If you have health insurance through your spouse's employer, you may not need to sign up for Medicare at 65. This depends on the size of the company your spouse works for and whether you have creditable coverage. If your spouse works for a large employer, defined as a company with 20 or more employees, you don't need to sign up for Medicare at 65. However, if your spouse works for an employer with fewer than 20 employees, Medicare typically becomes the primary coverage at 65, and you need to sign up to avoid gaps in coverage. Additionally, if your spouse is not working and is 65 or older, they can enroll in Medicare Part A for free, assuming you are 62 or older.

| Characteristics | Values |

|---|---|

| Medicare qualification | Eligible at 65 years of age, or younger with a qualifying disability or end-stage renal disease |

| Spouse qualification | Eligible at 65 years of age, or based on the working spouse's work record |

| Medicare and private insurance | If you have creditable coverage, you don't need to sign up for Medicare |

| Group Health Plan (GHP) | Company with 20 or more employees, insurance pays primary |

| Small Group Health Plan (SGHP) | Company with fewer than 20 employees, insurance pays secondary, enrol in Parts A, B and D |

| Medicare Parts | Part A is free, Part B and Part D have monthly premiums |

| Medicare and employer coverage | If covered by spouse's employer, you may not need to sign up for Medicare at 65, depending on the size of the employer |

| Delaying Medicare | You can delay Medicare if you have coverage from a current employer |

Explore related products

$43.71 $49

What You'll Learn

![]()

Medicare Parts A and B

Medicare is federal health insurance for anyone aged 65 and older, and some people under 65 with certain disabilities or conditions. Medicare Parts A and B, also known as Original Medicare, are available to individuals who are eligible for premium-free Part A based on their own earnings or those of a spouse, parent, or child.

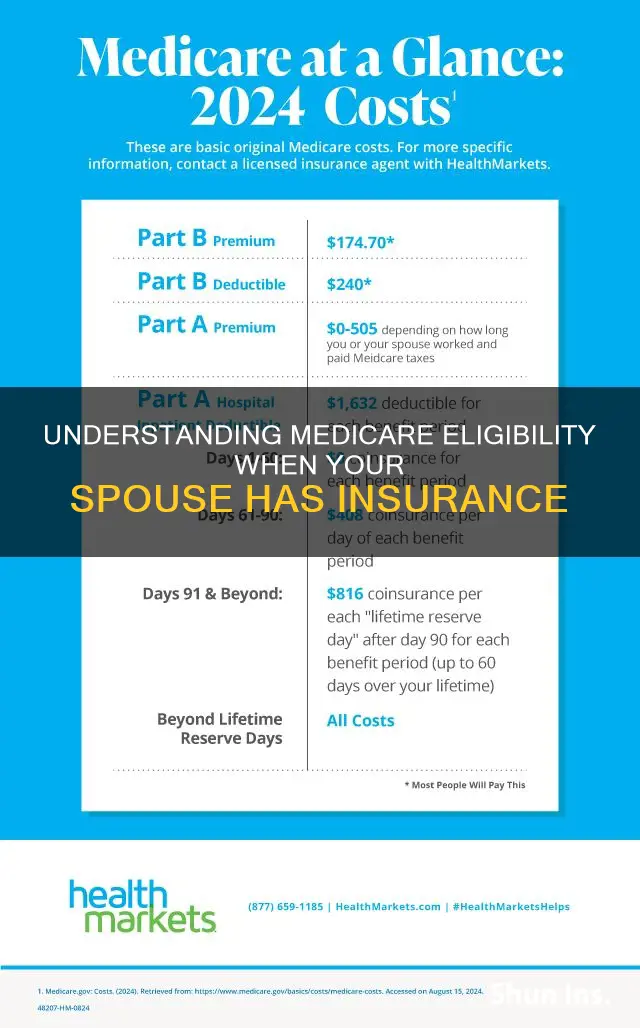

Medicare Part A is hospital insurance, and Part B is medical insurance. Part A is free for those with the qualifying number of Social Security credits, while Part B requires a monthly premium. Part A helps cover inpatient care in hospitals, skilled nursing facility care, hospice care, and home health care. Part B, on the other hand, requires a monthly premium and covers 20% of the cost of medical services such as doctor visits, outpatient care, and durable medical equipment.

If your spouse has insurance, you may still qualify for Medicare Parts A and B. If your spouse works for a company with at least 20 employees, their insurance is considered a Group Health Plan (GHP), and your insurance will pay primary. In this case, you don't need to sign up for Medicare Parts A and B, but you can choose to sign up for Part A to get more secondary coverage. However, if your spouse's company has fewer than 20 employees, it is considered a Small Group Health Plan (SGHP), and you need to sign up for Parts A, B, and likely D if you want Medicare to pay primary.

If your spouse is covered by an employer's plan and is about to turn 65, you have several options. You can choose to wait to enrol in Medicare until you lose your spouse's employer coverage, or you can enrol in Part A only and delay Part B and Part D. However, you need to ensure that you have creditable coverage to avoid paying late enrolment penalties. Once you lose your employer coverage, you have a special enrolment period of eight months to enrol in Medicare without penalty.

Contraception Coverage: What's Included in Your Medical Insurance?

You may want to see also

Explore related products

![]()

Medicare and private insurance

Medicare is individual insurance, so spouses cannot be on the same plan. However, if one spouse is eligible for Medicare, their working partner may still have health insurance coverage through their employer, and the other spouse may continue to be covered under that plan. If the older spouse intends to retire when they turn 65, the younger spouse has several options for health insurance coverage.

If your spouse works for a large employer, defined as a company with 20 or more employees, you don't need to sign up for Medicare at 65. The company-sponsored health insurance will be the primary payer of medical bills, and Medicare will be the secondary payer. Employers with 20 or more employees must offer the same health benefits to all employees and their spouses, regardless of age, and they cannot require employees or spouses to enroll in Medicare at 65.

If your spouse works for an employer with fewer than 20 employees, Medicare typically becomes the primary coverage at 65, and the employer coverage is secondary. In that case, you need to sign up for Medicare at 65 or else you may face gaps in coverage. If your spouse's insurance is not creditable, you should apply for Medicare Part A and Part B.

If you have health insurance through your spouse's employer, you may delay signing up for Medicare only if you are still working. Even if you are covered by your spouse's retiree health insurance, you need to enroll in Medicare no later than eight months after your spouse stops working or you may have to pay a lifetime late enrollment penalty.

If your spouse is older than you and not working when they turn 65, they may be eligible to receive Medicare benefits based on your work record, even if you are not retired or receiving Medicare coverage yourself. If your spouse is 65 and not working, they can enroll in Medicare Part A (with no premium) if you have reached 62 years of age. You can both enroll in Original Medicare Part B when you reach 65 without being penalized for late enrollment if your employer health insurance coverage is comparable to what Medicare recipients receive.

Horse Medical Insurance: Understanding the Cost and Coverage

You may want to see also

Explore related products

![]()

Medicare and age

Medicare is typically available to individuals aged 65 or older. People often sign up for Medicare Parts A (Hospital Insurance) and B (Medical Insurance) when they turn 65. This is the Initial Enrollment Period, which includes the three months before and after the individual's 65th birthday. Signing up during this period ensures there are no gaps in coverage or late enrollment penalties.

If an individual misses the Initial Enrollment Period, they will have to wait to sign up, resulting in a gap in coverage. They may also incur a monthly penalty for Part B, which increases the longer they wait. This penalty is payable for as long as the individual has Part B.

In some cases, it may be beneficial to delay enrollment in Medicare Part B. For instance, if an individual is covered by their spouse's employer-sponsored health insurance, they may choose to delay enrolling in Medicare until they lose this coverage or their spouse retires. This is because Medicare Part B requires a monthly premium, whereas Part A is typically free.

It is important to note that Medicare eligibility is based on an individual's qualifications, and spousal coverage is not included. However, a spouse can become eligible for their own Medicare plan when they turn 65, regardless of their work history.

Additionally, individuals under 65 may be eligible for Medicare due to a disability. In this case, they will need 40 credits to qualify for Social Security disability benefits.

Retiree Medical Insurance: Should You Cancel Your Coverage?

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Medicare and disability

If your spouse has insurance, you do not need to sign up for Medicare as long as you have what is called "creditable coverage". This means that the insurance provided by your spouse's employer is primary, and Medicare pays secondary, covering whatever the primary insurance does not. However, if your spouse works for a company with fewer than 20 employees, you should ask their HR representative if the insurance is creditable. If it is not, you should apply for Medicare Part A and Part B.

If you are under 65 and eligible for Medicare due to a disability, the number used to determine primary vs. secondary coverage jumps up to 100 employees.

People who meet all the criteria for Social Security Disability are generally automatically enrolled in Parts A and B of Medicare. People who meet the standards but do not qualify for Social Security benefits can purchase Medicare by paying a monthly Part A premium, in addition to the monthly Part B premium. Medicare coverage is the same for people who qualify based on disability as for those based on age.

If you are receiving Social Security disability benefits, you will get Medicare automatically after receiving disability benefits for 24 months. If you have ALS, you will get Medicare automatically as soon as you start receiving disability benefits.

Medicare beneficiaries with disabilities can keep their coverage for at least 7 years and 9 months as long as their disabling condition still meets the rules. This includes a nine-month trial work period. After this period, they can purchase Medicare Part A and Part B if they continue to have a disability.

Benefits for Medical Assistants: Paid Vacation, Sick Leave, and Insurance

You may want to see also

Explore related products

![]()

Medicare and employer insurance

Medicare is individual insurance, so spouses cannot be on the same plan together. If your spouse is eligible for Medicare, they can get their own plan. However, there are some options for non-working spouses.

If you are covered by your spouse's employer health insurance, you may not need to sign up for Medicare at 65. This depends on the size of the employer. If your spouse works for a large employer, defined as a company with 20 or more employees, you don't need to sign up for Medicare at 65. The company-sponsored health insurance will be the primary payer, and Medicare will be the secondary payer. Employers with 20 or more employees must offer the same health benefits to all employees and their spouses, regardless of age, and they cannot require employees or spouses to enroll in Medicare at 65.

However, if your spouse works for an employer with fewer than 20 employees, Medicare typically becomes the primary coverage at 65, and the employer coverage is secondary. In that case, you need to sign up for Medicare at 65 to avoid gaps in coverage. If your spouse's employer coverage is considered creditable, you do not need to sign up for a Part D Prescription Drug plan.

If your spouse is still working and you are becoming eligible for Medicare, you may want to enroll only in premium-free Medicare Part A until your spouse retires or their employer coverage ends. Part B can be added later without penalty during a Special Enrollment Period, as long as your spouse's employer provides creditable coverage. If you are covered by your spouse's employer health insurance and are turning 65, you can enroll in Medicare Parts A and B, Part D prescription drug coverage, or a Medicare Advantage (Part C) plan. Many people in this situation choose to wait to enroll until they lose their spouse's employer coverage or choose to only enroll in Part A, as it usually has no premium.

If you decide to delay enrolling in Medicare, you will have a Special Enrollment Period of eight months that begins when your spouse's employer coverage is lost or when they retire. If you have health insurance through your spouse's employer, you can delay signing up for Medicare only if you or your spouse is still working. If your spouse continues their employer's coverage through COBRA, you must enroll in Medicare during your initial enrollment period to avoid late enrollment penalties.

Insurance Coverage for Weight Loss Medication: What's Included?

You may want to see also

Frequently asked questions

If your husband works for a large employer (a company with 20 or more employees), you don't need to sign up for Medicare at 65. However, if your husband works for an employer with fewer than 20 employees, Medicare typically becomes the primary coverage at 65, and you need to sign up to avoid gaps in coverage.

You can delay signing up for Medicare if you have coverage from your spouse's current employer. However, you need to enroll in Medicare no later than eight months after your spouse stops working to avoid a lifetime late enrollment penalty.

If your husband's insurance is creditable, you don't need to sign up for Medicare. Your spouse's private insurance coverage is creditable if they work for a company with at least 20 employees. If the company has fewer than 20 employees, ask their HR representative if the insurance is creditable.

If your husband is covered by your employer health insurance, he may want to enroll only in premium-free Medicare Part A until you retire or your employer coverage ends. Part B can be added later without penalty during a Special Enrollment Period.

If your spouse is younger than 65 and receives disability benefits from Social Security for 24 months, they automatically become eligible for Medicare on the 25th month.