Insurance companies do offer policies specifically designed to cover dogs, addressing various aspects of pet ownership. These policies, often referred to as pet insurance, typically provide financial protection against veterinary expenses, including accidents, illnesses, surgeries, and sometimes routine care. Additionally, some plans may cover liability claims if a dog causes property damage or injures someone. The availability and scope of coverage can vary widely depending on the insurer, the dog’s breed, age, and health history, as well as the owner’s location. While not all insurance companies offer pet insurance, many specialize in this niche, providing tailored plans to meet the needs of dog owners seeking peace of mind and financial security for their furry companions.

Explore related products

What You'll Learn

![]()

Pet Health Insurance Coverage

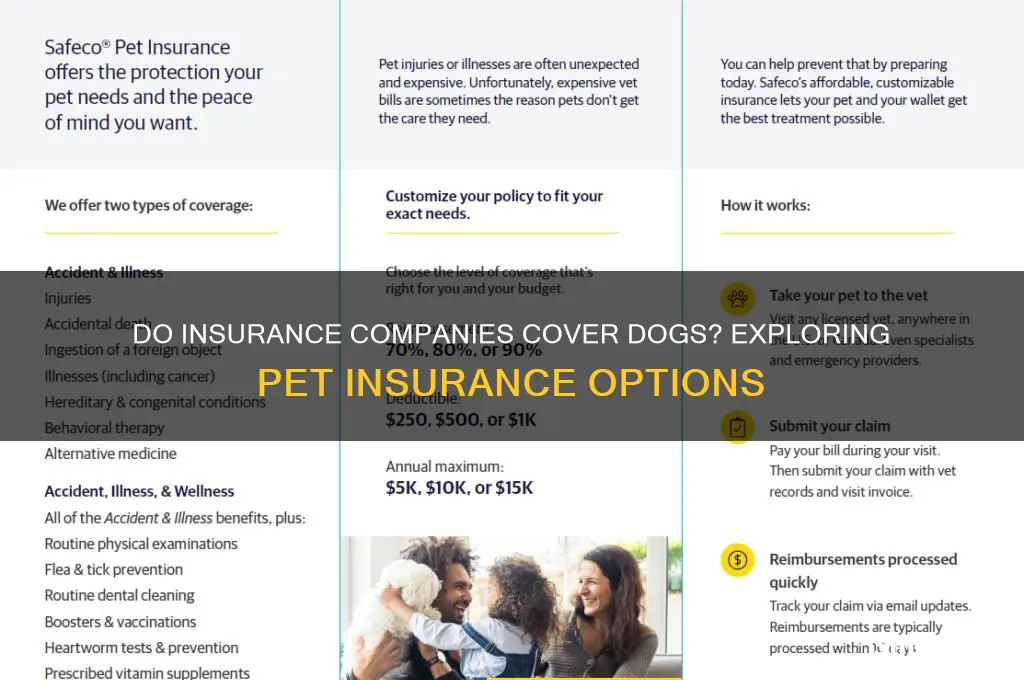

When considering pet health insurance coverage for your dog, it’s essential to understand the types of plans available. Basic plans typically cover accidents and emergencies, such as injuries from accidents or sudden illnesses. More comprehensive plans may include coverage for chronic conditions, hereditary diseases, and even preventive care like vaccinations, spaying/neutering, and dental cleanings. Some policies also offer add-ons for alternative therapies, such as acupuncture or physical therapy, which can be beneficial for dogs with specific health needs. The level of coverage you choose will depend on your dog’s breed, age, health history, and your budget.

Premiums for pet health insurance vary based on factors like your dog’s age, breed, location, and the extent of coverage selected. Younger, healthier dogs generally have lower premiums, while older dogs or breeds prone to specific health issues may face higher costs. Most policies operate on a reimbursement model, where you pay the vet bill upfront and then submit a claim to the insurance company for reimbursement, typically a percentage of the covered costs. Some providers also offer direct payment options to veterinarians, reducing out-of-pocket expenses. Understanding deductibles, annual limits, and co-pays is crucial to choosing a plan that aligns with your financial situation.

Exclusions and waiting periods are important aspects to consider when purchasing pet health insurance coverage. Pre-existing conditions—health issues your dog had before the policy started—are often excluded from coverage. Additionally, most policies have waiting periods (usually a few days for accidents and up to two weeks for illnesses) before coverage begins. Certain breeds may also face restrictions or higher premiums due to genetic predispositions to specific conditions. Reading the policy details carefully and asking questions about exclusions can help you avoid surprises when filing a claim.

Finally, pet health insurance coverage provides peace of mind by allowing you to focus on your dog’s well-being rather than the cost of care. It enables you to make decisions based on what’s best for your pet’s health, rather than being limited by financial constraints. With veterinary costs continuing to rise, investing in pet health insurance can be a wise decision, especially for dogs with a higher risk of health issues. By comparing plans, understanding coverage options, and selecting a policy that fits your needs, you can ensure your dog receives the care they deserve throughout their life.

Does Safeco Insurance Serve California? Coverage and Availability Explained

You may want to see also

Explore related products

![]()

Breed-Specific Insurance Policies

Insurance companies do offer policies that cover dogs, and among these, breed-specific insurance policies are a specialized option tailored to address the unique health risks, behaviors, and needs of particular dog breeds. These policies recognize that certain breeds are predisposed to specific genetic conditions, have higher energy levels, or face breed-related restrictions, which can impact insurance costs and coverage requirements. For example, breeds like German Shepherds, Bulldogs, or Golden Retrievers may have higher premiums due to their susceptibility to hip dysplasia, respiratory issues, or cancer, respectively. Breed-specific policies are designed to provide comprehensive coverage for these known risks, ensuring pet owners are not caught off guard by expensive veterinary bills.

When considering breed-specific insurance policies, it’s essential to understand that these plans often include coverage for hereditary and congenital conditions common to the breed. For instance, a policy for a Doberman Pinscher might emphasize coverage for cardiomyopathy, while a policy for a Pug may focus on respiratory and eye issues. Additionally, some breeds are classified as "high-risk" by insurers due to their size, strength, or historical use (e.g., guard dogs like Rottweilers or Pit Bulls), which can affect liability coverage. Breed-specific policies may include higher liability limits to protect owners against potential claims arising from breed-related incidents.

Another key aspect of breed-specific insurance policies is their consideration of the breed’s lifespan and associated healthcare costs. Smaller breeds like Chihuahuas or Shih Tzus generally live longer but may develop dental issues or joint problems as they age, while larger breeds like Great Danes or Saint Bernards have shorter lifespans and are prone to conditions like bloat or arthritis. These policies often adjust premiums and coverage based on the breed’s average lifespan and the expected veterinary expenses over time. Pet owners should carefully review the policy details to ensure it aligns with their dog’s specific needs.

For mixed-breed dogs, some insurers offer hybrid policies that combine elements of breed-specific coverage based on the dog’s dominant breeds. However, purebred dogs are the primary focus of breed-specific insurance policies. Owners of purebreds should research their dog’s breed history and common health issues to select a policy that offers adequate protection. It’s also advisable to compare multiple insurers, as coverage options and premiums can vary significantly depending on the company’s assessment of breed-related risks.

Finally, breed-specific insurance policies often include additional benefits tailored to the breed’s lifestyle. For example, policies for working breeds like Border Collies or Labrador Retrievers may offer coverage for training or rehabilitation costs related to their active roles. Similarly, policies for breeds prone to anxiety, such as Separation Anxiety in Labrador Retrievers, might include behavioral therapy coverage. By focusing on the unique traits and needs of specific breeds, these policies provide a more personalized and effective insurance solution for dog owners.

Life Insurance Rating: What You Need to Know

You may want to see also

Explore related products

![]()

Liability Insurance for Dogs

When considering liability insurance for dogs, it’s important to understand what factors influence eligibility and premiums. Insurance companies often assess the dog’s breed, age, size, and history of aggression. Breeds perceived as high-risk, such as Pit Bulls or Rottweilers, may face higher premiums or limited coverage options. Additionally, dogs with a history of biting or aggressive behavior may be excluded from policies altogether. Some insurers also require proof of obedience training or behavioral assessments to mitigate risks. It’s crucial to disclose all relevant information about your dog to ensure accurate coverage.

Most liability insurance for dogs is included as part of a broader homeowners or renters insurance policy, rather than being sold as a standalone product. However, if your dog is considered high-risk or your current policy excludes pet-related incidents, you may need to purchase a separate liability policy specifically for your dog. These standalone policies can be more expensive but provide comprehensive coverage tailored to your pet’s needs. Always review your policy details to understand what is covered, including limits on liability payouts and any exclusions.

To obtain liability insurance for your dog, start by contacting your current homeowners or renters insurance provider to inquire about adding pet liability coverage. If they don’t offer it, research specialized pet insurance companies that provide standalone liability policies. When comparing options, consider the coverage limits, deductibles, and premiums. It’s also wise to read customer reviews and check the insurer’s reputation for handling claims. Taking proactive steps, such as enrolling your dog in obedience training, can also improve your chances of securing affordable coverage.

Finally, liability insurance for dogs is not just a financial safeguard but also a responsible choice for pet owners. Dogs, regardless of breed or temperament, can act unpredictably in certain situations, and the consequences can be costly. By investing in liability insurance, you protect yourself from potential lawsuits and ensure that victims of dog-related incidents receive the compensation they need. This coverage promotes peace of mind and allows you to enjoy your pet’s companionship without the constant worry of unforeseen liabilities. Whether your dog is a small lapdog or a large breed, liability insurance is a valuable tool in managing the risks of pet ownership.

Colonial Penn Life Insurance: Is It Rated Well?

You may want to see also

Explore related products

![]()

Cost Factors in Dog Insurance

When considering dog insurance, understanding the cost factors is crucial for pet owners. The premium you pay for your dog’s insurance policy is influenced by several key elements. One of the primary factors is the breed of your dog. Certain breeds are predisposed to specific health conditions, which can significantly increase insurance costs. For example, large breeds like Great Danes or Bernese Mountain Dogs may face higher premiums due to their susceptibility to joint issues or heart conditions. Similarly, breeds like Bulldogs or Pugs, known for respiratory problems, often come with elevated insurance costs. Insurers assess these breed-specific risks to determine the likelihood of future claims.

Another critical cost factor is the age of your dog. Younger dogs generally have lower insurance premiums because they are less likely to have pre-existing conditions or chronic illnesses. As dogs age, the risk of health issues increases, leading to higher insurance costs. Some insurers may even have age limits for enrolling dogs in new policies, making it more expensive or difficult to insure older dogs. Additionally, the size and weight of your dog can impact costs, as larger dogs often require more expensive treatments and medications.

The location where you live also plays a significant role in determining dog insurance costs. Veterinary care costs vary widely by region, with urban areas typically having higher fees than rural areas. Insurers factor in these regional differences when calculating premiums. For instance, living in a city with a high cost of living may result in higher insurance rates compared to a rural town with lower veterinary expenses. Furthermore, areas with a higher prevalence of certain diseases or parasites may also influence pricing.

The type of coverage you choose is another major cost factor. Basic policies often cover accidents and emergencies, while comprehensive plans include routine care, vaccinations, and chronic condition management. Naturally, more extensive coverage comes with higher premiums. Additionally, the deductible and reimbursement level you select will affect costs. A lower deductible means higher monthly premiums, while a higher deductible reduces monthly costs but increases out-of-pocket expenses when filing a claim. Reimbursement rates, typically ranging from 70% to 90% of covered costs, also impact premiums, with higher reimbursement rates leading to higher premiums.

Lastly, your dog’s medical history and pre-existing conditions are critical in determining insurance costs. Dogs with a history of illnesses or chronic conditions may face higher premiums or exclusions for those specific conditions. Some insurers may even deny coverage for dogs with significant pre-existing issues. It’s essential to disclose your dog’s full medical history accurately, as failing to do so could result in denied claims or policy cancellation. Understanding these cost factors allows pet owners to make informed decisions when selecting a dog insurance policy that balances coverage and affordability.

Running Red Lights: Impact on Insurance Rates and Penalties

You may want to see also

Explore related products

![]()

Pre-Existing Conditions Exclusions

When considering pet insurance for dogs, one of the most critical aspects to understand is the Pre-Existing Conditions Exclusions. These exclusions are a standard feature in most pet insurance policies and can significantly impact the coverage your dog receives. A pre-existing condition is any injury, illness, or symptom that occurred or showed signs before the policy’s effective date or during a waiting period. Insurance companies exclude these conditions to manage risk and keep premiums affordable for policyholders. It’s essential to review your dog’s medical history carefully before purchasing a policy, as pre-existing conditions will not be covered, even if they resurface later.

Most pet insurance providers define pre-existing conditions broadly to avoid ambiguity. This includes not only diagnosed conditions but also any symptoms or abnormalities noted in your dog’s medical records or observed by a veterinarian. For example, if your dog had a limp before the policy started, even if it was never formally diagnosed, it would likely be considered pre-existing. Some insurers may also exclude conditions that are "bilaterally symmetrical," meaning if a condition affects one side of the body (e.g., a left knee injury), the same condition on the other side (e.g., a right knee injury) may also be excluded, even if it develops later.

It’s important to note that not all pre-existing conditions are permanent exclusions. Some insurers differentiate between curable and incurable pre-existing conditions. Curable conditions, such as a one-time ear infection that has been fully resolved and has no recurrence for a specified period (e.g., 6–12 months), may become eligible for coverage again. However, chronic or lifelong conditions, such as diabetes, allergies, or hip dysplasia, are typically excluded permanently. Always check the policy’s terms to understand how pre-existing conditions are handled.

To avoid surprises, be transparent about your dog’s health history when applying for insurance. Failing to disclose pre-existing conditions could result in denied claims or even policy cancellation. If your dog has a pre-existing condition, consider whether the policy still offers enough value for other potential issues. Some pet owners opt for accident-only plans, which exclude illnesses but cover injuries unrelated to pre-existing conditions. Additionally, some insurers offer "diminishing exclusions" for curable conditions, where coverage for a previously excluded condition may be reinstated after a period of good health.

Finally, if you’re adopting a dog or insuring a puppy, start the policy as early as possible to minimize the risk of pre-existing conditions. Puppies are less likely to have health issues, and early coverage ensures that any conditions developing later in life will be eligible for treatment. Always compare policies from multiple providers, as some may have more lenient definitions or better options for managing pre-existing conditions. Understanding these exclusions upfront will help you choose a policy that provides the best possible care for your dog while avoiding unexpected out-of-pocket expenses.

Utility Trailer Insurance: Is Coverage Required for Your Hauling Needs?

You may want to see also

Frequently asked questions

Yes, many insurance companies offer pet insurance policies that cover dogs, providing financial protection for veterinary care, accidents, and illnesses.

Dog insurance typically covers veterinary visits, surgeries, medications, emergency care, and sometimes preventive treatments like vaccinations or spaying/neutering, depending on the policy.

The cost of dog insurance varies based on factors like the dog’s breed, age, location, and the level of coverage chosen, but it generally ranges from $20 to $60 per month.

Dog insurance can be particularly beneficial for breeds prone to hereditary conditions or health issues, but it’s worth considering for any dog to avoid unexpected veterinary expenses.