If you are turning 65, you may be eligible for Medicare, but you may be wondering if you should keep your current insurance. This is a complex decision that depends on your specific circumstances, such as whether you are still working, the type of insurance you have, and the level of coverage you require. It is important to carefully consider your options and understand the potential consequences of enrolling in Medicare or retaining your current insurance plan.

| Characteristics | Values |

|---|---|

| Medicare eligibility | People aged 65 and older, younger people with disabilities, and people with End-Stage Renal Disease (ESRD) |

| Medicare parts | Part A (Hospital Insurance), Part B (Medical Insurance), Part D (Drug Coverage) |

| Medicare plans | Original Medicare, Medicare Advantage Plan (HMO or PPO), Medicare Supplement Insurance (Medigap) |

| Medicare costs | Monthly premiums, out-of-pocket costs (deductibles, co-pays, coinsurance), late enrollment penalties |

| Medicare and other insurance | Can have Medicare and other health insurance, coordination of benefits determines payment order |

| Switching to Medicare | Notify Marketplace plan, update Marketplace application, confirm plan for household members |

| Keeping current insurance | Possible with employer-sponsored insurance until retirement, delay Part B enrollment until retirement |

Explore related products

$19.95 $14.95

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UY218_.jpg)

What You'll Learn

![]()

Medicare and other health insurance

Medicare is a federal health insurance program for people aged 65 and over, as well as certain younger people with disabilities, and those with End-Stage Renal Disease. It is important to understand how Medicare works with other insurance, as you may have other health insurance alongside Medicare.

If you have Medicare and other health insurance, each type of coverage is called a "payer". The "primary payer" pays up to the limits of its coverage and then sends the rest of the balance to the "secondary payer". If the secondary payer doesn't cover the remaining balance, you may be responsible for the remaining costs. If you have group health insurance, your employer may offer coverage when you have Medicare, such as a supplemental plan, drug coverage, or a Medicare Advantage Plan.

You can keep your Marketplace plan if you have Medicare, but you will pay the full price for it, and your insurance company might end your Marketplace coverage. If you have to pay a premium for Medicare Part A, you can choose whether you want coverage through Medicare or the Marketplace. If you are receiving employer-sponsored health insurance through your or your spouse's job when you turn 65, you may be able to keep your insurance until you or your spouse retires. You will need to contact your employer's benefits representative to confirm this.

Medicare Supplement Insurance (Medigap) is extra insurance you can buy from a private company to help pay your share of costs in Original Medicare. Generally, you need Part A and Part B to buy a Medigap policy. Medigap policies do not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs.

Accent's Insurance Carrier

You may want to see also

Explore related products

![]()

Medicare and Marketplace coverage

Medicare is a federal health insurance program for people aged 65 and over, as well as certain younger people with disabilities, and those with End-Stage Renal Disease (ESRD). If you have Medicare, you don't need to do anything regarding the Health Insurance Marketplace as they are separate entities. The Marketplace won't affect your Medicare choices or benefits.

If you have employer-sponsored health insurance, you may be able to keep it when you turn 65. However, it is important to check with your employer's benefits representative to confirm. You should also consider enrolling in Medicare Part A as soon as you are eligible, as it is premium-free for most beneficiaries. If you have to pay a premium for Part A, you can choose to keep your Marketplace plan and drop Part A and Part B.

If you have Marketplace coverage and are eligible for Medicare, you should notify your Marketplace plan. Your Marketplace coverage will not be automatically cancelled when you enrol in Medicare, and you may have to repay some or all of the financial assistance you received for your Marketplace plan once your Medicare coverage begins.

If you have Medicare and other health insurance, each type of coverage is called a "payer". The "primary payer" pays up to the limits of its coverage and then sends the rest of the balance to the "secondary payer". If the secondary payer does not cover the remaining balance, you may be responsible for the remaining costs.

Car Insurance Costs: When Do They Drop for Women?

You may want to see also

Explore related products

![]()

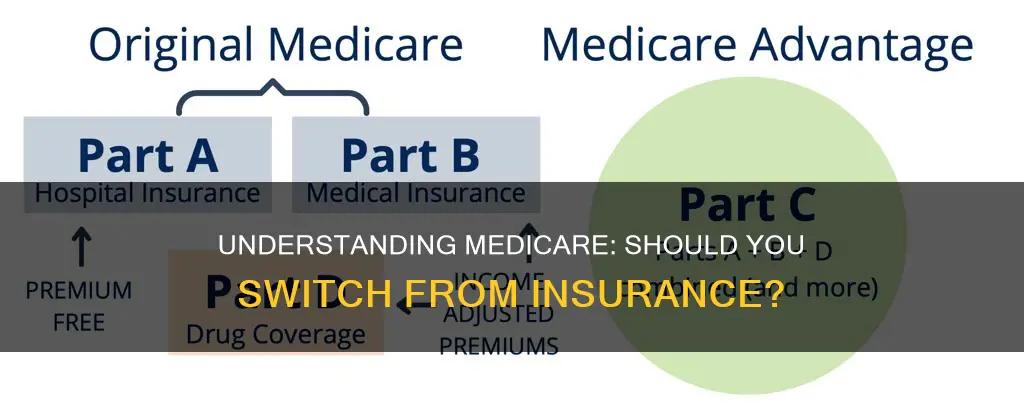

Medicare Part A and Part B

Medicare is federal health insurance for anyone aged 65 or older and some people under 65 with certain disabilities or conditions. Original Medicare includes Part A and Part B.

Medicare Part A (Hospital Insurance) covers inpatient care in hospitals, skilled nursing facility care, hospice care, and home health care. Most people get Part A for free, but some have to pay a premium for this coverage. To be eligible for premium-free Part A, an individual must be entitled to receive Medicare based on their own earnings or those of a spouse, parent, or child. To receive premium-free Part A, the worker must have a specified number of quarters of coverage (QCs) and file an application for Social Security or Railroad Retirement Board (RRB) benefits. If you have to pay a premium for Part A, you can choose whether you want to have coverage through Medicare or the Marketplace.

Medicare Part B (Medical Insurance) is typically paid for at a premium. To keep premium Part A, the person must also enrol in Part B and continue to pay all monthly premiums for both. Once you sign up for Part A and Part B, you can choose how you get your coverage. You can use any doctor or hospital that accepts Medicare anywhere in the U.S. You can also shop for and buy supplemental coverage that helps pay your out-of-pocket costs.

Medicare Advantage (Part C) is an alternative to Parts A and B that bundles several coverage types, including Parts A, B, and usually D (Medicare Drug Plan). Medicare Advantage Plans are offered by private insurance companies and may include additional benefits that Original Medicare doesn't.

Boat Insurance: Is It Mandatory?

You may want to see also

Explore related products

![]()

Medicare and prescription drug plans

Medicare is a federal health insurance program for people aged 65 and over, as well as certain younger people with disabilities, and those with End-Stage Renal Disease. If you have Medicare and other health insurance, each type of coverage is called a "payer". The "primary payer" pays up to the limit of its coverage and then sends the rest of the balance to the "secondary payer". If you have prescription drug coverage, it is important to ask if it is considered "creditable". If it is creditable, you can wait to join a Medicare drug plan or a Medicare Advantage Plan with drug coverage.

If you have to pay a premium for Medicare Part A, you can choose whether you want coverage through Medicare or another insurance provider. You can keep your Marketplace plan if you have Medicare, but you will pay the full price for it. Your insurance company might end your Marketplace coverage, and you will have to pay a monthly late enrollment penalty.

If you have retiree coverage, it is important to check before joining a new plan, as you may lose your retiree coverage. Your employer may offer coverage when you have Medicare, such as a supplemental plan, drug coverage, or a Medicare Advantage Plan.

If you have questions about Medicare Part A and Part B enrollment, you can visit SSA.gov or call Medicare at 1-800-MEDICARE (800-633-4227).

Insurance Coverage: Will I Lose My Benefits?

You may want to see also

Explore related products

![]()

Medicare and retiree coverage

Medicare is a federal health insurance program for people aged 65 and over, as well as certain younger people with disabilities, and those with End-Stage Renal Disease.

If you are still working past the age of 65, you may be able to keep your employer's health insurance and wait to sign up for Medicare without paying a late enrollment penalty. You can also keep your Marketplace plan if you have Medicare, but you will pay the full price for it.

Retiree health coverage is health insurance that some employers, unions, and trusts may offer to retiring employees and their spouses. It is typically group health insurance similar to plans offered to active employees. Even if you have a retiree health plan, you most likely need to sign up for Medicare. Depending on the plan, you may need to sign up for Part A and Part B, or just Part A.

If you have both Medicare and retiree coverage, Medicare generally pays first for your healthcare bills, and then your retiree plan covers the rest. However, retiree coverage may also pay for care or other items and services that Medicare does not cover, such as vision, dental, and prescription drugs.

If you have retiree coverage, it is important to check whether you will lose this coverage if you get Medicare. You may need to enroll in both Medicare Part A and Part B to get full benefits from your retiree coverage.

American Modern Insurance: Admitted Carrier Status

You may want to see also

Frequently asked questions

No, you can keep your insurance and delay signing up for Medicare. However, you may want to enrol in Part A as soon as you are eligible, as it is premium-free for most beneficiaries. If you have employer-sponsored insurance, you may be able to keep it until you retire.

Medicare coverage includes benefits like free preventive benefits, cancer screenings, an annual wellness visit, and more. There is also a $2,000 cap on what you pay out-of-pocket for Part D drugs.

Some private insurance companies reduce their payments or do not pay at all for services if you are eligible for other coverage, like Medicare. You may also face late enrollment penalties if you do not sign up for Medicare Part A or Part B when you are first eligible.

Yes, but you will pay full price for your insurance plan. You may also need to sign up for Medicare Part B for your insurance to pay the remaining balance after Medicare.

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71tm-tSiWnL._AC_UL320_.jpg)