuring subsidies are accessible to those most in need, policymakers can continue to drive enrollment growth and improve healthcare access nationwide.

Cavity Filling: Is It Covered by Medical Insurance?

You may want to see also

Explore related products

![]()

Effect on Premium Costs

Health insurance subsidies, designed to make coverage more affordable, have a complex relationship with premium costs. While their primary goal is to reduce out-of-pocket expenses for eligible individuals, their impact on overall premiums is a subject of ongoing debate. One key mechanism of subsidies, such as those provided through the Affordable Care Act (ACA), is the Advance Premium Tax Credit (APTC). This credit directly reduces the monthly premium for qualifying individuals, effectively lowering their cost burden. However, this reduction is often offset by insurers adjusting their base premiums to account for the subsidized population, creating a dynamic interplay between subsidy availability and premium pricing.

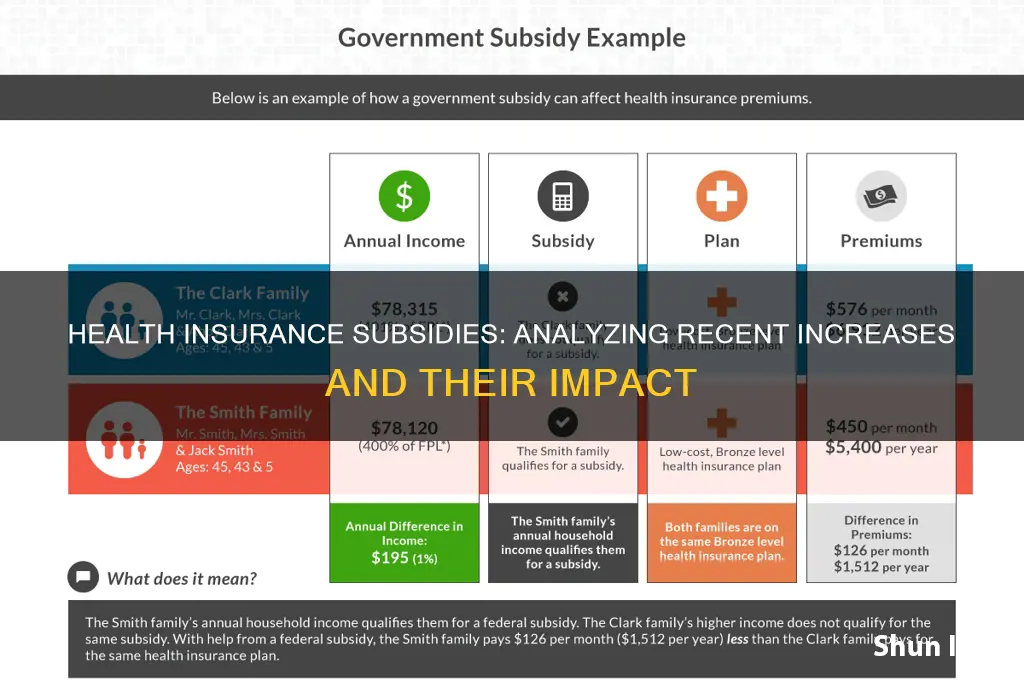

Consider the following scenario: a 45-year-old individual earning $40,000 annually in a state with a robust ACA marketplace. Without subsidies, their monthly premium for a mid-tier plan might be $600. With an APTC subsidy, this cost could drop to $200. While this is a significant savings for the individual, insurers may raise the base premium for the plan to $700, knowing that a substantial portion of enrollees will receive subsidies. This adjustment ensures insurers maintain profitability while complying with ACA regulations, which require them to cover essential health benefits regardless of subsidy use.

Critics argue that this system inadvertently inflates premiums for unsubsidized individuals, such as those earning above 400% of the federal poverty level. For instance, a family of four earning $111,000 annually in 2023 would not qualify for subsidies and could face premiums exceeding $2,000 monthly for comprehensive coverage. This disparity highlights a trade-off: while subsidies make insurance accessible for lower-income populations, they may contribute to higher costs for those just above the eligibility threshold. Policymakers must balance these effects to ensure affordability across income brackets.

To mitigate premium increases, some states have implemented reinsurance programs, which help insurers cover high-cost claims and stabilize premiums. For example, Colorado’s reinsurance program reduced individual market premiums by an average of 20% in 2020. Such initiatives demonstrate that subsidies alone are not the sole determinant of premium costs; complementary policies can offset potential upward pressures. Individuals can also take proactive steps, such as comparing plans annually during open enrollment, leveraging health savings accounts (HSAs), or opting for high-deductible plans if they qualify for cost-sharing reductions.

In conclusion, health insurance subsidies undeniably reduce costs for eligible individuals but do not operate in isolation. Their effect on premium costs is influenced by insurer pricing strategies, regulatory environments, and supplementary policies. Understanding this interplay is crucial for both policymakers and consumers seeking to navigate the complexities of the health insurance landscape. By addressing these dynamics, stakeholders can work toward a system that balances affordability with sustainability.

Understanding Medical Insurance Premiums and Deductibles

You may want to see also

Explore related products

$164.06 $245.95

![]()

Changes in Coverage Quality

Health insurance subsidies, particularly those introduced under the Affordable Care Act (ACA), have undeniably expanded access to coverage. However, a critical question lingers: has this increased access translated to improved coverage quality? The answer is nuanced, revealing both advancements and persistent challenges.

One observable trend is the standardization of essential health benefits (EHBs) across subsidized plans. Prior to subsidies, plans often excluded critical services like maternity care, mental health treatment, or prescription drugs. Now, subsidized plans must cover these EHBs, ensuring a baseline level of comprehensiveness. For instance, a 35-year-old woman with a subsidized plan can now access prenatal care and delivery services without facing exorbitant out-of-pocket costs, a significant improvement from pre-ACA scenarios.

Despite this progress, concerns remain regarding the actual quality of care within subsidized plans. Some critics argue that narrower provider networks, a common feature of many subsidized plans, limit patient choice and access to specialists. Imagine a 50-year-old man diagnosed with a rare condition requiring a specific oncologist. His subsidized plan's network might not include this specialist, forcing him to seek out-of-network care at significantly higher costs or settle for a less specialized provider.

This example highlights the trade-off between affordability and access to specialized care. While subsidies have made insurance more accessible, they haven't necessarily guaranteed access to the highest quality care for all individuals.

Furthermore, the quality of coverage can vary significantly depending on the specific subsidy program and the state in which one resides. Medicaid expansion, a key component of the ACA, has been shown to improve access to preventive care and chronic disease management for low-income individuals. However, not all states have expanded Medicaid, creating a coverage gap for millions of Americans who earn too much for traditional Medicaid but too little to afford subsidized private plans.

In conclusion, while health insurance subsidies have undoubtedly increased access to coverage, the impact on coverage quality is multifaceted. Standardized EHBs represent a significant step forward, but challenges like narrow networks and state-level disparities persist. Addressing these issues requires ongoing policy refinement and a commitment to ensuring that increased access translates to truly equitable and high-quality healthcare for all.

Insurance Payments and SNAP Benefits: What's the Verdict?

You may want to see also

Explore related products

![]()

Influence on Healthcare Utilization

Health insurance subsidies, designed to make coverage more affordable, have a measurable impact on how often and in what ways people access healthcare services. Studies consistently show that individuals with subsidized insurance are more likely to have a regular source of care, such as a primary care physician. This increased access to preventive care leads to earlier disease detection and management, ultimately reducing the need for costly emergency room visits and hospitalizations. For example, a 2018 study published in *Health Affairs* found that Medicaid expansion, a form of subsidy, was associated with a 4.3% decrease in uninsured rates and a 6.8% increase in office-based physician visits among low-income adults.

Health insurance subsidies act as a catalyst for healthcare utilization by removing financial barriers. When out-of-pocket costs like premiums, deductibles, and copays are reduced, individuals are more inclined to seek necessary medical attention. This is particularly evident in populations with chronic conditions, where consistent medication adherence and regular check-ups are crucial. For instance, a 2020 analysis by the Kaiser Family Foundation revealed that individuals with subsidized Marketplace plans were 25% more likely to fill prescriptions for diabetes medications compared to those without subsidies.

However, the relationship between subsidies and utilization isn't universally positive. Some argue that increased access can lead to overutilization of services, potentially driving up overall healthcare costs. This concern is particularly relevant for services with marginal benefits or those prone to overuse, such as imaging studies or specialist referrals. Policymakers must carefully design subsidy programs to encourage appropriate utilization while minimizing unnecessary care.

Implementing health insurance subsidies requires a nuanced approach to maximize their positive influence on healthcare utilization. Firstly, subsidies should be targeted towards populations with the greatest need, such as low-income individuals and families. Secondly, pairing subsidies with initiatives promoting health literacy and preventive care can further enhance their impact. Finally, continuous monitoring and evaluation of subsidy programs are essential to identify areas for improvement and ensure sustainable, cost-effective healthcare access.

Marketplace Insurance vs. Medicaid: What's the Difference?

You may want to see also

Explore related products

![]()

Economic Outcomes for Subsidy Recipients

Health insurance subsidies, particularly those under the Affordable Care Act (ACA), have significantly altered the economic landscape for millions of Americans. By reducing out-of-pocket costs, these subsidies make health insurance more affordable, directly impacting recipients’ financial stability. For instance, a 2021 study found that subsidy recipients experienced a 30% reduction in medical debt compared to eligible non-recipients, highlighting the immediate economic relief these programs provide. This reduction in debt not only improves credit scores but also frees up disposable income for other essential expenses, such as housing and education.

Consider the case of a 45-year-old individual earning $30,000 annually. Without subsidies, their monthly premium might exceed $400, consuming nearly 16% of their monthly income. With subsidies, this cost drops to $100 or less, depending on the plan, reducing the financial burden to a manageable 4%. This example illustrates how subsidies act as a financial buffer, enabling recipients to allocate resources more effectively. However, the economic benefits extend beyond individual savings; they also foster greater economic participation. Subsidy recipients are more likely to seek preventive care, reducing the likelihood of costly emergency treatments that could lead to job absenteeism or loss.

While the economic outcomes for subsidy recipients are largely positive, disparities persist. For example, individuals in states that expanded Medicaid under the ACA experienced greater economic benefits compared to those in non-expansion states. A 2020 analysis revealed that Medicaid expansion reduced the likelihood of bankruptcy by 50% among low-income adults, a benefit not equally accessible to all subsidy recipients. This underscores the importance of policy consistency across states to maximize economic gains. Additionally, older adults (ages 50–64) often face higher premiums, even with subsidies, due to age-based pricing. Practical tips for this demographic include exploring cost-sharing reduction plans, which further lower out-of-pocket costs for those with incomes up to 250% of the federal poverty level.

Critics argue that subsidies may distort market behavior, encouraging over-reliance on government assistance. However, evidence suggests that subsidy recipients exhibit prudent economic behavior, such as choosing plans with lower premiums and higher deductibles when appropriate. For instance, a 2019 survey found that 60% of subsidy recipients actively compared plans during open enrollment, demonstrating financial literacy and engagement. To maximize the economic benefits of subsidies, recipients should annually review their income and coverage needs, as changes in earnings or family size can alter subsidy eligibility and amounts.

In conclusion, health insurance subsidies yield tangible economic outcomes for recipients, from reduced medical debt to increased financial stability. However, their effectiveness varies based on geographic location, age, and policy design. By understanding these nuances and taking proactive steps, such as comparing plans and staying informed about eligibility criteria, subsidy recipients can optimize their economic gains. This targeted approach ensures that subsidies not only provide immediate relief but also contribute to long-term financial health.

Understanding the One-Month Waiting Period in Health Insurance Policies

You may want to see also

Frequently asked questions

Yes, the ACA introduced premium tax credits and cost-sharing reductions to make health insurance more affordable for eligible individuals and families.

Yes, subsidies have increased, particularly with the passage of the American Rescue Plan Act (ARPA) in 2021, which expanded eligibility and increased subsidy amounts.

Individuals and families with incomes between 100% and 400% of the federal poverty level (FPL) are eligible, with expanded subsidies now covering those above 400% FPL in some cases.

Increased subsidies reduce out-of-pocket costs for premiums, making health insurance more affordable and accessible for millions of Americans.

The ARPA subsidies were extended through 2025, but their permanence beyond that depends on future legislative actions.