Health insurers often reinsure to mitigate financial risks associated with high-cost claims or catastrophic events that could otherwise threaten their solvency. Reinsurance involves transferring a portion of their risk to another party, known as a reinsurer, in exchange for a premium. This practice allows health insurers to protect themselves against unpredictable and potentially devastating losses, ensuring they can continue to meet policyholder obligations. Reinsurance also enables insurers to expand their coverage offerings and manage their capital more efficiently by spreading risk across a broader pool. Common types of reinsurance in health insurance include quota share, where a fixed percentage of premiums and claims are shared, and excess of loss, which covers claims above a certain threshold. By reinsuring, health insurers can maintain financial stability, comply with regulatory requirements, and provide more reliable coverage to their customers.

| Characteristics | Values |

|---|---|

| Do health insurers reinsure? | Yes, many health insurers purchase reinsurance to protect themselves against large or unexpected claims. |

| Purpose of Reinsurance | To transfer financial risk, stabilize financial results, and ensure solvency in case of catastrophic or high-cost claims. |

| Types of Reinsurance | Treaty Reinsurance: Automatic coverage for predefined risks (e.g., stop-loss, quota share). Facultative Reinsurance: Coverage for specific, high-risk policies or claims. |

| Common Triggers | High-cost medical procedures, chronic illnesses, or rare conditions exceeding a predefined threshold. |

| Key Players | Ceding Insurers: Health insurers buying reinsurance. Reinsurers: Companies providing reinsurance (e.g., Munich Re, Swiss Re, SCOR). |

| Cost Structure | Premiums paid by ceding insurers based on risk assessment, claim history, and coverage limits. |

| Regulatory Considerations | Reinsurance contracts must comply with local and international regulations (e.g., Solvency II in Europe). |

| Market Trends | Increasing use of reinsurance due to rising healthcare costs, aging populations, and advancements in medical technology. |

| Examples | Stop-loss reinsurance for employer-sponsored health plans, reinsurance for high-risk individuals, or catastrophic coverage. |

| Impact on Premiums | Reinsurance costs may indirectly influence health insurance premiums, as insurers factor in reinsurance expenses. |

Explore related products

What You'll Learn

- Reinsurance Basics: Understanding how health insurers transfer risk to reinsurers for financial protection

- Types of Reinsurance: Proportional vs. non-proportional reinsurance in health insurance contracts

- Risk Management: Reinsurance as a tool to manage high-cost claims and stabilize finances

- Regulatory Impact: How government regulations influence health insurers' reinsurance decisions

- Cost Implications: The financial benefits and expenses of reinsurance for health insurers

![]()

Reinsurance Basics: Understanding how health insurers transfer risk to reinsurers for financial protection

Health insurers face significant financial risks due to unpredictable and potentially catastrophic claims. To mitigate these risks, they often transfer a portion of their exposure to reinsurers through reinsurance agreements. This practice allows primary insurers to protect their balance sheets, ensure solvency, and maintain stability in the face of large or frequent claims. For instance, a health insurer might reinsure high-cost claims exceeding $1 million, capping their liability and reducing the impact of outlier events.

Reinsurance contracts come in various forms, each tailored to the insurer’s risk appetite and portfolio characteristics. Quota share reinsurance involves the reinsurer taking a fixed percentage of all premiums and claims, providing steady risk sharing. In contrast, excess of loss reinsurance protects against claims above a specified threshold, making it ideal for managing extreme events. For example, a health insurer might purchase an excess of loss treaty with a $500,000 retention level, meaning the reinsurer covers any single claim exceeding this amount. This structure allows insurers to retain smaller, more predictable risks while offloading the tail-end exposure.

The reinsurance process begins with a detailed risk assessment, where the insurer evaluates its portfolio’s vulnerability to large claims. Factors such as policyholder demographics, coverage limits, and historical claims data play a critical role in determining the reinsurance need. Once a treaty is in place, the insurer pays a premium to the reinsurer, typically calculated as a percentage of the ceded risk. For instance, a reinsurer might charge 10% of the expected claims above the retention level. This cost is a strategic investment in financial stability, enabling insurers to underwrite policies with greater confidence.

One practical example of reinsurance in action is the coverage of specialty drugs, which can cost hundreds of thousands of dollars annually per patient. Without reinsurance, a single policyholder requiring such treatment could strain an insurer’s finances. By reinsuring these risks, the insurer limits its exposure while ensuring the policyholder receives necessary care. This arrangement highlights the dual benefit of reinsurance: protecting the insurer’s financial health while maintaining its ability to serve customers effectively.

However, reinsurance is not without challenges. Insurers must carefully negotiate terms to avoid overpaying for coverage or ceding too much risk. Additionally, reinsurers may impose exclusions or conditions that limit the insurer’s flexibility. For instance, a reinsurer might exclude pre-existing conditions or require higher retentions for high-risk groups. To navigate these complexities, insurers often work with brokers or consultants who specialize in structuring reinsurance programs. By doing so, they can achieve optimal risk transfer while balancing cost and coverage.

In conclusion, reinsurance is a critical tool for health insurers to manage financial risk and ensure long-term sustainability. By understanding the mechanics of reinsurance—from treaty types to risk assessment—insurers can design strategies that protect against unpredictable losses while maintaining competitive pricing. Whether through quota share or excess of loss arrangements, reinsurance provides a safety net that enables insurers to focus on their core mission: providing healthcare coverage to those who need it.

Mary Lou Retton's Health Insurance: What We Know So Far

You may want to see also

Explore related products

![]()

Types of Reinsurance: Proportional vs. non-proportional reinsurance in health insurance contracts

Health insurers frequently reinsure to mitigate financial risks associated with high-cost claims, ensuring stability and solvency. Reinsurance contracts in health insurance fall broadly into two categories: proportional and non-proportional. Each type serves distinct purposes, tailored to the insurer’s risk appetite and portfolio composition. Understanding these structures is critical for insurers to manage exposure effectively while maintaining profitability.

Proportional reinsurance operates on a shared-risk model, where the reinsurer assumes a predetermined percentage of both premiums and claims. For instance, in a 50% quota share agreement, the reinsurer receives half of the premiums and covers half of the claims. This arrangement provides predictable cost-sharing but limits the insurer’s profit potential, as gains are also divided. It’s particularly useful for insurers with volatile claim patterns, such as those covering high-risk populations like seniors or individuals with chronic conditions. For example, a health insurer managing a Medicare Advantage plan might use proportional reinsurance to cap losses from expensive treatments like chemotherapy or organ transplants.

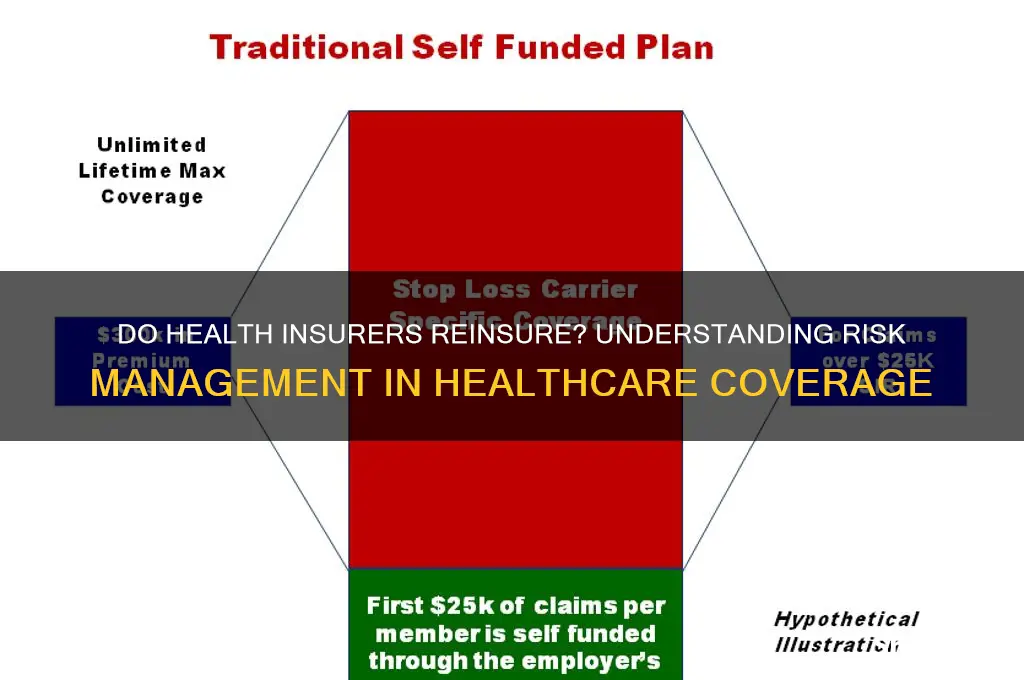

In contrast, non-proportional reinsurance triggers only when claims exceed a specified threshold, known as the retention or deductible. Excess of loss reinsurance, a common subtype, protects against catastrophic claims. For instance, an insurer might retain the first $1 million in claims per policyholder and reinsure anything above that. This structure allows insurers to retain more premium income while safeguarding against outlier events. It’s ideal for insurers with relatively stable claim patterns but exposure to high-severity risks, such as rare genetic disorders or emergency surgeries. A practical tip for insurers: align the retention level with historical claim data to avoid overpaying for coverage that rarely activates.

Choosing between proportional and non-proportional reinsurance depends on strategic priorities. Proportional reinsurance offers stability and simplicity, making it suitable for insurers seeking consistent risk reduction. Non-proportional reinsurance, however, provides flexibility and cost efficiency, appealing to those confident in their ability to manage routine claims but wary of black swan events. For instance, a regional insurer with a young, healthy policyholder base might opt for non-proportional reinsurance to minimize costs while protecting against unexpected pandemics or medical inflation.

A critical caution: reinsurance is not a one-size-fits-all solution. Insurers must assess their risk profile, regulatory environment, and financial goals before structuring contracts. Over-reliance on reinsurance can erode underwriting discipline, while underutilization exposes the insurer to unnecessary risk. Regular reviews of reinsurance treaties, especially in response to shifts in claim trends or market conditions, are essential. For example, an insurer experiencing a surge in mental health claims might renegotiate terms to include higher coverage limits for psychiatric treatments.

In conclusion, proportional and non-proportional reinsurance each offer unique advantages for health insurers navigating complex risk landscapes. By carefully selecting and tailoring these arrangements, insurers can achieve financial resilience while delivering reliable coverage to policyholders. The key lies in aligning reinsurance strategies with specific risk exposures and business objectives.

Medical Insurance Math: A Guide to Calculating Coverage

You may want to see also

Explore related products

![]()

Risk Management: Reinsurance as a tool to manage high-cost claims and stabilize finances

Health insurers frequently reinsure to mitigate the financial impact of high-cost claims, which can destabilize their balance sheets and threaten solvency. Reinsurance acts as a safety net, transferring a portion of the risk to another party in exchange for a premium. For instance, a health insurer might reinsure claims exceeding $1 million, ensuring that catastrophic events like complex surgeries or prolonged intensive care treatments don’t overwhelm their reserves. This practice is particularly critical in markets with high medical inflation or unpredictable claim patterns, such as oncology treatments, where costs can escalate rapidly due to expensive therapies like CAR-T cell therapy, which can cost upwards of $400,000 per treatment.

Analyzing the mechanics of reinsurance reveals its dual role: risk transfer and financial stabilization. Insurers typically choose between proportional reinsurance, where the reinsurer shares a fixed percentage of all claims, or non-proportional reinsurance, which covers claims only after a predetermined threshold is met. For health insurers, non-proportional reinsurance is often more appealing because it targets high-cost claims directly. For example, an insurer might set a retention level of $500,000, meaning any claim above this amount is reinsured. This structure allows insurers to retain control over smaller, more predictable claims while offloading the volatility of large payouts. However, the cost of reinsurance premiums must be carefully weighed against the potential savings, as over-reliance on reinsurance can erode profitability.

Persuasively, reinsurance is not just a financial tool but a strategic imperative for health insurers operating in volatile markets. Consider the case of a regional insurer facing a sudden outbreak of a rare disease requiring specialized, costly treatments. Without reinsurance, a cluster of such claims could deplete reserves and force premium hikes, alienating customers. Reinsurance provides a buffer, enabling insurers to maintain stable premiums while ensuring policyholders receive necessary care. Moreover, reinsurers often bring expertise in risk assessment and claims management, which can improve an insurer’s underwriting and operational efficiency. For instance, reinsurers may offer insights into emerging medical trends, such as the rise of gene therapies, helping insurers price policies more accurately.

Comparatively, reinsurance in health insurance differs from other sectors like property or casualty insurance due to the unique nature of medical risks. Health claims are often recurring and less predictable, with costs influenced by factors like patient adherence, treatment advancements, and regulatory changes. Unlike a hurricane or car accident, which are discrete events, a chronic condition like diabetes requires ongoing management, making risk modeling more complex. Health insurers must therefore tailor their reinsurance strategies to account for these dynamics, often using stop-loss reinsurance to cap their exposure to individual policyholders or specific conditions. This contrasts with industries where risks are more event-driven and reinsurance can be structured around discrete incidents.

Descriptively, implementing reinsurance requires a meticulous approach, starting with a thorough assessment of claim history and risk appetite. Insurers must analyze their portfolio to identify high-risk segments, such as policyholders with pre-existing conditions or those in high-claim geographic areas. Next, they negotiate terms with reinsurers, balancing coverage limits, premiums, and deductibles to align with their financial goals. For example, an insurer might opt for a $1 million stop-loss limit with a 20% coinsurance requirement, meaning they retain 20% of any claim exceeding the limit. Post-implementation, insurers must monitor performance, adjusting strategies as claim trends evolve. Practical tips include regularly reviewing reinsurance contracts to ensure they reflect current risk profiles and leveraging technology to streamline data sharing with reinsurers, enhancing transparency and efficiency.

In conclusion, reinsurance is a vital tool for health insurers to manage high-cost claims and stabilize finances, offering both risk transfer and strategic advantages. By carefully structuring reinsurance agreements and staying attuned to market dynamics, insurers can protect their financial health while ensuring policyholders receive uninterrupted care. Whether through stop-loss arrangements or collaborative risk management, reinsurance enables insurers to navigate the complexities of medical risks with greater confidence and resilience.

Medicaid and Private Insurance: Louisiana's Dual Coverage Option

You may want to see also

Explore related products

![]()

Regulatory Impact: How government regulations influence health insurers' reinsurance decisions

Health insurers frequently reinsure to mitigate financial risks associated with high-cost claims, particularly in volatile markets or when covering populations with unpredictable health outcomes. Government regulations play a pivotal role in shaping these reinsurance decisions, often dictating the terms under which insurers can transfer risk. For instance, the Affordable Care Act (ACA) in the United States introduced risk-sharing mechanisms like risk corridors, reinsurance, and risk adjustment programs, which directly influenced how insurers approached reinsurance. These programs were designed to stabilize premiums by redistributing risk among insurers, but their implementation and eventual phase-out demonstrated how regulatory changes can force insurers to recalibrate their reinsurance strategies.

Consider the European Union’s Solvency II directive, a regulatory framework that mandates insurers maintain sufficient capital to cover potential losses. This regulation incentivizes health insurers to reinsure as a means of reducing capital requirements, particularly for long-tail liabilities or catastrophic risks. However, the directive’s complexity and stringent reporting standards can also increase operational costs, prompting smaller insurers to rely more heavily on reinsurance to remain compliant. In contrast, countries with less prescriptive regulations may see insurers adopting more flexible reinsurance arrangements, tailored to their specific risk profiles rather than regulatory mandates.

A persuasive argument can be made that regulatory unpredictability is one of the most significant challenges insurers face when deciding whether to reinsure. For example, changes in government policies regarding coverage mandates or benefit requirements can alter the risk landscape overnight. Insurers operating in such environments often turn to reinsurance as a hedge against regulatory-induced volatility. However, if regulations are too restrictive—such as caps on reinsurance recoveries or limits on deductible amounts—insurers may opt for self-insurance or alternative risk-transfer mechanisms, potentially exposing themselves to greater financial risk.

To illustrate, in markets where governments impose price controls on premiums, insurers may struggle to recoup costs for high-risk policies. Reinsurance becomes a critical tool in these scenarios, allowing insurers to offload excess risk while maintaining compliance with pricing regulations. However, regulators must strike a balance: overly permissive reinsurance rules can lead to moral hazard, where insurers underprice policies knowing they can transfer risk, while overly restrictive rules can stifle market competition and innovation.

In conclusion, government regulations are not merely a backdrop to health insurers’ reinsurance decisions—they are a driving force. Insurers must navigate a complex web of mandates, incentives, and restrictions that shape their risk-management strategies. For policymakers, understanding this dynamic is crucial to crafting regulations that foster market stability without inadvertently discouraging reinsurance. For insurers, staying abreast of regulatory changes and adapting reinsurance strategies accordingly is essential to managing risk effectively in an ever-evolving landscape.

Health Insurance and Taxes: Do You Need to Show Proof?

You may want to see also

Explore related products

![]()

Cost Implications: The financial benefits and expenses of reinsurance for health insurers

Reinsurance serves as a financial safety net for health insurers, but its cost implications are a double-edged sword. On one hand, it mitigates the risk of catastrophic claims by transferring a portion of the liability to reinsurers. For instance, a health insurer might reinsure claims exceeding $1 million, capping their exposure and stabilizing cash flow. This risk transfer allows insurers to offer broader coverage without fear of insolvency, fostering market competitiveness. However, the premiums paid to reinsurers—often 10-20% of the ceded risk—directly reduce profit margins. Insurers must carefully weigh the cost of reinsurance against the potential losses it prevents.

The financial benefits of reinsurance extend beyond risk mitigation. By capping liability, insurers can adopt more aggressive pricing strategies, attracting price-sensitive consumers. For example, a health insurer might lower premiums for high-deductible plans, knowing that reinsurance will cover extreme claims. Additionally, reinsurance enhances financial predictability, enabling insurers to meet regulatory capital requirements and maintain credit ratings. A study by the Geneva Association found that reinsured insurers are 30% more likely to achieve consistent profitability over a five-year period compared to their non-reinsured counterparts. These advantages underscore reinsurance as a strategic tool for long-term financial health.

However, the expenses associated with reinsurance are not limited to premiums. Administrative costs, such as contract negotiation and claims processing, can add 2-5% to the total reinsurance expense. Moreover, reinsurers often impose deductibles or coinsurance clauses, leaving insurers responsible for a portion of large claims. For instance, a reinsurance treaty might require the insurer to cover the first $500,000 of a claim before reinsurance kicks in. Such structures demand meticulous underwriting and risk assessment to avoid unintended financial exposure. Insurers must also consider opportunity costs, as funds allocated to reinsurance premiums could otherwise be invested in growth initiatives or returned to shareholders.

A comparative analysis reveals that the cost-benefit ratio of reinsurance varies by insurer size and market position. Large insurers with diversified portfolios may find reinsurance less critical, as their scale allows for internal risk pooling. Conversely, smaller insurers or those operating in volatile markets often rely heavily on reinsurance to survive unpredictable claim patterns. For example, a regional insurer in a hurricane-prone area might allocate 15% of its premium revenue to reinsurance, while a national insurer might spend only 5%. This disparity highlights the need for tailored reinsurance strategies that align with an insurer’s risk appetite and market dynamics.

In conclusion, reinsurance offers health insurers a powerful mechanism to manage risk and stabilize finances, but its cost implications demand careful consideration. By balancing premiums, administrative expenses, and opportunity costs against the benefits of risk transfer and strategic flexibility, insurers can optimize their reinsurance strategies. Practical tips include negotiating deductible levels, exploring alternative reinsurance structures like quota share treaties, and regularly reviewing reinsurance needs in response to changing market conditions. Ultimately, reinsurance is not a one-size-fits-all solution but a dynamic tool that requires ongoing evaluation to maximize financial benefits while minimizing expenses.

Understanding Accident Insurance Reimbursement Calculations

You may want to see also

Frequently asked questions

Yes, many health insurers reinsure their policies to manage financial risk and protect themselves from large or unexpected claims.

Health insurers reinsure to transfer a portion of their risk to reinsurers, ensuring financial stability and reducing the impact of high-cost claims or catastrophic events.

Reinsurance for health insurers involves the insurer paying a premium to a reinsurer, who then agrees to cover a portion of the claims that exceed a predetermined threshold, as outlined in the reinsurance contract.