Health insurance companies operate as for-profit entities in many markets, generating revenue through premiums paid by policyholders while managing costs associated with medical claims, administrative expenses, and reserves. While their primary function is to provide financial protection against healthcare expenses, insurers aim to maintain profitability by carefully balancing risk pools, setting actuarially sound premiums, and investing surplus funds. Critics argue that profit motives may conflict with patient care, leading to denied claims or limited coverage, while proponents highlight the efficiency and innovation that market-driven models can bring. Understanding how health insurers earn profit requires examining their revenue streams, cost management strategies, and the broader regulatory environment in which they operate.

| Characteristics | Values |

|---|---|

| Profitability | Yes, health insurance companies can and do earn profits. In 2022, the U.S. health insurance industry reported a profit margin of approximately 3-5%, varying by company and market conditions. |

| Revenue Sources | Premiums from policyholders, investment income, and administrative fees. |

| Expenses | Claims payouts, administrative costs, marketing, and regulatory compliance. |

| Market Leaders | UnitedHealth Group, Anthem, Aetna, and Humana are among the top profitable health insurers in the U.S. as of 2023. |

| Profit Drivers | Efficient claims management, investment returns, and scale economies. |

| Regulatory Impact | Profitability is influenced by regulations like the Affordable Care Act (ACA), which caps administrative costs and profit margins in some markets. |

| Global Trends | Health insurers in developed countries like the U.S., Germany, and Switzerland consistently report profits, while profitability varies in emerging markets. |

| Challenges | Rising healthcare costs, regulatory changes, and increased competition can impact profit margins. |

| Latest Data (2023) | UnitedHealth Group reported a net income of $20.8 billion in 2022, with a profit margin of ~5.5%. |

Explore related products

What You'll Learn

- Revenue Sources: Premiums, investments, and additional fees contribute to health insurance companies' income streams

- Claim Payouts: Balancing premiums with medical claim costs is crucial for profitability

- Administrative Costs: Overhead expenses impact profit margins significantly in health insurance operations

- Market Competition: Competitive pricing and market share influence profit potential in the industry

- Regulatory Impact: Government policies and regulations can limit or enhance profit opportunities

![]()

Revenue Sources: Premiums, investments, and additional fees contribute to health insurance companies' income streams

Health insurance companies generate revenue through a multifaceted approach, primarily relying on premiums, investments, and additional fees. Premiums, the most straightforward income stream, are the regular payments policyholders make to maintain coverage. These payments are calculated based on factors like age, health status, and coverage level, ensuring a steady cash flow for insurers. For instance, a 30-year-old individual might pay $300 monthly for a comprehensive plan, while a family of four could pay upwards of $1,200, depending on their needs and risk profile.

Beyond premiums, insurers leverage investments to grow their income. They pool policyholders’ premiums into large portfolios, investing in bonds, stocks, and real estate to generate returns. This strategy not only offsets administrative costs but also builds reserves for future claims. For example, a major insurer might allocate 60% of its portfolio to low-risk government bonds and 40% to higher-yielding equities, balancing stability with growth potential. However, this approach carries risks, as market volatility can impact investment returns, affecting profitability.

Additional fees serve as a supplementary revenue source, often derived from policy add-ons, late payments, or administrative charges. For instance, a policyholder might pay a $50 fee for adding a dependent mid-term or a $25 penalty for missing a premium payment deadline. While these fees may seem minor, they collectively contribute significantly to insurers’ bottom lines. A large insurer with millions of policyholders could generate millions annually from such fees alone, highlighting their importance in the revenue mix.

Understanding these revenue streams reveals the delicate balance insurers must maintain. Premiums provide stability, investments offer growth potential, and fees supplement income. However, this model is not without challenges. Regulatory changes, rising healthcare costs, and economic downturns can disrupt these streams, forcing insurers to adapt. For consumers, this underscores the importance of scrutinizing policies to ensure they receive value for their premiums while being mindful of potential hidden fees.

In practice, policyholders can optimize their insurance experience by negotiating premiums, understanding investment-linked policies, and avoiding unnecessary fees. For example, opting for annual premium payments instead of monthly installments can save up to 5% in administrative fees. Similarly, choosing plans with transparent investment strategies can provide insight into how premiums are utilized. By grasping these revenue sources, both insurers and policyholders can navigate the complex landscape of health insurance more effectively, ensuring sustainability and value for all stakeholders.

Arizona Medical Insurance: Where to Apply

You may want to see also

Explore related products

![]()

Claim Payouts: Balancing premiums with medical claim costs is crucial for profitability

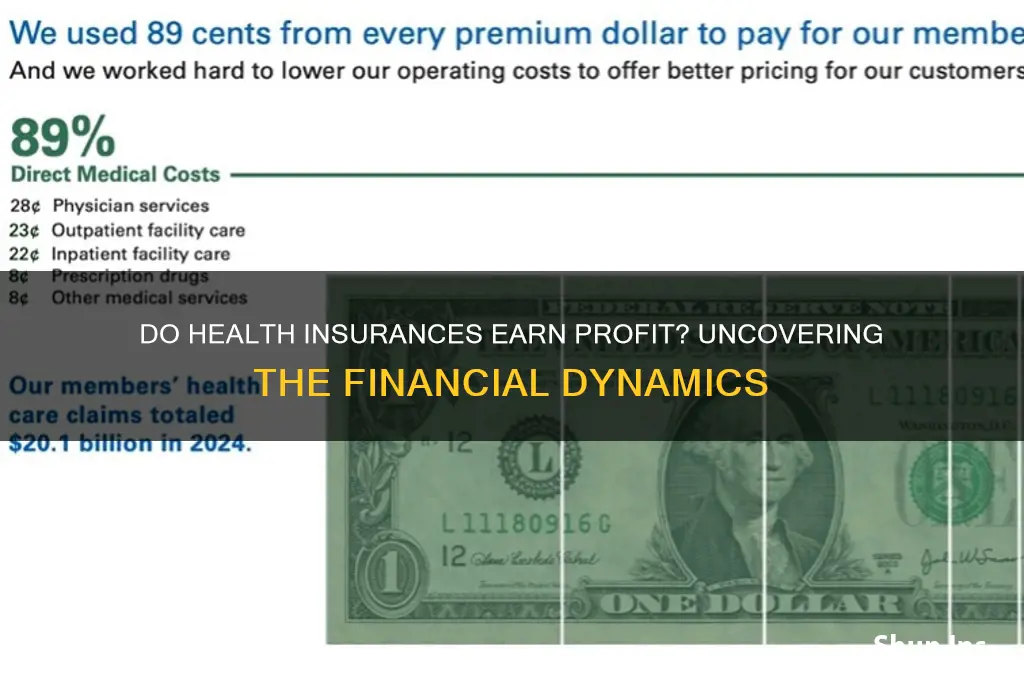

Health insurance companies operate on a delicate financial tightrope, where the premiums collected from policyholders must sufficiently cover the costs of medical claims paid out. This balance is not merely a matter of arithmetic but a strategic imperative that determines profitability. For instance, a 2020 report by the Kaiser Family Foundation revealed that U.S. health insurers spent approximately 82 cents of every premium dollar on medical claims and healthcare quality improvements. The remaining 18 cents covered administrative costs and profit margins, highlighting the razor-thin nature of this balance. Missteps in this equation can lead to financial instability, as seen in 2017 when several insurers exited the Affordable Care Act marketplaces due to unsustainable claim costs.

To achieve this balance, insurers employ actuarial science to predict future claim costs based on historical data, demographic trends, and health risk factors. For example, a 45-year-old nonsmoker with no chronic conditions might pay a monthly premium of $400, while a 60-year-old with diabetes could pay $800 or more. These premiums are calibrated to offset the higher likelihood of medical claims in older or higher-risk populations. However, unpredictability in healthcare—such as a sudden outbreak of a new disease or a spike in chronic conditions—can disrupt these calculations, forcing insurers to adjust premiums or risk financial strain.

One practical strategy insurers use to manage claim costs is implementing utilization management programs. These programs include prior authorization for expensive procedures, step therapy for prescription drugs, and wellness initiatives to reduce long-term health risks. For instance, a patient prescribed a brand-name cholesterol medication might be required to try a generic version first, saving both the insurer and the patient money. Similarly, preventive care programs, such as annual check-ups or smoking cessation classes, can reduce the incidence of costly chronic diseases, lowering claim payouts over time.

Despite these measures, external factors often complicate the balance between premiums and claim costs. Government regulations, such as mandated coverage for pre-existing conditions or caps on out-of-pocket expenses, can increase claim liabilities without a corresponding rise in premiums. Economic downturns may also lead to reduced enrollment, shrinking the pool of premium revenue. Insurers must therefore remain agile, continuously reassessing their pricing models and cost-control strategies to maintain profitability.

Ultimately, the art of balancing premiums with medical claim costs is a dynamic process that requires foresight, adaptability, and a commitment to both financial sustainability and policyholder well-being. Insurers that master this balance not only secure their own profitability but also contribute to a more stable and accessible healthcare system. For consumers, understanding this delicate equilibrium can provide insight into why premiums fluctuate and how their own health choices impact the broader insurance landscape.

Get Medical Insurance for Your Year Abroad

You may want to see also

Explore related products

![]()

Administrative Costs: Overhead expenses impact profit margins significantly in health insurance operations

Health insurance companies, like any business, aim to generate profit, but their financial health is intricately tied to managing administrative costs. These overhead expenses, which include salaries, technology infrastructure, and regulatory compliance, can consume a significant portion of premium revenues. For instance, in the United States, administrative costs in the health insurance sector often account for 15-25% of total premiums collected, compared to single-digit percentages in countries with more streamlined systems. This disparity highlights the critical role administrative efficiency plays in determining profit margins.

Consider the operational complexity of processing claims, managing provider networks, and ensuring compliance with ever-evolving regulations. Each of these tasks requires substantial manpower and technological investment. For example, a mid-sized insurer might employ hundreds of claims processors, each earning an average salary of $50,000 annually, not including benefits. Add to this the cost of software licenses, which can run into millions of dollars per year, and the financial burden becomes clear. Reducing these costs, even marginally, can significantly boost profitability.

To mitigate administrative expenses, insurers often turn to automation and outsourcing. Robotic process automation (RPA), for instance, can handle repetitive tasks like data entry and claim verification with greater speed and accuracy than humans. A study by McKinsey found that insurers implementing RPA reduced processing times by up to 80%, freeing up resources for more strategic activities. Similarly, outsourcing customer service to countries with lower labor costs can cut expenses by 30-50%. However, these strategies come with risks, such as potential quality issues and data security concerns, which must be carefully managed.

Another critical factor is regulatory compliance, which varies widely by region. In the U.S., insurers must navigate the complexities of the Affordable Care Act, state-specific mandates, and HIPAA regulations, each requiring dedicated legal and compliance teams. These teams not only incur direct costs but also slow down decision-making processes. In contrast, countries with unified healthcare systems, like Canada, often have lower administrative costs due to simplified regulatory frameworks. Insurers operating in such environments can allocate more resources to core functions, enhancing profitability.

Ultimately, the ability of health insurers to earn profit hinges on their capacity to streamline administrative costs without compromising service quality. This requires a delicate balance between investment in technology, strategic outsourcing, and regulatory compliance. For policyholders, understanding these dynamics can provide insight into premium pricing and the value they receive. For insurers, mastering this balance is not just a financial imperative but a competitive necessity in an increasingly crowded market.

Understanding Medical Insurance Eligibility for Low-Income Earners

You may want to see also

Explore related products

![]()

Market Competition: Competitive pricing and market share influence profit potential in the industry

Health insurance companies operate in a highly competitive market where pricing strategies and market share are critical determinants of profitability. To understand this dynamic, consider how insurers balance the need to attract customers with affordable premiums while ensuring sufficient revenue to cover claims and operational costs. Competitive pricing is not merely about undercutting rivals; it involves a nuanced approach that factors in the cost of medical services, regulatory requirements, and consumer expectations. For instance, a company might offer lower premiums to gain market share but must offset this by managing claims efficiently or investing in preventive care programs to reduce long-term costs.

Analyzing market share reveals its direct impact on profit potential. Larger insurers often benefit from economies of scale, enabling them to negotiate better rates with healthcare providers and spread administrative costs across a broader customer base. For example, UnitedHealth Group, one of the largest U.S. insurers, leverages its size to offer competitive pricing while maintaining profitability. Conversely, smaller insurers may struggle to compete on price alone, forcing them to differentiate through specialized plans or superior customer service. This highlights the trade-off between aggressive pricing to gain market share and maintaining margins to sustain profitability.

A persuasive argument for competitive pricing lies in its ability to drive innovation and improve customer value. Insurers that strategically price their plans can reinvest profits into technology, such as telemedicine or health analytics tools, which enhance customer experience and reduce costs. For instance, a company might introduce a $20 monthly premium discount for policyholders who use wearable fitness trackers, encouraging healthier behaviors while lowering claims. Such initiatives not only attract price-sensitive consumers but also position the insurer as a forward-thinking player in the market.

Comparatively, the impact of market competition varies across regions and demographics. In highly saturated markets like urban areas, insurers often engage in price wars to capture a larger share, potentially squeezing profit margins. In contrast, rural or underserved areas may allow for higher premiums due to limited competition. Age categories also play a role; plans targeting younger, healthier individuals can be priced lower, while those for older populations must account for higher medical costs. Practical tips for insurers include segmenting markets to tailor pricing strategies and monitoring competitor moves to avoid being outpriced.

In conclusion, market competition in health insurance demands a strategic approach to pricing and market share. Insurers must balance aggressive pricing to attract customers with sustainable practices to ensure long-term profitability. By understanding the interplay between cost, value, and consumer behavior, companies can navigate this competitive landscape effectively, ultimately influencing their profit potential.

Choosing the Right GEICO Entity to Sue: A Legal Guide

You may want to see also

Explore related products

![]()

Regulatory Impact: Government policies and regulations can limit or enhance profit opportunities

Government policies and regulations act as a double-edged sword for health insurance profitability. On one side, they impose restrictions that squeeze margins. Mandated coverage of pre-existing conditions, for instance, forces insurers to accept high-risk individuals without charging actuarially fair premiums, leading to potential losses. Similarly, caps on administrative expenses limit insurers' ability to invest in cost-saving technologies or streamline operations, further squeezing profits. These regulations, while protecting consumers, create a challenging environment for insurers to maintain healthy bottom lines.

A contrasting perspective reveals how regulations can also foster profitability. Government-mandated minimum coverage requirements, for example, expand the pool of insured individuals, increasing the customer base for insurers. Additionally, regulations promoting preventive care can lead to healthier populations, reducing costly claims and improving insurer profitability in the long run. Think of it as a trade-off: regulations may limit short-term gains but can contribute to a more sustainable and profitable industry in the long term.

Consider the Affordable Care Act (ACA) in the United States. While it introduced regulations like guaranteed issue and community rating, it also established health insurance marketplaces, significantly expanding access to coverage. This influx of new customers, many subsidized by the government, provided a substantial revenue stream for insurers. The ACA also mandated essential health benefits, standardizing coverage and potentially reducing administrative complexities for insurers. This example illustrates how regulatory changes can create both challenges and opportunities for profit within the health insurance industry.

Navigating this regulatory landscape requires insurers to be agile and strategic. They must invest in data analytics to accurately price policies under mandated coverage requirements. Developing innovative wellness programs that align with preventive care mandates can also reduce claims and improve profitability. Furthermore, insurers can leverage technology to streamline operations and comply with administrative cost caps. Ultimately, success hinges on the ability to adapt to evolving regulations while identifying opportunities for growth within the framework they establish.

Vein Procedure Coverage: What Your Medical Insurance Offers

You may want to see also

Frequently asked questions

Yes, health insurance companies can earn profit, primarily through premiums collected from policyholders, investment income, and efficient management of healthcare costs.

Health insurance companies make a profit by setting premiums higher than the expected cost of claims, investing excess funds, and controlling healthcare expenditures through negotiated rates and utilization management.

While many health insurance companies are for-profit, there are also nonprofit insurers that focus on providing coverage without generating profit, reinvesting any surplus into improving services or lowering premiums.

![Profit [Region 2]](https://m.media-amazon.com/images/I/41ikusivibL._AC_UY218_.jpg)