Health insurance is a critical component of financial planning, providing individuals and families with protection against high medical costs. However, many people are unaware that most health insurance plans come with a maximum limit, often referred to as the out-of-pocket maximum. This limit caps the total amount policyholders are required to pay for covered services in a given year, after which the insurance company assumes full responsibility for additional costs. Understanding this maximum is essential, as it directly impacts budgeting and decision-making regarding healthcare expenses. While the out-of-pocket maximum varies by plan, it typically includes deductibles, copayments, and coinsurance, but excludes premiums. Knowing this limit can help individuals anticipate their financial liability and choose a plan that aligns with their healthcare needs and financial situation.

| Characteristics | Values |

|---|---|

| Maximum Coverage Limit | Most health insurance plans have a maximum coverage limit, which is the highest amount the insurer will pay for covered services in a policy period (usually a year). |

| Out-of-Pocket Maximum | This is the most a policyholder will pay out of pocket for covered services in a year, including deductibles, copayments, and coinsurance. After reaching this limit, the insurer covers 100% of covered expenses. |

| Lifetime Maximum | Some plans have a lifetime maximum, capping the total amount the insurer will pay over the policyholder's lifetime. However, this is less common since the Affordable Care Act (ACA) eliminated lifetime limits for essential health benefits. |

| Annual Maximum | Many dental and vision insurance plans have annual maximums, limiting the amount they will pay for services each year. |

| Maximum Reimbursement | In reimbursement-based plans, there is a maximum amount the insurer will reimburse for specific services or treatments. |

| Maximum Number of Visits | Some plans limit the number of covered visits to certain providers (e.g., therapy sessions, specialist visits) per year. |

| Maximum Prescription Coverage | Prescription drug coverage often has limits on the amount or cost of medications covered, sometimes tiered by drug type. |

| Maximum Age Limit | Some health insurance plans, especially in certain countries, may have maximum age limits for enrollment or coverage. |

| Maximum Pre-Authorization Requirements | Certain high-cost treatments or procedures may require pre-authorization and have maximum coverage limits. |

| Maximum Network Coverage | Out-of-network services may have lower maximum coverage limits compared to in-network services. |

Explore related products

What You'll Learn

- Lifetime Maximum Limits: Caps on total payouts over policyholder's lifetime, varies by plan and provider

- Annual Maximum Coverage: Limits on benefits paid per year, resets annually, affects out-of-pocket costs

- Maximum Out-of-Pocket Costs: Highest amount paid annually before insurance covers 100% of expenses

- Maximum Room Rent in Policies: Defines daily or total room rent coverage in hospitalization plans

- Maximum Pre-Existing Coverage: Waiting periods and caps for pre-existing conditions, varies by insurer

![]()

Lifetime Maximum Limits: Caps on total payouts over policyholder's lifetime, varies by plan and provider

Health insurance policies often include lifetime maximum limits, a critical yet frequently overlooked detail that can significantly impact long-term financial security. These caps dictate the total amount an insurer will pay out over a policyholder’s lifetime, varying widely by plan and provider. For instance, while some high-end plans may offer lifetime maximums exceeding $5 million, more affordable options might cap payouts at $1 million or less. Understanding this limit is essential, as exceeding it could leave policyholders responsible for all subsequent medical expenses, potentially leading to catastrophic financial strain.

Consider a scenario where a 45-year-old individual with a $2 million lifetime maximum undergoes a $500,000 cancer treatment. If they later require a $1.8 million organ transplant, the insurer would only cover $1.5 million, leaving the policyholder to pay the remaining $300,000 out of pocket. This example underscores the importance of aligning lifetime maximums with personal health risks and financial capacity. For those with chronic conditions or a family history of costly illnesses, opting for a higher cap—despite the increased premium—may be a prudent investment.

When evaluating plans, policyholders should scrutinize not only the lifetime maximum but also the provider’s track record for approving high-cost treatments. Some insurers may impose additional restrictions, such as excluding certain procedures or requiring pre-authorization for expensive care. For example, a plan with a $3 million lifetime maximum might exclude experimental therapies, effectively reducing its practical value for patients with rare or complex conditions. Prospective buyers should request detailed policy documents and consult with a healthcare advocate to fully understand these nuances.

A practical tip for maximizing coverage is to periodically reassess your insurance needs, especially after significant life changes like marriage, childbirth, or a new diagnosis. For instance, a young professional with a $1 million lifetime maximum might find this adequate in their 20s but insufficient after developing a chronic illness in their 40s. Switching to a plan with a higher cap during open enrollment or a qualifying life event can mitigate future risks. Additionally, pairing health insurance with supplemental policies, such as critical illness or disability insurance, can provide a financial buffer if the lifetime maximum is reached.

In conclusion, lifetime maximum limits are a double-edged sword in health insurance—offering protection up to a point but potentially exposing policyholders to substantial risk beyond that threshold. By carefully selecting a plan, staying informed about policy details, and proactively adjusting coverage as health needs evolve, individuals can navigate this limitation more effectively. Ignoring this aspect could lead to unforeseen financial hardship, while strategic planning ensures that insurance remains a reliable safety net throughout life.

Insurance Companies Requiring Only 3 Years Claims History Revealed

You may want to see also

Explore related products

![]()

Annual Maximum Coverage: Limits on benefits paid per year, resets annually, affects out-of-pocket costs

Health insurance policies often include an annual maximum coverage limit, a cap on the total amount the insurer will pay for covered services within a policy year. This limit is a critical component of your plan, directly influencing your out-of-pocket expenses and overall financial risk. For instance, if your policy has an annual maximum of $1,000,000, once claims reach this threshold, you’re responsible for all additional costs until the plan resets the following year. Understanding this limit is essential for budgeting and planning, especially if you anticipate high medical expenses due to chronic conditions or planned procedures.

Consider a scenario where a 45-year-old individual with diabetes requires insulin, specialist visits, and lab tests. Insulin alone can cost $300–$900 per month, and without an annual maximum, expenses could spiral. However, with a $1,000,000 cap, the insurer covers these costs until the limit is met, after which the individual must pay out-of-pocket. This example highlights how annual maximum coverage acts as both a safety net and a potential financial boundary. It’s crucial to review this limit alongside deductibles and coinsurance to fully grasp your exposure to costs.

From a strategic perspective, annual maximum coverage resets every year, offering a fresh start for benefit utilization. This reset is particularly beneficial for those who exceeded their limit in the previous year, as it restores access to covered services without prior-year expenses carrying over. However, it also means that ongoing treatments or conditions may require reevaluation of costs annually. For example, a patient undergoing chemotherapy might need to reassess their out-of-pocket burden each year, as the annual reset could impact their financial planning for continuous care.

To navigate annual maximum coverage effectively, follow these steps: first, identify your policy’s specific limit by reviewing your Summary of Benefits. Second, estimate your annual medical expenses based on past usage and anticipated needs. Third, compare this estimate to your coverage limit to gauge potential out-of-pocket exposure. Finally, consider supplemental insurance or health savings accounts (HSAs) to mitigate risks if your expected costs approach the maximum. For instance, an HSA allows you to save pre-tax dollars for medical expenses, providing a buffer if you reach your annual limit.

A cautionary note: annual maximum coverage does not apply to all services. Some policies exclude certain treatments, such as cosmetic procedures or experimental therapies, from this limit. Additionally, out-of-network care may not count toward the maximum, leaving you vulnerable to higher costs. Always verify which services are covered and how they contribute to the limit. For example, a policy might cover up to $500,000 for in-network hospitalization but exclude out-of-network emergency room visits from the annual maximum, exposing you to significant expenses.

In conclusion, annual maximum coverage is a double-edged sword—it caps insurer liability while resetting annually to provide renewed benefits. By understanding this limit and its implications, you can better manage out-of-pocket costs and make informed decisions about your healthcare. Pairing this knowledge with strategic financial planning, such as using HSAs or supplemental insurance, ensures you’re prepared for both expected and unexpected medical expenses. Always scrutinize your policy details to avoid surprises and maximize the value of your coverage.

Dollar General's Medical Insurance: What's Covered?

You may want to see also

Explore related products

![]()

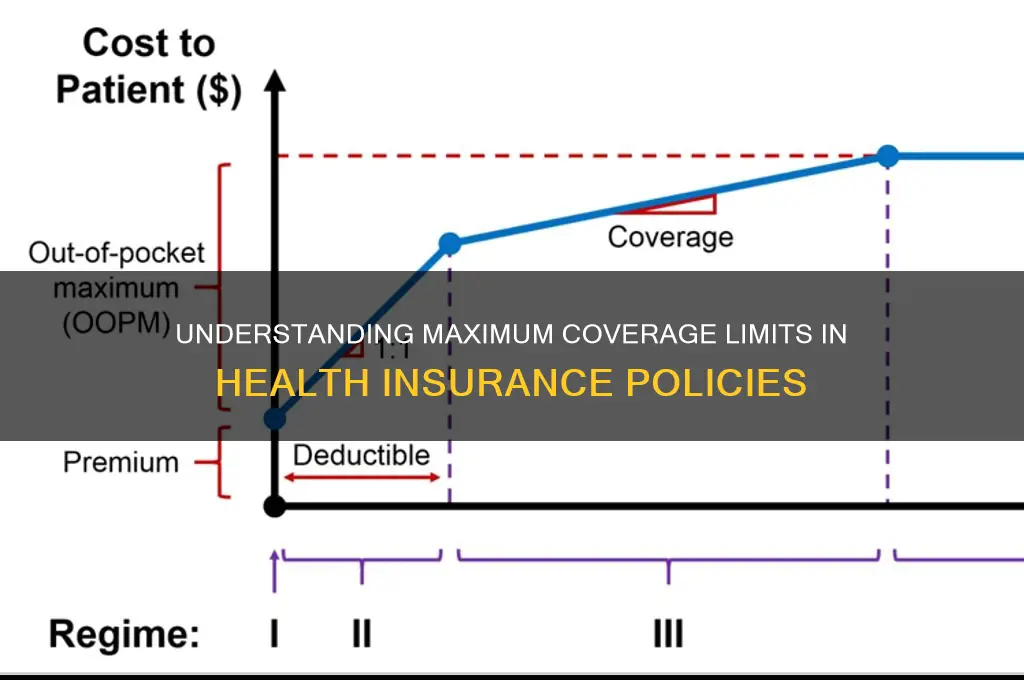

Maximum Out-of-Pocket Costs: Highest amount paid annually before insurance covers 100% of expenses

Health insurance plans often include a maximum out-of-pocket (MOOP) limit, a critical yet frequently overlooked feature. This cap represents the highest amount you’ll pay annually for covered services before your insurance takes over, covering 100% of additional expenses. For instance, if your plan has a $5,000 MOOP and you’ve spent $4,500 on deductibles, copays, and coinsurance, the next $500 in covered costs will be your responsibility. Once you hit $5,000, the insurance covers everything else for the rest of the year. This safeguard prevents catastrophic financial strain from unexpected medical events, such as surgeries or chronic conditions requiring ongoing treatment.

Understanding how MOOP works requires breaking down its components. Deductibles, copays, and coinsurance all count toward this limit, but premiums do not. For example, if your plan has a $2,000 deductible, 20% coinsurance, and a $30 copay for specialist visits, all these payments accumulate until you reach the MOOP. However, not all services qualify. Some plans exclude out-of-network care or certain prescription drugs from the MOOP calculation, so scrutinize your policy details. Families should note that individual and family MOOPs may differ; a family plan might require each member to meet their own limit or set a collective cap, typically double the individual amount.

Choosing a plan with an appropriate MOOP depends on your health needs and financial situation. Lower MOOPs often come with higher premiums, ideal for those with chronic conditions or families anticipating significant medical expenses. Conversely, healthy individuals might opt for higher MOOPs to reduce monthly costs. For example, a 30-year-old with no pre-existing conditions might save hundreds annually by selecting a plan with a $7,000 MOOP instead of a $4,000 one. However, this trade-off requires careful consideration, as unexpected emergencies can quickly escalate costs.

Practical tips can help you maximize the benefits of your MOOP. First, track your out-of-pocket spending throughout the year using a spreadsheet or app to ensure you’re not overpaying. Second, verify that all eligible expenses are applied to your MOOP by regularly reviewing your Explanation of Benefits (EOB) statements. If you’re nearing the limit, schedule elective procedures or stock up on prescriptions to take advantage of full coverage. Finally, during open enrollment, compare MOOP limits across plans, factoring in both premiums and potential out-of-pocket costs to find the best balance for your budget and health needs.

Cancer Insurance: What to Say When Applying

You may want to see also

Explore related products

![]()

Maximum Room Rent in Policies: Defines daily or total room rent coverage in hospitalization plans

Health insurance policies often come with caps on room rent, a detail that can significantly impact your out-of-pocket expenses during hospitalization. This "maximum room rent" clause defines the upper limit your insurer will cover for your daily or total hospital stay. Exceed this limit, and you’re responsible for the difference, even if other policy benefits (like surgery or medication) are fully covered. For instance, a policy with a daily room rent cap of ₹5,000 means any room costing ₹7,000 per day leaves you paying ₹2,000 daily out of pocket.

Understanding this cap requires scrutinizing your policy’s fine print. Some plans set a flat daily rate, while others impose a total limit for the entire hospitalization period. For example, a policy might cap daily room rent at ₹6,000 but restrict total room expenses to ₹60,000 for a 10-day stay. If your actual room costs exceed these limits, the insurer prorates other expenses (like doctor fees or diagnostics) based on the capped room rate, further reducing your coverage. This proration rule is often overlooked but can drastically shrink your overall claim amount.

Choosing a policy with an appropriate room rent cap depends on your healthcare preferences and budget. If you prefer private rooms or hospitals with higher tariffs, opt for a plan with a higher cap or a "no room rent capping" feature, which eliminates this restriction altogether. However, such plans come with higher premiums. For instance, a policy with a ₹10,000 daily cap might cost 20–30% more than one with a ₹5,000 cap. Evaluate your city’s hospital rates and your financial cushion for unexpected costs before deciding.

A practical tip: During hospitalization, ask for an itemized bill to verify room charges align with your policy’s cap. If the hospital offers rooms within your policy’s limit, request a downgrade to avoid excess charges. Additionally, if you anticipate a long hospital stay, calculate whether the total room rent cap will suffice. For example, a 14-day stay in a ₹8,000 room under a ₹100,000 total cap leaves no room for error—exceeding this triggers proration for all expenses.

In conclusion, the maximum room rent clause is a critical yet often misunderstood aspect of health insurance. It’s not just about the room cost; it’s about how this cap cascades into reduced coverage for other medical expenses. By carefully selecting a policy, verifying hospital rates, and managing room choices during admission, you can minimize financial surprises and maximize your policy’s utility.

Top Insurance Providers Offering Annuity Plans: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Maximum Pre-Existing Coverage: Waiting periods and caps for pre-existing conditions, varies by insurer

Health insurance policies often impose waiting periods and coverage caps for pre-existing conditions, creating a complex landscape for individuals seeking comprehensive care. These limitations, which vary widely by insurer, can significantly impact access to treatment and financial stability. For instance, a policy might require a 12-month waiting period before covering expenses related to a pre-existing condition like diabetes or hypertension. During this time, the insured is responsible for all related medical costs, which can be financially crippling without proper planning. Understanding these restrictions is crucial for anyone navigating the health insurance market, especially those with chronic illnesses.

Consider the case of a 45-year-old with asthma, a condition often classified as pre-existing. Insurer A might impose a 24-month waiting period before covering asthma-related treatments, while Insurer B may cap annual coverage at $10,000 for such conditions. These disparities highlight the importance of comparing policies carefully. For example, if asthma medications cost $300 monthly, the insured under Insurer B would face out-of-pocket expenses after reaching the $10,000 cap, despite the absence of a waiting period. Such scenarios underscore the need to evaluate both waiting periods and coverage limits when selecting a plan.

To mitigate the impact of these restrictions, individuals should adopt a proactive approach. First, review the policy’s definition of pre-existing conditions, as this varies by insurer. For example, some may exclude conditions treated within the last six months, while others look back two years. Second, consider supplemental insurance or health savings accounts (HSAs) to cover gaps during waiting periods. For instance, an HSA allows tax-free savings for medical expenses, providing a financial cushion. Third, negotiate with insurers or seek employer-sponsored plans, which often have more lenient terms for pre-existing conditions due to group coverage benefits.

A comparative analysis reveals that while some insurers prioritize affordability with lower premiums but stricter caps, others offer higher coverage limits at a premium. For example, a policy with a $5,000 annual cap for pre-existing conditions might cost $200 monthly, while one with a $20,000 cap could cost $400. The choice depends on individual health needs and financial capacity. Those with stable, manageable conditions might opt for lower premiums, while those requiring frequent treatments should prioritize higher coverage limits. This trade-off between cost and coverage is a critical consideration in policy selection.

In conclusion, navigating maximum pre-existing coverage requires a strategic approach. By understanding waiting periods, coverage caps, and policy nuances, individuals can make informed decisions. Practical steps, such as comparing insurers, utilizing supplemental options, and negotiating terms, can help manage these limitations effectively. Ultimately, the goal is to secure a policy that balances affordability with adequate coverage, ensuring financial protection without compromising access to necessary care.

MVP Insurance and Medicare: What You Need to Know

You may want to see also

Frequently asked questions

Yes, most health insurance plans have a maximum limit, often referred to as the "lifetime maximum" or "annual maximum," which caps the total amount the insurer will pay for covered services.

Once the maximum limit is reached, the insured individual is typically responsible for paying all additional medical expenses out of pocket, unless they switch to a new plan or policy.

Yes, some comprehensive health insurance plans, especially those offered by employers or government programs, may not have a maximum limit, providing unlimited coverage for covered services.

Yes, the ACA prohibits health insurance plans from imposing lifetime dollar limits on essential health benefits, though some plans may still have annual limits on specific services.

You can review your plan’s Summary of Benefits and Coverage (SBC) or contact your insurance provider directly to understand the specific maximum limits and coverage details.

![Designed for Boost Summit 5G Phone Case with Tempered Glass Screen Protector [Maximum Coverage], Full-Body Protective [Dual Layer Hybrid] Shockproof Cover Case for Boost Mobile Summit 5G (Green)](https://m.media-amazon.com/images/I/81XlXZt4BwL._AC_UL320_.jpg)