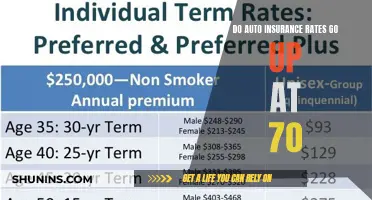

Car insurance rates for those aged 80 and above are among the highest, with rates for an 80-year-old driver being comparable to those of a teenager. This is due to older individuals being more prone to accidents and sustaining graver injuries in the event of a collision.

| Characteristics | Values |

|---|---|

| Age auto insurance rates increase | 70, 75, 80 |

| Average annual full coverage rate for 65-year-old | $1,740 |

| Average annual full coverage rate for 75-year-old | $2,008 |

| Average cost of car insurance in 2023 | $2,014 per year |

| Average cost of car insurance in 2024 | $2,299 per year |

Explore related products

What You'll Learn

- Car insurance rates for seniors start to increase at 65

- The average cost of car insurance for a 65-year-old is $1,740 a year

- Seniors can take a defensive driving course to reduce their premiums

- Senior drivers with a history of accidents will be penalised the most at Geico

- Senior drivers can expect a sharp increase in auto insurance rates at 80

![]()

Car insurance rates for seniors start to increase at 65

The cost of car insurance for seniors depends on various factors, including age, driving record, address, vehicle make and model, credit report, and coverage limits. While rates typically increase after age 65, they may not always do so, depending on state laws and insurance company guidelines. Some companies offer lower rates to those between 50 and 65, as this group has lower accident rates.

To save on car insurance, seniors can take advantage of mature driver discounts, which are offered by many insurance companies for drivers of a certain age with clean records. Additionally, seniors can attend an approved driving course to qualify for a discount. Other ways for seniors to save on car insurance include lowering annual mileage, bundling policies, and maintaining a good driving record.

While car insurance rates for seniors may increase, it is important to note that they will not reach the high rates of teenage drivers. Seniors can also benefit from discounts and take steps to improve their driving skills and safety to mitigate the impact of age-related factors on their insurance premiums.

Progressive Auto Insurance: Good or Bad?

You may want to see also

Explore related products

![]()

The average cost of car insurance for a 65-year-old is $1,740 a year

The cost of car insurance is influenced by a variety of factors, including age, gender, location, driving record, credit score, and vehicle type. While age is not the only factor that impacts car insurance rates, it is one of the most significant.

Car insurance rates are typically the highest for teens and young adults due to their lack of driving experience and higher likelihood of accidents. As drivers gain more experience and enter their mid-20s to mid-50s, insurance rates generally decrease. This is because insurance companies consider experienced drivers to be less likely to file claims, making them cheaper to insure.

However, as drivers reach their senior years, insurance rates start to increase again. This is usually due to risk factors associated with older age groups, such as vision or hearing loss, slower reflexes, and overall health changes. The average cost of car insurance for a 65-year-old is $1,740 per year for full coverage, according to Insurance.com. This is a notable increase from the average cost of car insurance for a 50-year-old, which is around $1,400 per year.

It is important to note that insurance rates can vary depending on other factors such as location and driving record. For example, in some states like California, Hawaii, and Massachusetts, age is not permitted to be used as a rating factor in car insurance rates. Additionally, insurance companies may offer discounts for senior drivers who take defensive driving courses or have a clean driving record, which can help offset the increase in insurance rates.

Overall, while age 65 may mark the beginning of higher car insurance rates, there are still ways to mitigate these costs and ensure safe and affordable coverage for senior drivers.

Insurance Claims: Recovered Vehicle

You may want to see also

Explore related products

![]()

Seniors can take a defensive driving course to reduce their premiums

While auto insurance rates do not automatically go up at age 80, it is common for rates to increase for seniors. This is because older individuals are considered more likely to be involved in an accident due to potential physical, cognitive, or visual impairments. However, seniors can take a defensive driving course to reduce their premiums.

Defensive driving courses are designed to educate drivers on collision prevention techniques and encourage courtesy and cooperation on the road. These courses can be taken online, in a classroom, or behind the wheel, and typically cover topics such as crash prevention techniques, safe following distances, and how to safely share the road. They are often affordable, ranging from $15 to $100, and can result in significant savings on car insurance premiums.

Many states have mandated mature driver discounts for seniors who complete state-approved driving courses. Organizations such as AARP, AAA, and The National Safety Council (NSC) offer these courses, which can lead to discounts of up to 20% on car insurance policies. For example, completing the AARP Smart Driver online course can qualify seniors for a multi-year discount on their car insurance. Similarly, the AAA Driver Improvement Program is designed to reduce the risk of seniors behind the wheel and can result in lower insurance premiums.

In addition to these benefits, defensive driving courses can also help seniors get tickets or citations dismissed and remove points from their licenses. Overall, taking a defensive driving course is a great way for seniors to improve their driving skills, reduce their insurance premiums, and maintain their independence and mobility.

GEICO: Home and Auto Bundling

You may want to see also

Explore related products

$16.97 $18.99

![]()

Senior drivers with a history of accidents will be penalised the most at Geico

While auto insurance rates do not automatically go up at age 80, it is true that older adults are more likely to experience higher premiums. This is due to a variety of factors, including physical, cognitive, and visual impairments that can increase the risk of accidents. However, this does not automatically mean that seniors will pay more for coverage than younger drivers. It is important to remember that insurance companies use multiple criteria to assess a driver's level of risk and calculate their rate.

In addition to these discounts, Geico also offers a Prime Time contract for customers over the age of 50. To qualify, drivers must have no operators under the age of 25, have no violations or accidents in the past three years, and not use any vehicle for business purposes. This contract is not available in every state, but it can provide guaranteed renewal for eligible customers who may otherwise face non-renewal due to their age.

It is worth noting that, while accident history is a significant factor in determining insurance rates, other criteria are also considered. These include age, gender, location, credit score, vehicle type, and driving record. By taking advantage of discounts, maintaining a safe driving record, and comparing rates, senior drivers can help minimise the impact of age-related premium increases.

Gap Insurance: Partial Payment Explained

You may want to see also

Explore related products

![]()

Senior drivers can expect a sharp increase in auto insurance rates at 80

Younger and older drivers are generally considered more accident-prone and, therefore, riskier to insure. Teenagers lack driving experience and are more likely to take risks on the road, while older individuals may have physical, cognitive, or visual impairments that affect their driving ability. As a result, car insurance is typically most expensive for these two age groups.

Insurance rates decrease significantly from ages 19 to 34, stabilize from 34 to 75, and then begin to trend upward at 75. At 80, there is a considerable spike in insurance rates due to the increased risk of accidents and more severe injuries in the event of a collision.

In addition to age, insurance companies consider various other factors when determining rates, including driving experience, claims history, gender, marital status, education level, career, credit score, and location. It is important to note that not all states permit age as a rating factor, and some states have banned the use of gender as a factor.

To offset the higher costs of insurance for seniors, many companies offer discounts specifically for this age group. For example, seniors can often get a discount by completing a state-approved defensive driving course or by maintaining a safe driving record. Other ways to save on car insurance include bundling policies, paying the policy in full, increasing the deductible, and shopping around for the best rates.

Engine Failure: Is Your Car Insurance Useless?

You may want to see also

Frequently asked questions

Yes, auto insurance rates go up at age 80. This is because seniors are considered to be riskier to insure due to age-related changes in their health, such as hearing or vision loss, slower reflexes, and overall health changes.

In addition to age, the cost of auto insurance is influenced by gender, driving experience, coverage lapses, driving history, marital status, education level, career, credit score, and location.

There are several ways to lower auto insurance rates as a senior. These include taking a defensive driving course, maintaining a safe driving record, maintaining vehicle safety, and increasing your deductible. Additionally, you can also take advantage of discounts offered by auto insurance companies specifically for senior drivers.

Auto insurance rates are typically the highest for young and inexperienced drivers, with a significant drop occurring around age 25. Rates then stabilize or decrease slightly until around age 65, before increasing again at age 75 and above.