Insurance agents are typically paid through commissions, which are a percentage of the insurance premium. Commissions incentivize agents to provide excellent service and go above and beyond to find the best coverage for their clients. There are two main types of insurance agents: captive agents, who exclusively represent one insurance carrier and receive a salary from the insurance company, and independent agents, who are not tied to a single provider and have more flexibility. Both types of agents receive commissions, with independent agents typically earning higher commissions to compensate for their higher business expenses. Commission rates vary depending on the type of insurance, the agent's location, and the insurance provider, and agents may also receive bonuses or additional commissions based on performance metrics.

| Characteristics | Values |

|---|---|

| Do insurance agents make a commission? | Yes |

| Types of insurance agents | Captive, Independent |

| Captive agents' salary | Fixed wages, plus commission |

| Independent agents' salary | Straight commission, moderate annual salary |

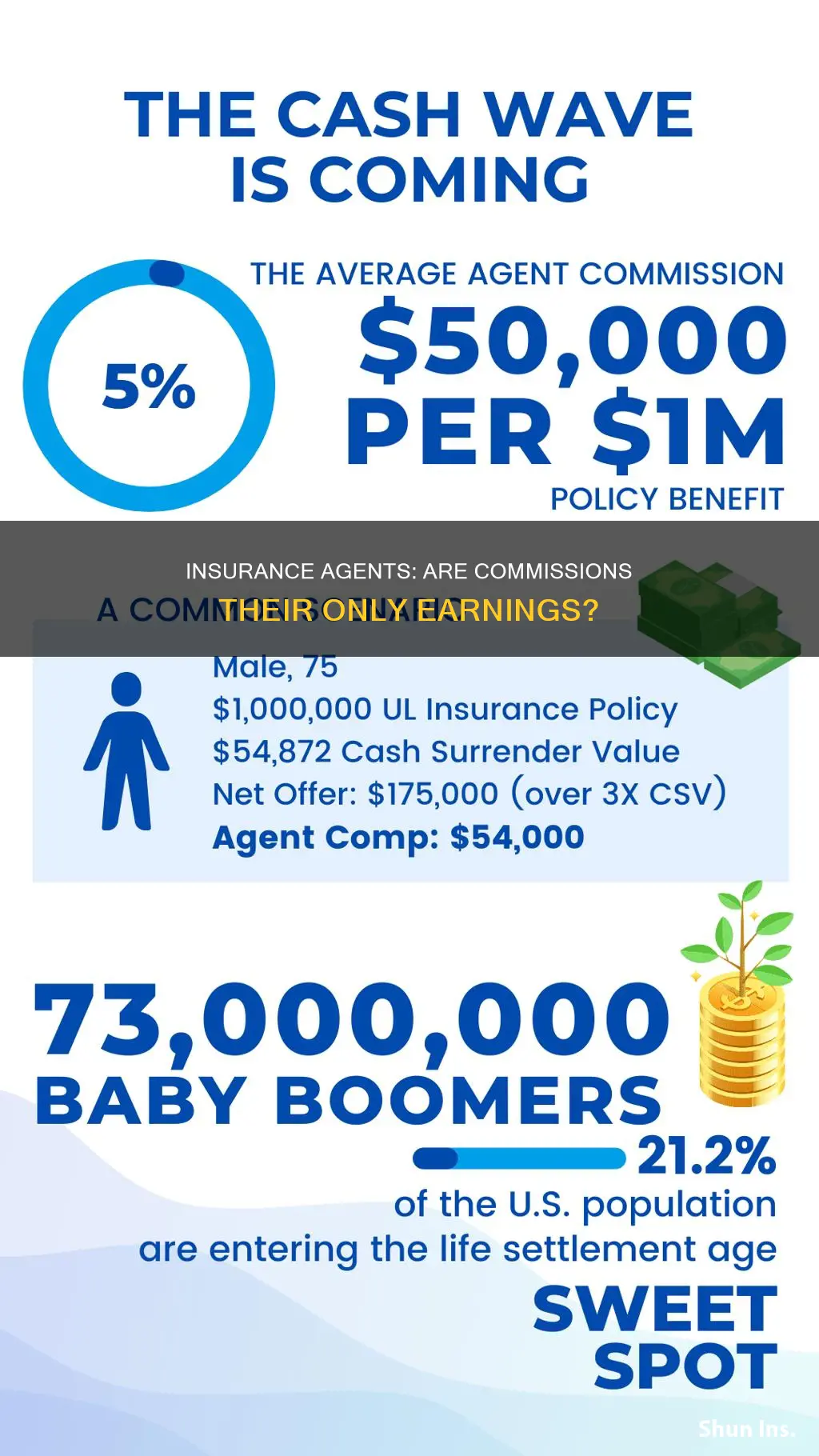

| Commission rates | 5%-20% (varies by state, carrier, policy, and agent) |

| Commission rates for auto and home policies | Captive agents: 5%-10%, Independent agents: 15% |

| Commission rates for health insurance agents | 5%-10% |

| Commission rates for group policies | 3%-6% |

| Commission rates for life insurance agents | 40%-120% of first-year premiums |

| Commission rates for renewals | 2%-15% |

| Contingent commissions | Yes, based on performance metrics |

| Bonuses | Yes, based on insurance company performance and "profitable years" |

Explore related products

What You'll Learn

![]()

Captive vs independent agents

Captive and independent insurance agents are two types of insurance agents in the United States, and their compensation structures differ. Captive agents are contracted to work with a single insurance company and are paid a salary, commission, or both by that company. They may also receive benefits and bonuses from their insurers. Independent agents, on the other hand, work with multiple insurance companies and are typically paid only through commissions on sales. They have access to a wider range of policies and can offer their clients more coverage options. However, they are responsible for paying their overhead costs and generating their leads.

Captive agents receive extensive support from their insurance company, including marketing materials, client referrals, and cost-sharing for buying leads. They also benefit from the company's broader marketing strategy and are often provided with a list of prospects. In return for this support, captive agents typically earn a lower commission than independent agents, sometimes as much as 50% less. Additionally, captive agents must meet sales quotas and may be pushed to sell certain policies, which may not always be the best fit for the client.

Independent insurance agents, by contrast, have the freedom to work with multiple insurance companies and sell policies from various providers. This allows them to offer their clients a wider selection of coverage options and find the most suitable policies for their clients' needs. Independent agents have more opportunities to cross-sell and mix-and-match policies, creating custom plans for their clients. However, they do not have access to the same level of support and referrals provided by insurance companies to their exclusive agents. Independent agents are responsible for generating their own leads and maintaining their independent business operations, which can result in higher overhead costs.

While captive agents have the security of a salary and benefits provided by their insurance company, independent agents have the potential to earn higher commissions per sale. Independent agents are solely focused on closing sales to earn their income, and their commission is their only source of income. They rarely receive bonuses or participate in cost-sharing programs, but the higher commission rates can make up for these differences. Ultimately, both career paths as captive or independent agents can be lucrative and have their own perks.

Understanding Your Mortgage Payment and Insurance Bundle

You may want to see also

Explore related products

![]()

Premium commissions

Captive insurance agents, who work for a single insurer, may be paid a salary or receive commissions on the premiums their clients pay. For auto and home policies, they typically earn 5% to 10% of the entire premiums paid in the first year, with renewal commissions ranging from 2% to 5%.

Independent insurance agents, who can sell policies for multiple carriers, often receive higher commissions than captive agents. For auto and home policies, they may earn about 15% of the first-year premiums and 2% to 15% for renewals. This incentive structure motivates independent agents to find the most suitable and valuable coverage for their clients.

Life insurance agents tend to receive larger upfront commissions, with rates ranging from 40% to 120% of the first-year premiums. The renewal commissions for life insurance policies are significantly lower, typically ranging from 1% to 2%.

It is important to note that insurance agents' commissions may vary based on the dollar amount of premiums they place with a company annually. Additionally, some insurance companies implement profit-sharing programs, rewarding agencies with a percentage of written or earned premiums as a bonus upon achieving specific revenue targets.

Who Are Insurance Solicitors and What Do They Do?

You may want to see also

Explore related products

![]()

Performance-based pay

Insurance agents are typically paid through commissions, with their performance-based pay depending on a range of factors. Firstly, the type of insurance agent impacts the structure of their pay. Captive agents exclusively represent a single insurance carrier, and they usually receive a salary from the insurance company. They may also receive a commission payment on the policies sold and earn bonuses tied to the performance of the insurance company. In contrast, independent insurance agents are not tied to a specific insurance provider, and although they also earn a salary, they are more reliant on driving business growth to maximise their insurance commissions.

The type of insurance policy also determines the commission structure. For instance, captive insurance agents selling auto and home policies earn about 5% to 10% of the entire premiums paid for the first year, while independent agents receive approximately 15%. Life insurance agents receive front-loaded commissions of 40% to 120% of the first year's premiums, but renewal rates drop to 1-2%. Health insurance agents' commission rates depend on their partner providers, with an average range of 5-10% of the total premiums in the first year. Agents selling group policies earn lower commissions of around 3-6%. Medicare Advantage and Part D plans offer flat-rate commissions per application, while Med Supp plans do not have a maximum broker commission, allowing agents to earn an average of $573 per policy.

The length of the client relationship also impacts an insurance agent's commission. Agents focusing on long-term relationships can benefit from residual commissions through home insurance renewals, leading to a more stable income over time. While this ties their financial success to client satisfaction, it also incentivises agents to navigate the insurance claims process effectively and provide excellent service.

Finally, insurance agents' performance-based pay can be influenced by certain performance metrics. Agents may receive contingent commissions based on meeting sales targets or maintaining low claim ratios. Additionally, some insurance companies implement profit-sharing programs, rewarding agencies with a percentage of premiums as a bonus once revenue targets are achieved.

Understanding H06 Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Salary and bonuses

The salary and bonuses of insurance agents vary depending on their type and contract. Captive agents exclusively represent a single insurance carrier and are typically salaried employees, earning a fixed wage from the insurance company. They may also receive commissions and bonuses based on their sales performance. On the other hand, independent insurance agents are not tied to a specific provider, giving them more flexibility in the products they offer. They usually rely primarily on commissions and may earn higher commissions than captive agents.

Captive insurance agents selling auto and home policies typically earn commissions of 5% to 10% of the total premiums in the first year, while independent agents may receive up to 15%. Life insurance agents receive the highest commissions in the industry, with front-loaded commissions ranging from 40% to 120% of the first year's premiums, although renewal rates are significantly lower at 1% to 2%. Health insurance agents' commissions vary, averaging between 5% and 10% of the policy's total premiums, with group policies earning slightly lower commissions of around 3% to 6%.

In addition to base commissions, some insurers offer supplemental and contingent commissions as incentives for agents to meet certain business targets. Contingent commissions are based on performance metrics such as sales targets or maintaining low claim ratios. Agents focusing on long-term client relationships may benefit from residual commissions, earning a steady income through policy renewals.

While most insurance agents receive at least some commission, the industry has been moving towards a straight commission structure. Some captive agents, such as those working for direct carriers, may receive a salary plus bonuses based on the number of accounts they sign up. These bonuses can be in the form of profit-sharing programs where agencies receive a percentage of premiums as a bonus once they achieve certain revenue targets.

Blue Benefit Private Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

$8.99

![]()

Commission rates

Captive Agents

Captive agents exclusively represent one insurance carrier and are effectively in-house advocates for that insurance company's products. They typically receive a salary from the insurance company, which provides a reliable income regardless of the policies sold. They may also receive a commission payment on the policies sold and earn bonuses tied to the performance of the insurance company. For auto and home policies, captive insurance agents earn about 5% to 10% of the entire premiums paid for the first year. Commission rates for renewals range between 2% and 15%, averaging around 2% to 5%.

Independent Agents

Independent insurance agents are not tied to an individual insurance provider, which means they have more freedom and flexibility in the carriers and products they represent. They usually work solely on commission, meaning their income is dependent on the number of policies they sell. Independent agents typically earn higher commissions than captive agents, with about 15% of the entire premiums paid for the first year for auto and home policies. Like captive agents, their commission rates for renewals are between 2% and 15%, but they have more variability in their commission rates overall.

Health Insurance Agents

Life Insurance Agents

Life insurance agents receive the highest commission rates in the industry, with front-loaded commissions of 40% to 120% of a policy's first-year premiums. However, the rates for renewals drop significantly to 1% to 2%, and some agents no longer receive commissions after the third year.

Bar Insurance: What Types Does Your Business Need?

You may want to see also

Frequently asked questions

Yes, insurance agents typically make money through commissions.

The amount of commission an insurance agent makes varies. It depends on the type of insurance, the agent's contract, and the state. For auto and home policies, captive insurance agents earn about 5% to 10% of the entire premiums paid for the first year, while independent agents receive about 15%.

No, insurance agents can also receive a salary from the insurance company. Captive agents, who exclusively represent one insurance carrier, typically receive a salary from the insurance company. Independent agents, on the other hand, are not tied to a single insurance provider and may or may not receive a salary.

Insurance agents will continue to earn a commission as long as the insurance policy remains active and the policyholder continues to pay their premiums. Agents can also earn a commission when a client renews their policy.

No, insurance agents do not lose money if clients make a claim. Their income is not directly impacted by claims. However, frequent or large claims can affect the overall risk profile of the insurance company, which might lead to premium adjustments for everyone in that risk pool.