Medicare is a federal health insurance program for people aged 65 and over, as well as certain younger people with disabilities or specific health conditions. Medicare is split into several parts, including Part A (Hospital Insurance), Part B (Medical Insurance), Part C (Medicare Advantage), and Part D (Medicare drug coverage). Medicare Advantage is an alternative way to receive the benefits of Original Medicare (Part A and Part B) through private, Medicare-approved insurance companies. It's important to note that Medicare Supplement Insurance, or Medigap, is extra insurance that can be purchased from a private company to help cover out-of-pocket costs in Original Medicare. Individuals may have both Medicare and private health insurance, known as dual coverage, which can provide additional benefits but may also complicate benefits management.

| Characteristics | Values |

|---|---|

| Medicare | Federal health insurance for people aged 65 and older and certain younger people with disabilities |

| Administered by the federal government | |

| Benefits, premiums, and cost-sharing structures are decided at the federal level | |

| Generally the same for everyone of similar income | |

| No exclusions for pre-existing conditions | |

| Includes Part A, Part B, Part C, Part D, and Medigap | |

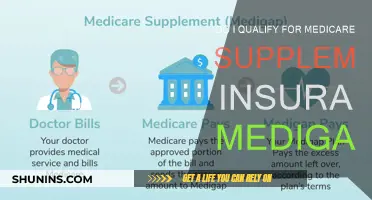

| Medigap policies help pay your share of costs in Original Medicare | |

| Medigap policies don't cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs | |

| Medicare Advantage is a Medicare-approved plan from a private company that offers an alternative to Original Medicare | |

| Medicare Advantage plans include prescription drug coverage and may have extra benefits like routine dental care | |

| Medicare Advantage plans set their premiums, deductibles, and coinsurance/copayment amounts | |

| Medicare Advantage plans have monthly premiums as low as $0 | |

| Non-Medicare Insurance | Offered by private companies |

| May not cover pre-existing conditions | |

| May have exclusions for specific conditions | |

| May have a waiting period before coverage for pre-existing conditions becomes effective | |

| May have higher monthly premiums for pre-existing conditions |

Explore related products

What You'll Learn

![]()

Medicare vs. Medicaid

Medicare and Medicaid are both government-run health insurance programs in the United States. However, they cater to two distinct groups of people. Medicare is primarily designed for individuals aged 65 and above and younger people with disabilities or end-stage renal disease. It is available to people at any income level. On the other hand, Medicaid is a joint federal and state program that provides health coverage for individuals and families with low incomes and resources. This includes children, pregnant women, people with disabilities, and seniors.

Medicare is the primary payer for medical needs, while Medicaid can cover costs that Medicare does not, such as nursing home care and personal care services. When visiting a provider that accepts both Medicare and Medicaid, Medicare pays first for the care, and Medicaid pays second, covering copays and other uncovered costs. If an individual qualifies for both Medicare and Medicaid, they are considered ""dually eligible"" and may be eligible for the Qualified Medicare Beneficiary (QMB) program, which assists with Part A and Part B premiums, coinsurance, and deductibles.

Eligibility for Medicaid varies by state, and individuals must meet their state's income and resource requirements. Some states allow individuals to ""spend down"" their income to qualify for Medicaid by paying non-covered medical expenses until their income is lowered to the qualifying level. Medicare eligibility generally begins three months before an individual turns 65 and ends three months after, and it is recommended to sign up as soon as eligible to avoid gaps in coverage and late enrollment penalties.

While Medicare is available to those aged 65 and above, regardless of income, individuals who are 65 or older and meet their state's income requirements for Medicaid can sign up for both programs. Together, they offer more comprehensive health coverage at a lower cost. It is important to note that Medicare and Medicaid have different parts, such as Part A (Hospital Insurance) and Part B (Medical Insurance), which may impact the specific coverage provided and the associated costs.

Best Medical Insurance for Unskilled Workers: Company Comparison

You may want to see also

Explore related products

![]()

Medicare and private insurance

Medicare is a federal health insurance program for anyone aged 65 and over, and some people under 65 with certain disabilities or conditions. It is public health insurance, which is government-funded. There are two main ways to get Medicare coverage: Original Medicare and Medicare Advantage. Original Medicare includes Part A and Part B, and you can join a separate Medicare drug plan (Part D) to get drug coverage. Medicare Advantage is a Medicare-approved plan from a private company that offers an alternative to Original Medicare for health and drug coverage. These plans include Part A, Part B, and usually Part D.

Private health insurance, on the other hand, is offered by private companies. Many people get private health insurance through a group plan provided by their employers. It is possible to have both Medicare and private insurance at the same time. This can happen if you have coverage through an employer, your spouse's employer, COBRA, or TRICARE. When you have both types of insurance, a process called "coordination of benefits" determines which insurance provider pays first. This provider is called the "primary payer" and they pay up to the limits of their coverage. The other provider is the "secondary payer" and they pay for costs that the primary payer doesn't cover, but they may not cover all of the remaining costs. The order of payment is important because if the secondary payer doesn't cover the remaining balance, you may be responsible for the rest of the costs.

If you have questions about which insurance pays first, you can contact the Benefits Coordination and Recovery Center at 1-855-798-2627 (TTY: 1-855-797-2627). You can also reach out to Medicare, the Social Security Administration (SSA), the State Health Insurance Assistance Program (SHIP), or the United States Department of Labor, depending on your specific questions and concerns.

Medicaid is another type of public health insurance that is a joint federal and state program. It provides health coverage for certain low-income people, families, children, pregnant women, the elderly, and people with disabilities. Medicaid offers benefits that Medicare doesn't normally cover, like nursing home care and personal care services. People with Medicaid usually don't pay anything for covered medical expenses but may owe a small co-payment for some items or services. It is possible to have both Medicare and Medicaid.

Maximizing Tax Benefits: Deducting Spousal Medical Insurance via Employers

You may want to see also

Explore related products

![]()

Medicare Part A and Part B

Medicare is federal health insurance for anyone aged 65 and older, as well as some people under 65 with certain disabilities or conditions. Medicare has different parts, and each part covers different services.

Medicare Part A, also known as hospital insurance, covers inpatient hospital care, skilled nursing facility care, hospice care, and home health care. Most people get Part A for free, but some have to pay a premium for this coverage. To be eligible for premium-free Part A, an individual must be entitled to receive Medicare based on their own earnings or those of a spouse, parent, or child. To receive premium-free Part A, the worker must have a specified number of quarters of coverage (QCs) and file an application for Social Security or Railroad Retirement Board (RRB) benefits. An individual receiving monthly Social Security or RRB benefits, at least four months before turning 65, will get Part A automatically at age 65. However, if an individual is not receiving these benefits, they must file an application for Medicare by contacting the Social Security Administration. Individuals who are eligible for premium-free Part A include those who receive regular dialysis treatments or a kidney transplant, have filed an application for Medicare, and meet certain conditions regarding their work history or eligibility for Social Security or RRB benefits.

Medicare Part B, also known as medical insurance, covers outpatient hospital care, doctor visits, preventive services, and durable medical equipment. Individuals must pay a premium for Part B coverage. The premium amount may vary depending on the individual's income. To enroll in Part B, individuals must contact the Social Security Administration. Similar to Part A, individuals who are not receiving monthly Social Security or RRB benefits must file an application for Medicare.

Once an individual has signed up for Part A and Part B, they can choose between Original Medicare and Medicare Advantage. Original Medicare includes Part A and Part B and allows individuals to use any doctor or hospital that accepts Medicare anywhere in the US. Medicare Advantage, also known as Part C, is a bundled plan offered by private companies that include Part A, Part B, and usually Part D, which covers prescription drug costs. Medicare Advantage plans may have different out-of-pocket costs and provider networks compared to Original Medicare.

Dual Medical Insurance: BCBS' Comprehensive Coverage Options

You may want to see also

Explore related products

![]()

Medicare Advantage

There are several types of Medicare Advantage Plans, including Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), Special Needs Plans (SNPs), Medicare Medical Savings Accounts (MSAs), and Private Fee-for-Service Plans (PFFS).

Before joining a Medicare Advantage Plan, it is important to talk to your employer, union, or benefits administrator about their rules. Joining a Medicare Advantage Plan might cause you to lose your employer or union coverage, and you may not be able to get this coverage back. Additionally, a Medicare Advantage Plan can disenroll you if you move outside the plan's service area, lose Medicare or Medicaid eligibility, join a drug plan (in some cases), or if the plan's contract with Medicare ends.

FEMA and Insurance: When to Apply for Both?

You may want to see also

Explore related products

![]()

Medicare drug plans

Medicare is federal health insurance for anyone aged 65 or older, as well as some people under 65 with certain disabilities or conditions. Once you've signed up for Part A and Part B of Medicare, you can choose between Original Medicare and Medicare Advantage. Original Medicare includes Part A and Part B, and you can join a separate Medicare drug plan (Part D) to get Medicare drug coverage. You can use any doctor or hospital that accepts Medicare anywhere in the US. You can also shop for and buy supplemental coverage (Medigap) that helps pay for your out-of-pocket costs, like your 20% coinsurance. However, you generally need Part A and Part B to buy a Medigap policy.

Medicare Advantage, on the other hand, is a Medicare-approved plan from a private company that offers an alternative to Original Medicare for your health and drug coverage. These "bundled" plans typically include Part A, Part B, and often Part D. They may also offer some extra benefits that Original Medicare doesn't. However, you may be restricted to only using doctors who are in the plan's network.

If you don't join a Medicare drug plan when you first get Medicare and go 63 days or more without creditable drug coverage, you may have to pay a Part D late enrollment penalty. This penalty increases the longer you wait to join a plan, and you'll usually have to pay it monthly for as long as you have Part D coverage, even if you switch plans.

Medicare drug coverage helps pay for prescription drugs, but it's important to note that Medigap policies generally do not cover prescription drugs.

Aflac and Medical Insurance: What's the Difference?

You may want to see also

Frequently asked questions

Medicare is a federal health insurance program for people aged 65 and older and some younger people with disabilities.

Medicaid is a joint federal and state program that provides health coverage for certain low-income people, families, and children. Medicaid offers benefits that Medicare doesn't normally cover, like nursing home care and personal care services.

The different parts of Medicare are Part A (Hospital Insurance), Part B (Medical Insurance), Part C (Medicare Advantage), Part D (Medicare drug coverage), and Medigap (supplemental coverage).

Yes, if you have Medicare and other health insurance, each type of coverage is called a "payer." The "primary payer" pays up to its coverage limit, then sends the remaining balance to the "secondary payer."

If you are aged 65 or older, or have certain disabilities, and have signed up for Part A and Part B of Medicare, then you have Medicare insurance. If you have not signed up for Medicare or do not meet the eligibility criteria, you likely have non-Medicare insurance.