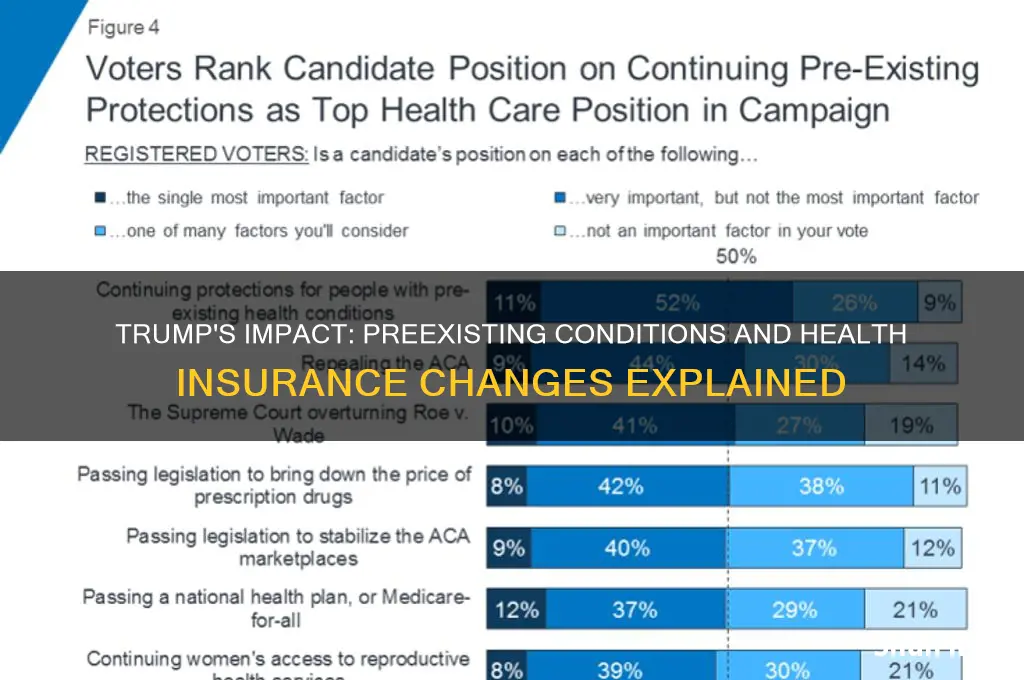

The question of whether former President Donald Trump eliminated protections for preexisting conditions in health insurance has been a contentious issue. While Trump did not outright do away with these protections, his administration took several actions that critics argued weakened the Affordable Care Act (ACA), particularly its safeguards for individuals with preexisting conditions. Trump supported legislative efforts to repeal the ACA, such as the American Health Care Act in 2017, which would have allowed states to waive essential health benefits and potentially undermine protections for preexisting conditions. Additionally, his administration expanded the use of short-term health plans and association health plans, which often excluded coverage for preexisting conditions. Although the ACA’s protections remained in place due to legal challenges and congressional gridlock, Trump’s policies and rhetoric raised significant concerns about the future of healthcare access for millions of Americans with preexisting conditions.

| Characteristics | Values |

|---|---|

| Trump's Actions on Preexisting Conditions | Did not eliminate protections for preexisting conditions under the ACA. |

| ACA (Obamacare) Protections | Prohibits insurers from denying coverage or charging more based on health. |

| Trump's Attempts to Repeal ACA | Supported legislative efforts to repeal ACA, which would have removed protections. |

| Legal Challenges | Backed a lawsuit (Texas v. Azar) to declare ACA unconstitutional, threatening protections. |

| Current Status of Protections | Protections remain in place as of 2023, upheld by courts and Congress. |

| Public Stance | Claimed support for preexisting condition protections but actions contradicted this. |

| Impact on Insurance Market | No changes to preexisting condition rules under Trump’s presidency. |

| Biden Administration’s Position | Strengthened ACA protections and expanded access to healthcare. |

Explore related products

What You'll Learn

![]()

ACA Protections Retained

Despite efforts to repeal the Affordable Care Act (ACA), protections for individuals with preexisting conditions remain intact. This is a critical point for the millions of Americans who rely on these safeguards to access affordable healthcare. The ACA’s prohibition on denying coverage or charging higher premiums based on health status has been a cornerstone of its legacy, ensuring that conditions like diabetes, cancer, or asthma do not disqualify anyone from insurance. While legislative and legal challenges have sought to dismantle the ACA, key provisions protecting preexisting conditions have endured, largely due to their widespread public support and embedded legal framework.

Analyzing the Trump administration’s actions reveals a pattern of attempting to weaken the ACA without fully eliminating preexisting condition protections. For instance, the administration supported lawsuits like *Texas v. United States*, which aimed to strike down the entire ACA, including its preexisting condition safeguards. However, these efforts were largely unsuccessful, as courts upheld the ACA’s constitutionality. Additionally, while Trump promoted short-term health plans and association health plans as alternatives, these options were not required to comply with ACA protections, creating a parallel, less regulated market. Yet, the core ACA marketplace plans, covering over 20 million Americans, retained their robust protections.

For consumers, understanding the retention of ACA protections is essential for navigating health insurance choices. If you have a preexisting condition, enrolling in a marketplace plan during open enrollment (typically November 1 to January 15) ensures access to comprehensive coverage without discrimination. Be cautious of non-ACA-compliant plans, which may exclude preexisting conditions or impose waiting periods. Practical tips include reviewing plan summaries for ACA compliance, checking if your preferred doctors are in-network, and utilizing premium tax credits if eligible. For example, a 45-year-old with hypertension could save up to 70% on monthly premiums through subsidies, depending on income.

Comparatively, the retention of ACA protections stands in stark contrast to pre-2010 health insurance practices, where individuals with preexisting conditions often faced denials or exorbitant rates. The ACA’s guaranteed issue and community rating provisions have fundamentally reshaped the insurance landscape, ensuring fairness and accessibility. While political debates continue, the practical reality is that these protections remain a vital safety net. For instance, a study by the Kaiser Family Foundation found that 54 million non-elderly adults have preexisting conditions, highlighting the broad impact of retaining these safeguards.

In conclusion, the ACA’s preexisting condition protections have withstood significant challenges, remaining a cornerstone of American healthcare policy. By focusing on marketplace plans and understanding the limitations of alternative options, individuals can secure coverage that meets their needs. As debates over healthcare reform persist, the retention of these protections serves as a reminder of their enduring importance in ensuring equitable access to care.

Did the ACA Cause Millions to Lose Health Insurance?

You may want to see also

Explore related products

![]()

Trump's Repeal Efforts

During his presidency, Donald Trump made repeated attempts to dismantle the Affordable Care Act (ACA), often referred to as Obamacare, which included protections for individuals with preexisting conditions. These efforts were primarily channeled through legislative proposals, executive actions, and legal challenges. While Trump frequently claimed he would protect coverage for preexisting conditions, his actions often contradicted this promise, leaving millions of Americans uncertain about their healthcare security.

One of Trump’s most significant repeal efforts was his support for the American Health Care Act (AHCA) in 2017. This bill, backed by House Republicans, would have allowed states to waive essential health benefits and community rating requirements, effectively undermining protections for preexisting conditions. Under the AHCA, insurers could charge higher premiums based on health status, making coverage unaffordable for those with chronic illnesses. Despite Trump’s assurances, the Congressional Budget Office estimated that 23 million people would lose insurance over a decade if the bill passed. Public outcry and opposition from both parties ultimately led to its failure, but it highlighted Trump’s willingness to compromise preexisting condition protections.

Another critical move was Trump’s decision to eliminate the individual mandate penalty in the 2017 Tax Cuts and Jobs Act. This penalty, a cornerstone of the ACA, encouraged healthy individuals to enroll in insurance, stabilizing the risk pool and keeping premiums lower for everyone, including those with preexisting conditions. Without it, healthier individuals were more likely to opt out, potentially leading to higher costs and fewer options for those with chronic health issues. While this change didn’t directly eliminate preexisting condition protections, it weakened the ACA’s framework, making it harder to sustain these safeguards.

Trump’s administration also pursued legal action to strike down the entire ACA, including its preexisting condition protections. In *California v. Texas*, the Department of Justice argued that the ACA was unconstitutional after the individual mandate penalty was zeroed out. If successful, this lawsuit would have invalidated the entire law, leaving 54 million Americans with preexisting conditions vulnerable to discrimination by insurers. Although the Supreme Court ultimately upheld the ACA in 2021, the case underscored Trump’s persistent efforts to dismantle the law, regardless of the consequences for those with preexisting conditions.

In contrast to his repeal efforts, Trump occasionally proposed alternative plans to address preexisting conditions, but these lacked substance and feasibility. For instance, he signed an executive order in 2020 declaring that individuals with preexisting conditions would be protected, but this order had no legal or regulatory force. Without legislative action or enforcement mechanisms, such declarations were largely symbolic and did little to reassure those at risk of losing coverage. Trump’s inability to offer a concrete alternative further eroded trust in his commitment to protecting preexisting conditions.

In summary, Trump’s repeal efforts were marked by legislative proposals, executive actions, and legal challenges that consistently threatened preexisting condition protections. While he often claimed to support these safeguards, his policies and actions undermined the ACA’s framework, leaving millions of Americans at risk. Understanding these efforts is crucial for evaluating the impact of his presidency on healthcare and the ongoing debate over preexisting condition protections.

Insurance Providers Accepted by Fairview: A Comprehensive Guide for Patients

You may want to see also

Explore related products

![]()

Pre-existing Conditions Defined

A pre-existing condition is any health issue that exists before the effective date of a new health insurance policy. This definition, though seemingly straightforward, carries significant weight in the healthcare debate, particularly in discussions surrounding the Affordable Care Act (ACA) and its subsequent modifications. Understanding what constitutes a pre-existing condition is crucial for anyone navigating the complexities of health insurance, especially those with ongoing medical needs.

Examples range from chronic illnesses like diabetes and asthma to past injuries or even pregnancy.

The ACA, often referred to as Obamacare, mandated that insurance companies cannot deny coverage or charge higher premiums based on pre-existing conditions. This provision was a game-changer for millions of Americans, ensuring access to healthcare regardless of their medical history. However, the question of whether the Trump administration "did away" with these protections requires a nuanced look at the actions taken during his tenure.

One key area of focus is the Trump administration’s efforts to dismantle parts of the ACA, particularly through legislative and judicial challenges. For instance, the administration supported a lawsuit (Texas v. United States) that sought to declare the entire ACA unconstitutional. Had this succeeded, protections for pre-existing conditions would have been eliminated. While the Supreme Court ultimately upheld the ACA in 2021, the uncertainty during this period highlighted the fragility of these safeguards.

Another critical aspect is the expansion of short-term health plans under Trump’s leadership. These plans, originally intended for temporary coverage gaps, were extended to last up to three years. Unlike ACA-compliant plans, short-term plans are not required to cover pre-existing conditions, often excluding them entirely or charging exorbitant rates. This move effectively created a parallel insurance market that undermined the ACA’s protections, leaving some individuals with limited options for comprehensive coverage.

For those with pre-existing conditions, the takeaway is clear: vigilance is essential. While the core protections of the ACA remain intact, ongoing political and legislative battles mean these safeguards are not guaranteed indefinitely. Individuals should carefully review insurance policies, avoid short-term plans if comprehensive coverage is needed, and stay informed about policy changes that could impact their healthcare access. Understanding the definition and implications of pre-existing conditions is the first step in advocating for one’s health and financial security.

Pet Insurance Providers That Cover Pre-Existing Conditions: A Guide

You may want to see also

Explore related products

![]()

Legal Challenges Overview

The Trump administration's efforts to reshape the Affordable Care Act (ACA) sparked numerous legal battles, particularly around protections for individuals with preexisting conditions. One of the most significant challenges came in the form of the *Texas v. United States* lawsuit, filed in 2018. The plaintiffs, led by several Republican-led states, argued that the ACA’s individual mandate was unconstitutional after Congress reduced the penalty to $0 in the 2017 Tax Cuts and Jobs Act. They further claimed that the entire law, including its preexisting condition protections, should be struck down as a result. This case exemplifies how legal challenges sought to dismantle the ACA’s core provisions by targeting its structural integrity.

Analyzing the legal strategy reveals a deliberate attempt to exploit legislative changes for broader policy goals. By zeroing in on the individual mandate, opponents aimed to invalidate the entire ACA, including Section 1201, which prohibits insurers from denying coverage or charging higher premiums based on preexisting conditions. The Trump administration supported this effort, declining to defend the ACA in court and filing briefs arguing that the protections for preexisting conditions were inseverable from the mandate. This approach underscores the interconnectedness of the ACA’s provisions and the potential domino effect of legal challenges.

A critical turning point came in 2020 when the Supreme Court ruled on *California v. Texas*, the successor to *Texas v. United States*. In a 7-2 decision, the Court held that the plaintiffs lacked standing to challenge the ACA, effectively preserving the law, including its preexisting condition protections. However, the Court did not rule on the constitutionality of the individual mandate itself, leaving open the possibility of future challenges. This outcome highlights the importance of standing in constitutional litigation and the role of judicial restraint in high-stakes policy disputes.

Practical takeaways from these legal challenges emphasize the need for vigilance in protecting healthcare rights. Advocates and policymakers must monitor legislative and judicial developments to safeguard the ACA’s gains. For individuals, understanding the legal landscape can empower them to advocate for their rights and challenge discriminatory practices. For example, if an insurer denies coverage based on a preexisting condition, individuals can cite the ACA’s protections and file complaints with state insurance commissioners or the Department of Health and Human Services.

Comparatively, the Trump-era legal challenges differ from earlier ACA disputes, such as *King v. Burwell* (2015), which focused on the legality of federal subsidies. While *King v. Burwell* centered on implementation, the more recent cases aimed at the ACA’s foundational structure. This shift reflects a strategic pivot from technical challenges to existential threats, underscoring the ongoing vulnerability of healthcare reforms to political and legal attacks. As the ACA continues to evolve, these legal battles serve as a reminder of the fragility of policy achievements and the enduring need for robust defenses.

Soft Tissue Grafts: Are They Covered by Medical Insurance?

You may want to see also

Explore related products

![]()

Current Policy Status

The Affordable Care Act (ACA), often referred to as Obamacare, remains the cornerstone of protections for individuals with preexisting conditions. Despite numerous attempts to repeal or replace it, the ACA’s provisions ensuring coverage for preexisting conditions have endured, though their stability has been tested under the Trump administration. As of the current policy status, these protections are still in place, but their future hinges on ongoing legal battles and legislative actions.

One critical aspect of the current policy landscape is the Texas v. California lawsuit, which challenges the constitutionality of the ACA. The Trump administration supported this challenge, arguing that the individual mandate’s repeal in 2017 rendered the entire law invalid. If successful, this lawsuit could dismantle the ACA, including its preexisting condition protections. However, as of now, the Supreme Court has upheld the ACA, preserving these safeguards. This ruling underscores the resilience of the ACA’s framework, but it also highlights the ongoing vulnerability of these protections to legal and political challenges.

In practice, the ACA mandates that health insurance plans cannot deny coverage or charge higher premiums based on preexisting conditions. This applies to all plans sold on the Health Insurance Marketplace and many employer-sponsored plans. For example, a 45-year-old with diabetes cannot be denied coverage or charged more due to their condition. Additionally, insurers are required to cover essential health benefits, such as prescription drugs and maternity care, which are often critical for individuals with chronic conditions. These provisions remain intact, providing a safety net for millions of Americans.

However, the Trump administration did introduce changes that indirectly impacted preexisting condition protections. For instance, the expansion of short-term health plans and association health plans offered cheaper alternatives but often excluded coverage for preexisting conditions. These plans, while not replacing ACA-compliant insurance, created confusion and potentially left some individuals underinsured. It’s crucial for consumers to verify that their plan complies with ACA standards to ensure full protection.

Moving forward, the current policy status reflects a delicate balance between preserving protections and navigating political and legal challenges. Individuals should stay informed about legislative developments and review their health insurance options annually during open enrollment. For those with preexisting conditions, sticking with ACA-compliant plans remains the safest bet. While the ACA’s protections have withstood significant challenges, their long-term stability depends on continued advocacy and legal defense.

Insurance Hike: Accidents and Their Impact

You may want to see also

Frequently asked questions

No, Trump did not eliminate protections for pre-existing conditions. The Affordable Care Act (ACA), also known as Obamacare, established these protections, and they remain in place. However, Trump and his administration supported efforts to repeal or weaken the ACA, which could have indirectly threatened these protections.

Trump’s administration took actions that critics argued could undermine protections for pre-existing conditions, such as supporting the repeal of the ACA and expanding short-term health plans that don’t cover pre-existing conditions. However, the core ACA protections remained in place during his presidency.

Trump’s efforts to repeal the ACA, if successful, could have eliminated protections for pre-existing conditions. However, these attempts were blocked by Congress and the courts, so the ACA’s protections remained intact throughout his presidency.

Yes, pre-existing conditions are still covered under health insurance. The ACA’s protections for pre-existing conditions were not removed during Trump’s presidency and continue to be in effect, ensuring that insurers cannot deny coverage or charge higher premiums based on pre-existing health conditions.