The relationship between health insurance premiums and wages is a topic of significant interest, as many individuals wonder whether their insurance costs rise in tandem with their earnings. Health insurance premiums are typically determined by a variety of factors, including age, location, coverage level, and the specific plan chosen. While wages themselves are not a direct factor in premium calculations, there is an indirect connection. Employers often subsidize health insurance plans, and as wages increase, employers might adjust their contributions or offer more comprehensive plans, which could lead to higher premiums for employees. Additionally, in some regions, government-subsidized health insurance programs may have income-based eligibility criteria, causing premiums to increase as income rises. Understanding this dynamic is crucial for employees to anticipate potential changes in their healthcare costs as their wages fluctuate.

| Characteristics | Values |

|---|---|

| General Trend | Health insurance premiums often increase with higher wages, but this is not universal and depends on various factors. |

| Employer-Sponsored Plans | Premiums may rise with wages if the employer adjusts contributions based on salary tiers. |

| Individual Market Plans | Premiums are primarily based on age, location, and plan type, not directly on income. However, higher wages may lead to reduced subsidies under the Affordable Care Act (ACA), effectively increasing out-of-pocket costs. |

| ACA Subsidies | Subsidies decrease as income rises, potentially increasing net premium costs for higher-wage earners. |

| Group Size and Negotiation | Larger employers may negotiate better rates, mitigating premium increases tied to wages. |

| State Regulations | Some states have regulations limiting how much premiums can increase based on income or other factors. |

| Cost-Sharing Mechanisms | Higher wages may lead to plans with lower subsidies but higher premiums for comprehensive coverage. |

| Inflation and Healthcare Costs | Premiums generally rise with inflation and healthcare costs, affecting all wage levels. |

| Income-Based Premiums (Rare) | Some plans may directly tie premiums to income, but this is uncommon in most markets. |

| Tax Implications | Higher wages may push individuals into higher tax brackets, indirectly affecting insurance costs through reduced subsidies or tax credits. |

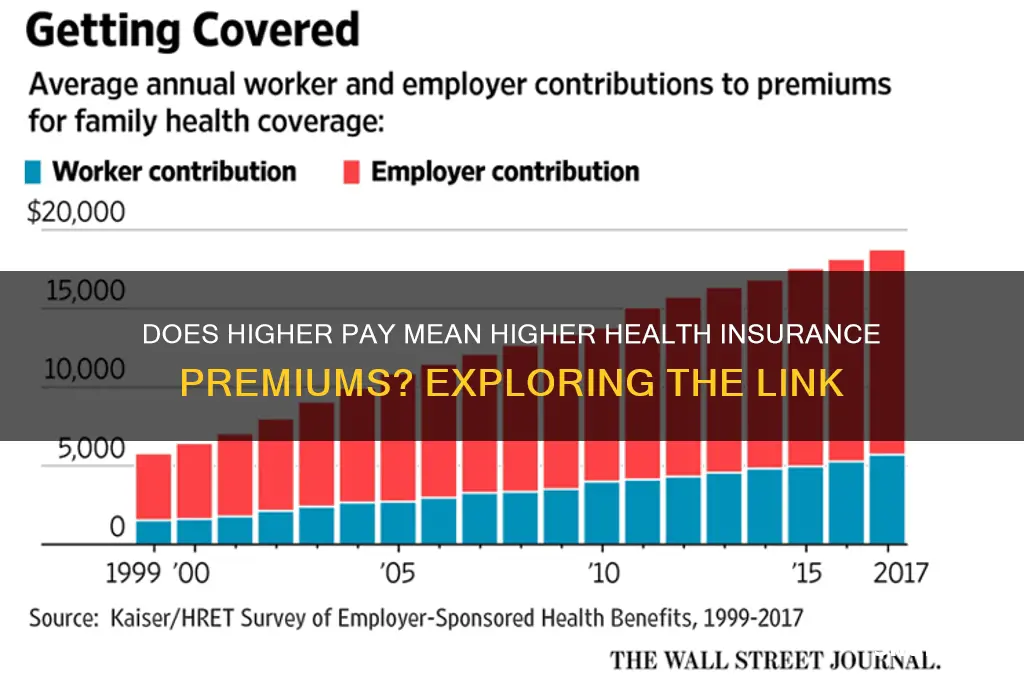

| Latest Data (as of 2023) | Average annual premiums for employer-sponsored family coverage reached $22,463, with employees paying $6,106 on average. Individual market premiums vary widely but are less directly tied to wages. |

| Key Takeaway | While premiums may not directly increase with wages, higher income can reduce subsidies, effectively increasing costs for some individuals. |

Explore related products

What You'll Learn

![]()

Impact of Income on Premium Calculation

Health insurance premiums are not universally tied to income, but in certain systems, income does play a pivotal role in determining costs. For instance, in the United States, the Affordable Care Act (ACA) uses income as a basis for calculating premiums for individuals purchasing plans through the Health Insurance Marketplace. Premiums are capped as a percentage of household income, ensuring that coverage remains affordable for lower-income individuals. For example, a person earning 150% of the federal poverty level (FPL) may pay no more than 4.14% of their income for a benchmark plan, while someone at 400% FPL might pay up to 9.83%. This sliding scale highlights how income directly influences premium costs in specific contexts.

In contrast, employer-sponsored health insurance in the U.S. typically does not adjust premiums based on individual wages. Instead, employers often cover a significant portion of the premium cost, and employees pay a flat rate regardless of their salary. However, higher-income employees may still feel the impact indirectly, as they are less likely to qualify for subsidies or tax credits that lower-income individuals receive. This disparity underscores the importance of understanding how income interacts with different insurance structures.

Globally, the relationship between income and premiums varies widely. In countries with universal healthcare systems, such as Canada or the UK, premiums are either nonexistent or not directly tied to income, as healthcare is funded through taxation. Conversely, in private insurance markets like those in India or South Africa, premiums may increase with income due to the demand for more comprehensive coverage. For example, a high-income individual in India might opt for a premium plan with lower deductibles and broader coverage, resulting in higher costs compared to a basic plan.

For those navigating income-based premium calculations, practical strategies can help manage costs. First, accurately estimate your household income when enrolling in ACA plans to ensure you receive the correct subsidies. Second, consider Health Savings Accounts (HSAs) if you’re in a higher income bracket, as they offer tax advantages for medical expenses. Finally, review your coverage annually, especially if your income fluctuates, to avoid overpaying or missing out on available discounts. Understanding these dynamics empowers individuals to make informed decisions about their health insurance.

In summary, while income does not universally dictate health insurance premiums, its impact is significant in specific systems and contexts. From ACA subsidies to global private insurance markets, income-based calculations shape affordability and access. By grasping these nuances and employing practical strategies, individuals can navigate the complexities of premium determination more effectively.

Why Insurance Companies Use Automated Calls: Understanding Robocalls

You may want to see also

Explore related products

![]()

Employer-Sponsored Plans vs. Wage Increases

Employer-sponsored health insurance plans often tie premiums to employee wages, creating a complex interplay between compensation and healthcare costs. While wage increases are generally seen as a financial benefit, they can inadvertently lead to higher health insurance premiums for employees. This occurs because many employers calculate premium contributions as a percentage of an employee’s salary, meaning higher wages result in larger deductions. For instance, if an employer covers 80% of a premium that is 5% of an employee’s salary, a $10,000 raise from $50,000 to $60,000 could increase the employee’s annual premium contribution by $200. This dynamic highlights the need for employees to weigh the net gain of a wage increase against potential rises in healthcare costs.

From an employer’s perspective, linking health insurance premiums to wages can serve as a cost-management strategy. By structuring contributions as a percentage of salary, employers ensure that their share of premiums remains proportional to employee earnings. However, this approach can create unintended consequences, such as discouraging employees from accepting raises or promotions if they perceive the net benefit as minimal. For example, a mid-level manager earning $75,000 might hesitate to take a promotion to $90,000 if the combined increase in premiums and taxes significantly erodes the additional income. Employers must balance this cost-sharing model with employee satisfaction to avoid stifling career growth.

Employees navigating this landscape should proactively assess how wage increases impact their overall compensation. A practical tip is to request a detailed breakdown of pre- and post-raise deductions, including health insurance premiums, taxes, and retirement contributions. Tools like online paycheck calculators can help estimate net pay after a salary adjustment. Additionally, employees should explore whether their employer offers alternative benefit structures, such as flat-rate premiums or tiered contribution models, which decouple premiums from wages. Negotiating for non-monetary benefits, like flexible work arrangements or additional vacation days, can also offset the perceived loss from higher premiums.

The comparison between employer-sponsored plans and wage increases underscores the importance of transparency and flexibility in benefits design. Employers can mitigate employee concerns by offering clear communication about how premiums are calculated and providing options that cater to diverse financial situations. For instance, a tech company might introduce a hybrid model where employees choose between percentage-based or fixed premium contributions. Similarly, employees should advocate for themselves by understanding their benefits package and negotiating terms that align with their long-term financial goals. Ultimately, the goal is to ensure that wage increases remain a positive incentive rather than a source of financial stress.

Meet the CEO of CSAA Insurance Group: Leadership and Vision

You may want to see also

Explore related products

![]()

Individual Market Premiums and Earnings

Health insurance premiums in the individual market often reflect a complex interplay between earnings and affordability. Unlike employer-sponsored plans, where premiums are typically fixed or subsidized, individual market premiums are influenced by income-based factors. For instance, under the Affordable Care Act (ACA), premium tax credits are available to individuals earning between 100% and 400% of the federal poverty level (FPL). As earnings rise within this range, the percentage of income required to pay premiums increases, effectively tying premium costs to wage levels. This sliding scale ensures that insurance remains affordable for lower-income individuals but can lead to higher premiums for those nearing the 400% FPL threshold.

Consider a 40-year-old individual in a state using the federal marketplace. At 200% FPL ($27,180 annually), they might pay around 6.3% of their income for a benchmark silver plan, equating to roughly $143 per month. However, at 300% FPL ($40,770 annually), their premium contribution rises to 9.5% of income, or approximately $325 per month. This example illustrates how premiums scale with earnings, even within subsidized brackets. Above 400% FPL, subsidies disappear entirely, leaving individuals to pay the full premium cost, which can be significantly higher depending on age, location, and plan choice.

A critical takeaway is that while higher wages may increase premium costs, they also often correlate with better access to comprehensive coverage. For example, individuals earning above 400% FPL might opt for gold or platinum plans, which offer lower out-of-pocket costs but come with higher premiums. Conversely, those with lower earnings may select bronze plans with lower premiums but higher deductibles, balancing affordability with coverage needs. Understanding this trade-off is essential for making informed decisions in the individual market.

To navigate this landscape effectively, individuals should assess their total healthcare costs, not just premiums. For instance, a higher-earning individual might prioritize a plan with a $500 deductible and $400 monthly premium if they anticipate frequent medical needs, while someone with fewer health concerns might opt for a $7,000 deductible plan with a $200 premium. Tools like Healthcare.gov’s subsidy calculator can help estimate costs based on income, while consulting a broker can provide personalized guidance. Ultimately, aligning premium costs with earnings and healthcare needs ensures optimal value in the individual market.

Proton Therapy Coverage: Which Insurers Support Prostate Cancer Treatment?

You may want to see also

Explore related products

![]()

Government Subsidies and Wage Thresholds

Health insurance premiums often fluctuate with income, but government subsidies can mitigate this effect—up to a point. Many countries, including the United States, tie subsidy eligibility to wage thresholds, creating a system where earning more can paradoxically reduce financial assistance. For instance, under the Affordable Care Act (ACA), individuals earning between 100% and 400% of the federal poverty level (FPL) qualify for premium tax credits. However, crossing the 400% FPL threshold eliminates this subsidy entirely, leaving individuals to shoulder the full cost of premiums, which can increase significantly with higher wages.

Consider a practical example: A single individual earning $50,000 annually (approximately 385% of the FPL in 2023) might receive a substantial subsidy, reducing their monthly premium to $200. If their income rises to $60,000 (exceeding 400% FPL), they lose eligibility for subsidies, and their premium could jump to $500 or more, depending on the plan. This "subsidy cliff" highlights the delicate balance between wage growth and healthcare affordability, underscoring the need for careful financial planning around income thresholds.

To navigate this system effectively, individuals should monitor their income relative to FPL thresholds annually. Tools like the ACA’s subsidy calculator can estimate eligibility based on projected earnings. For those nearing the 400% FPL threshold, strategies such as contributing to tax-advantaged accounts (e.g., HSAs or 401(k)s) can reduce taxable income, potentially preserving subsidy eligibility. Additionally, understanding state-specific programs or employer-sponsored plans can provide alternative avenues for cost savings.

Critics argue that rigid wage thresholds create disincentives for career advancement, as workers may avoid raises or promotions to retain subsidies. Policymakers could address this by phasing out subsidies gradually rather than abruptly, ensuring smoother transitions as incomes rise. Until such reforms materialize, individuals must proactively manage their finances, treating wage thresholds not as barriers but as benchmarks for strategic healthcare planning.

Occupational Therapy: Is Medical Insurance Enough?

You may want to see also

Explore related products

![]()

Wage-Based Premium Adjustments Over Time

Health insurance premiums often reflect an individual's ability to pay, and wage-based adjustments are a common mechanism insurers use to calibrate costs. Over time, as wages fluctuate, premiums may follow suit, creating a dynamic relationship between earnings and healthcare expenses. This practice, while controversial, is rooted in the principle of income-based fairness, where higher earners contribute more to the risk pool. However, it raises questions about affordability and equity, especially for those experiencing wage volatility or stagnation. Understanding how these adjustments work—and their long-term implications—is crucial for individuals navigating the complexities of health insurance.

Consider a scenario where an employee receives a 10% wage increase. In some employer-sponsored plans, this could trigger a proportional rise in their premium contribution, often through payroll deductions. For instance, if an employee previously paid $200 monthly, a 10% wage increase might elevate their premium to $220. While this seems straightforward, the cumulative effect over time can be significant. Over a decade, with annual wage increases averaging 3%, premiums could rise by 30% or more, assuming a direct correlation. This underscores the importance of budgeting for healthcare costs as wages grow, particularly in plans with wage-indexed premiums.

Not all wage-based adjustments are linear or predictable. Some insurers use tiered systems, where premiums increase only after crossing specific income thresholds. For example, a plan might charge a flat rate until an individual earns $50,000 annually, then apply a 2% premium increase for every $10,000 above that. Such structures aim to balance fairness with affordability, ensuring low-wage earners aren’t disproportionately burdened. However, they require careful scrutiny, as thresholds and percentages vary widely across plans and providers. Employees should review their plan’s wage-adjustment policy annually to anticipate changes and plan accordingly.

The long-term impact of wage-based premium adjustments extends beyond immediate costs. For younger workers, whose wages typically rise steadily, these adjustments may seem manageable. However, as individuals approach retirement age, wage growth often slows or stops, while healthcare needs—and costs—increase. This mismatch can lead to financial strain, particularly if premiums continue to rise based on past earnings. To mitigate this, individuals should explore options like health savings accounts (HSAs) or supplemental insurance policies that decouple premiums from wages. Additionally, advocating for policy reforms that cap premium increases or delink them from wages altogether can provide long-term relief.

In conclusion, wage-based premium adjustments are a double-edged sword. While they aim to distribute healthcare costs equitably, they can introduce unpredictability and financial stress, especially over time. By understanding the mechanics of these adjustments, individuals can make informed decisions, from choosing the right insurance plan to advocating for systemic changes. Proactive planning—such as monitoring wage thresholds, diversifying healthcare savings, and staying informed about policy trends—is key to navigating this evolving landscape. Ultimately, the goal is to ensure that health insurance remains accessible and affordable, regardless of how wages fluctuate.

Managing High Blood Pressure: Can Insurance Deny You?

You may want to see also

Frequently asked questions

Health insurance premiums may increase with a higher wage if your employer uses a tiered contribution model or if your income affects your eligibility for subsidies in individual plans.

Some employers may adjust the employee contribution for health insurance based on salary tiers, but this varies by company policy and is not universal.

If your employer ties premium contributions to salary levels, a raise or promotion could lead to a slight increase in your share of the premiums.

Yes, a higher wage may reduce or eliminate eligibility for premium tax credits, potentially increasing your out-of-pocket costs for individual health insurance plans.