The question of whether Donald Trump repealed the no health insurance fine is a significant one, as it relates to the Affordable Care Act (ACA), also known as Obamacare. The ACA originally included a provision known as the individual mandate, which required most Americans to have health insurance or pay a penalty, often referred to as the no health insurance fine. In 2017, as part of the Tax Cuts and Jobs Act, the Trump administration effectively eliminated this penalty by reducing it to $0 starting in 2019. This change meant that individuals who chose not to purchase health insurance would no longer face a federal tax penalty, marking a substantial shift in the enforcement of the ACA's individual mandate. While the mandate itself remains in the law, the removal of the fine has been a topic of debate regarding its impact on healthcare coverage and the stability of the insurance market.

| Characteristics | Values |

|---|---|

| Policy Change | Yes, Trump effectively repealed the individual mandate penalty (no health insurance fine) starting in 2019. |

| Legislation | Tax Cuts and Jobs Act of 2017 |

| Effective Date | January 1, 2019 |

| Penalty Reduction | Reduced the individual mandate penalty to $0. |

| Impact on ACA | Did not repeal the Affordable Care Act (ACA) itself, but eliminated the financial penalty for not having insurance. |

| Current Status | The individual mandate penalty remains at $0 as of the latest data (2023). |

| State-Level Penalties | Some states (e.g., California, New Jersey) have implemented their own penalties for not having health insurance. |

| Federal Penalty | No federal penalty for lacking health insurance since 2019. |

| Political Context | Part of Trump's efforts to dismantle key components of the ACA. |

| Public Reaction | Mixed reactions, with critics arguing it could lead to higher uninsured rates and supporters praising it as reducing government overreach. |

Explore related products

What You'll Learn

![]()

ACA Mandate Elimination

The Tax Cuts and Jobs Act of 2017, signed into law by President Trump, included a provision that effectively eliminated the Affordable Care Act's (ACA) individual mandate penalty. This change, which took effect in 2019, meant that individuals who chose not to purchase health insurance were no longer subject to a federal tax penalty. The elimination of this fine marked a significant shift in the enforcement of the ACA's individual mandate, which had been a cornerstone of the law's efforts to expand health insurance coverage.

Understanding the Impact

To grasp the implications of the ACA mandate elimination, consider the following scenario: a healthy 30-year-old individual, earning $40,000 annually, decides to opt-out of health insurance. Prior to 2019, this person would have faced a penalty of $695 or 2.5% of their income (whichever was higher). With the penalty eliminated, this individual can now allocate the money they would have spent on insurance premiums or penalties to other expenses, such as rent or student loans. However, it's essential to note that the absence of a penalty does not negate the potential financial risks associated with being uninsured, including high out-of-pocket costs for medical emergencies.

Analyzing the Consequences

A comparative analysis of states with and without their own individual mandates reveals interesting trends. States like California, New Jersey, and the District of Columbia, which implemented their own mandates and penalties, have seen more stable insurance markets and lower uninsured rates compared to states without such provisions. For instance, California's uninsured rate remained relatively constant at around 7% between 2018 and 2020, whereas states without mandates experienced more significant increases in uninsured rates. This data suggests that while the federal penalty elimination may not have directly caused widespread coverage losses, it did contribute to a more volatile insurance landscape, particularly in states without alternative measures in place.

Practical Considerations

For individuals navigating the post-mandate penalty landscape, it's crucial to weigh the risks and benefits of being uninsured. Those with pre-existing conditions or a higher likelihood of needing medical care should carefully consider the potential costs of forgoing insurance. On the other hand, healthy individuals with limited financial resources may opt for alternative arrangements, such as health sharing ministries or short-term health plans, which often provide more affordable coverage options. However, these alternatives typically offer less comprehensive benefits and may exclude coverage for pre-existing conditions or certain medical services.

Policy Implications and Future Directions

The elimination of the ACA mandate penalty has sparked ongoing debates about the most effective ways to encourage health insurance enrollment. Some policymakers advocate for reinstating a federal penalty, while others propose alternative incentives, such as tax credits or subsidies, to make coverage more affordable. As the healthcare landscape continues to evolve, it's essential for individuals to stay informed about policy changes and their potential impact on access to care. By understanding the nuances of the ACA mandate elimination, individuals can make more informed decisions about their health insurance options and better navigate the complexities of the healthcare system.

Medical Insurance Boundaries: Ethical and Legal Limits

You may want to see also

Explore related products

![]()

Tax Cuts and Jobs Act

The Tax Cuts and Jobs Act (TCJA) of 2017, a landmark piece of legislation under the Trump administration, significantly reshaped the U.S. tax code. Among its many provisions, one of the most debated changes was the reduction of the individual mandate penalty under the Affordable Care Act (ACA) to $0, effectively repealing the fine for not having health insurance starting in 2019. This move was framed as a tax cut, but its implications for healthcare policy were profound. By eliminating the financial penalty, the TCJA shifted the ACA’s enforcement mechanism, raising questions about its impact on insurance coverage rates and the broader healthcare market.

Analytically, the TCJA’s repeal of the health insurance fine was a strategic dismantling of a key ACA provision. The individual mandate was designed to encourage healthy individuals to purchase insurance, thereby stabilizing the risk pool and keeping premiums affordable. Without the penalty, economists predicted a decline in enrollment, particularly among younger, healthier individuals who might forgo coverage. This shift could lead to higher premiums for those remaining in the market, a phenomenon known as adverse selection. Critics argued that this change undermined the ACA’s goal of universal coverage, while supporters viewed it as a step toward reducing government overreach in personal healthcare decisions.

From a practical standpoint, the repeal of the fine had immediate and tangible effects on taxpayers. For the 2018 tax year, individuals were still required to pay the penalty if they lacked qualifying health coverage, but by 2019, this obligation disappeared. This change simplified tax filings for many, as they no longer needed to account for their insurance status on Form 8965. However, it also created confusion for those who assumed the ACA itself had been repealed, leading some to forgo coverage unnecessarily. Tax preparers and financial advisors had to educate clients on the distinction between the repealed penalty and the continued existence of the ACA’s other provisions.

Comparatively, the TCJA’s approach to healthcare differs sharply from previous policies. While the ACA used a carrot-and-stick approach—subsidies for purchasing insurance and penalties for non-compliance—the TCJA leaned entirely on the carrot, removing the stick. This shift reflects a broader ideological divide in U.S. healthcare policy: one side favoring mandates and penalties to ensure broad coverage, and the other emphasizing individual choice and market-driven solutions. The TCJA’s repeal of the fine aligns with the latter philosophy, prioritizing tax relief over enforcement of coverage requirements.

In conclusion, the Tax Cuts and Jobs Act’s repeal of the health insurance fine was a targeted policy change with far-reaching consequences. It exemplified the Trump administration’s approach to tax reform and healthcare, blending fiscal policy with ideological goals. While it provided immediate tax relief for some, it also introduced uncertainty into the healthcare market, highlighting the complex interplay between tax law and social policy. Understanding this provision requires a nuanced view of its intent, impact, and place within the broader healthcare debate.

Pregnancy Coverage: Top Health Insurance Providers for Expecting Parents

You may want to see also

Explore related products

$164.06 $245.95

![]()

Effective Date of Repeal

The Tax Cuts and Jobs Act of 2017, signed into law by President Trump, included a provision that effectively repealed the Affordable Care Act's individual mandate penalty, often referred to as the "no health insurance fine." This repeal did not take effect immediately, leaving many to wonder about the specific timing and implications. The effective date of this repeal was January 1, 2019, a detail crucial for understanding the transition period and its impact on taxpayers and healthcare policy.

Analyzing the timing reveals a deliberate legislative strategy. By setting the effective date for 2019, Congress allowed for a full year of tax compliance under the old rules in 2018, ensuring a smoother transition for both the IRS and taxpayers. This delay also provided individuals with one last opportunity to assess their healthcare coverage options before the penalty was eliminated. For instance, someone considering dropping their health insurance in 2018 would have faced a penalty, but the same decision in 2019 would incur no federal fine, though state-level penalties might still apply in certain regions.

From a practical standpoint, understanding the effective date is essential for financial planning. Taxpayers needed to be aware that the penalty still applied for the 2018 tax year, influencing decisions about health insurance coverage during that period. For example, a family of four earning $75,000 annually could have faced a penalty of approximately $2,085 in 2018 if uninsured, but this liability disappeared for 2019. This shift underscores the importance of staying informed about legislative changes and their timelines.

Comparatively, the repeal’s effective date contrasts with other healthcare policy changes, which often involve phased implementations or immediate effects. The delay in this case highlights a rare instance of legislative foresight, aiming to minimize confusion and administrative burden. However, it also created a temporary dichotomy: while the penalty was effectively repealed in law in 2017, its practical impact was deferred, requiring clear communication to avoid misunderstandings among the public.

In conclusion, the effective date of January 1, 2019, for the repeal of the no health insurance fine was a pivotal moment in healthcare policy, marking the end of a contentious aspect of the Affordable Care Act. Its delayed implementation served both administrative and taxpayer interests, offering a final year of compliance under the old rules while signaling a new era in health insurance regulation. For individuals and families, this date remains a critical reference point for understanding their obligations and options in the evolving landscape of healthcare coverage.

Medical Insurance: A Harmful Barrier to Patient Care?

You may want to see also

Explore related products

![]()

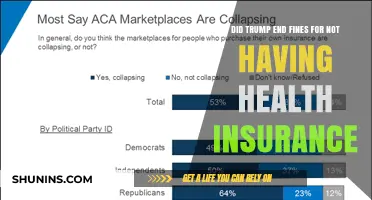

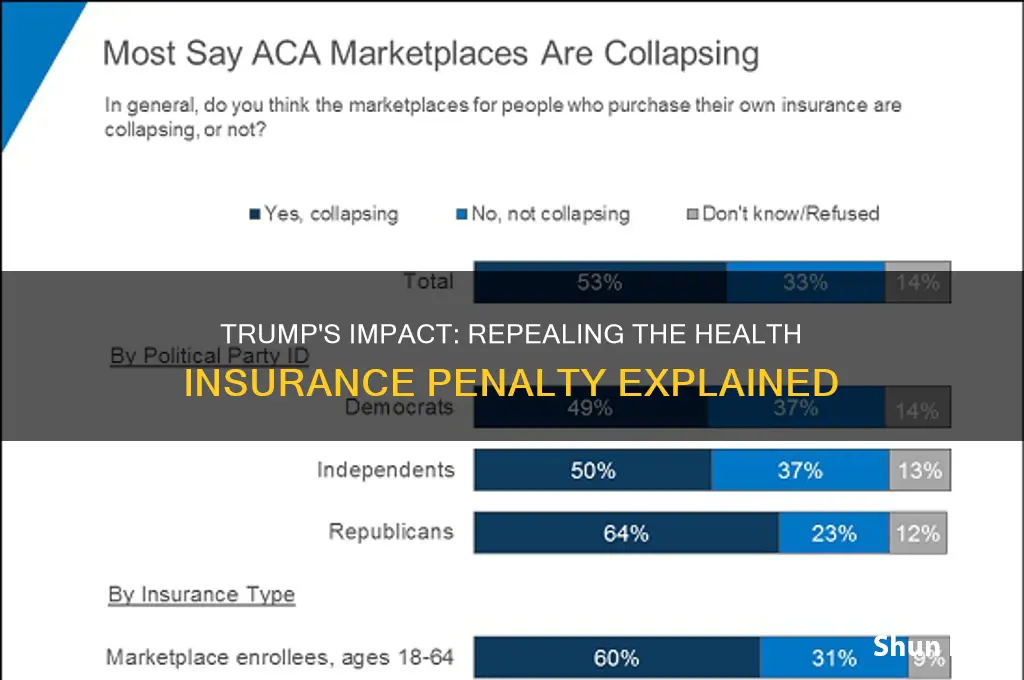

State-Level Penalties Impact

The Affordable Care Act's individual mandate, which required most Americans to have health insurance or pay a penalty, was effectively nullified when the Tax Cuts and Jobs Act of 2017 reduced the federal penalty to $0 starting in 2019. However, this federal change did not prevent states from implementing their own penalties for uninsured residents. As a result, the impact of state-level penalties has become a critical factor in shaping health insurance coverage rates and healthcare access across the country.

Analytical Perspective:

States like California, New Jersey, and Massachusetts have introduced their own mandates and penalties to counteract the federal rollback. For instance, California’s penalty for being uninsured in 2023 is $800 per adult and $400 per child, or 2.5% of household income, whichever is higher. Early data suggest these state-level penalties have helped maintain higher insurance rates compared to states without such measures. In California, the uninsured rate remained below 7% in 2022, while in Texas, which lacks a state mandate, it climbed to over 18%. This disparity highlights how state-level penalties can mitigate the effects of the federal repeal, but their success depends on enforcement mechanisms and public awareness campaigns.

Instructive Approach:

If you live in a state with a health insurance mandate, understanding the penalty structure is essential. For example, in New Jersey, the penalty for 2023 is calculated as either $713 per individual or 2.58% of household income, whichever is greater. To avoid this, ensure you enroll in a qualifying health plan during open enrollment periods. Some states, like Massachusetts, also offer exemptions for financial hardship or religious beliefs, so check your state’s guidelines. Pro tip: Use state-run marketplaces to compare plans and determine if you qualify for subsidies, which can offset costs and make compliance easier.

Comparative Analysis:

States without penalties have seen a sharper rise in uninsured rates, particularly among younger, healthier individuals who may perceive insurance as unnecessary. In Georgia, for instance, the uninsured rate increased by 2.5% between 2019 and 2022. Conversely, states with penalties have maintained more stable coverage levels. However, penalties alone are not a panacea. States like Vermont, which pairs its mandate with robust outreach programs, have achieved better results than those relying solely on fines. This suggests that penalties work best when combined with education and affordability initiatives.

Descriptive Insight:

The patchwork of state-level penalties has created a healthcare landscape where geography dictates access. In Washington State, the penalty is $800 per uninsured individual or 2.75% of income, but the state also invests heavily in Medicaid expansion and public health programs. This dual approach has kept uninsured rates low, even in rural areas. Meanwhile, in states like Florida, where there is no mandate and limited Medicaid expansion, residents face higher out-of-pocket costs and fewer coverage options. This contrast underscores the importance of state-level policies in shaping health equity and outcomes.

Persuasive Argument:

State-level penalties are not just about punishing the uninsured—they’re about protecting the broader healthcare system. When healthy individuals opt out of insurance, premiums rise for everyone else, creating a vicious cycle of higher costs and lower enrollment. States with mandates and penalties break this cycle by encouraging broader participation, which stabilizes insurance markets. Policymakers should view these measures as investments in public health, not burdens on citizens. For residents, compliance isn’t just a legal obligation—it’s a contribution to a healthier, more sustainable community.

T-Mobile's Phone Insurance Partner: Unveiling the Company Behind the Coverage

You may want to see also

Explore related products

![]()

Public Reaction and Debate

The repeal of the individual mandate penalty under the Trump administration sparked a wave of public reaction and debate, with opinions sharply divided along political, economic, and moral lines. Supporters of the repeal, largely from conservative circles, celebrated it as a victory for personal freedom and a reduction of government overreach. They argued that individuals should not be coerced into purchasing health insurance, especially if they felt they could not afford it or did not need it. This perspective resonated with younger, healthier demographics who viewed the mandate as an unnecessary financial burden. Conversely, critics, predominantly from liberal and progressive factions, warned that eliminating the penalty would destabilize the health insurance market, leading to higher premiums for those who remained insured and potentially leaving millions without coverage.

The debate extended beyond ideological camps, with practical implications for families and businesses. For instance, small business owners who previously struggled to provide health insurance for employees saw the repeal as a relief from regulatory pressure. However, healthcare providers and advocacy groups raised alarms about the long-term consequences, citing studies predicting increased uninsured rates and reduced access to preventive care. A 2017 Congressional Budget Office report estimated that 13 million more people would be uninsured by 2027 as a result of the repeal, a statistic that fueled heated discussions on social media and in town hall meetings. These conversations often highlighted the tension between individual liberty and collective responsibility in healthcare.

Public reaction also varied by age and health status, revealing deeper societal fault lines. Younger adults, who historically pay higher premiums to subsidize older and sicker individuals, were more likely to support the repeal, viewing it as a way to lower their costs. In contrast, older Americans and those with pre-existing conditions expressed fear that the repeal would make insurance unaffordable or inaccessible for them. This demographic divide was exacerbated by misinformation campaigns, with some claiming the repeal would lower overall healthcare costs, while others warned of a looming crisis. Fact-checking organizations played a crucial role in clarifying these claims, but the polarized nature of the debate often made it difficult for nuanced information to gain traction.

The repeal also became a focal point in state-level policy battles, as some states moved to reinstate their own individual mandates to counteract the federal change. States like New Jersey and California enacted penalties for residents without health insurance, citing the need to protect their markets and ensure coverage continuity. This patchwork approach further complicated public understanding, as residents in different states faced varying rules and consequences. For those navigating these changes, practical tips included checking state-specific regulations, exploring subsidized insurance options through the Affordable Care Act marketplace, and consulting financial advisors to weigh the risks of going uninsured.

Ultimately, the public reaction and debate surrounding the repeal of the no health insurance fine underscored the complexity of healthcare policy and its deep personal and political implications. While the repeal offered immediate relief for some, it raised broader questions about equity, affordability, and the role of government in ensuring access to care. As the dust settled, the conversation shifted toward long-term solutions, with advocates on both sides pushing for reforms that could balance individual freedoms with the need for a stable, inclusive healthcare system. For individuals, staying informed and proactive remained key, as the landscape continued to evolve in response to legislative and societal pressures.

Understanding Medical Insurance Carriers: What Does It Mean?

You may want to see also

Frequently asked questions

Yes, under the Trump administration, the individual mandate penalty (the fine for not having health insurance) was effectively repealed starting in 2019 as part of the Tax Cuts and Jobs Act of 2017.

Before the repeal, the fine for not having health insurance under the Affordable Care Act (ACA) was calculated as either a percentage of household income (2.5%) or a flat fee per person ($695 for adults, $347.50 for children), whichever was higher, up to a family maximum.

No, the repeal of the fine does not mean health insurance is no longer required. The ACA’s individual mandate still exists, but the penalty for not having coverage was reduced to $0 at the federal level. Some states, however, have implemented their own penalties for lacking insurance.

Yes, the fine could be reinstated if future legislation or policy changes are enacted. The repeal was a result of a specific law passed during the Trump administration, and Congress could choose to restore the penalty through new legislation.