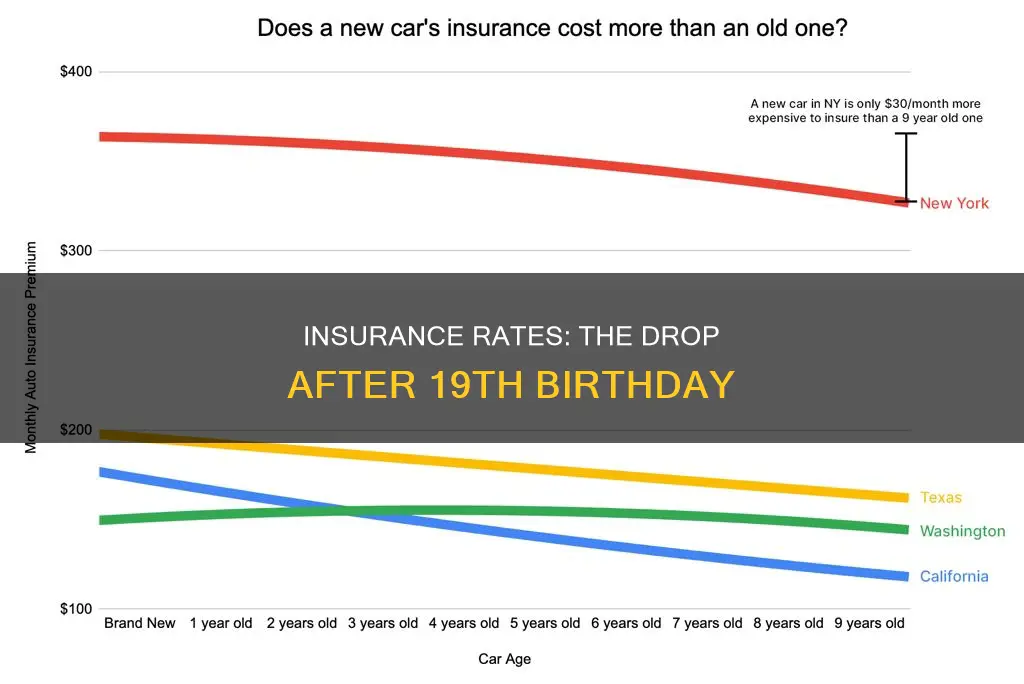

Car insurance rates are influenced by several factors, including age, driving history, location, vehicle type, and credit score. While rates may increase due to certain factors, they typically decrease as drivers gain experience and insurers perceive them as lower risk. Age is a significant factor, and younger drivers, especially those under 25, are considered high-risk due to their lack of experience. As a result, insurance rates tend to decrease at age 25, but this is not a guarantee, and a clean driving record is crucial for significant rate reductions. The most substantial rate drops occur before 25, with notable decreases at ages 19 and 21, as insurers recognize the increased experience and lower risk associated with these ages.

| Characteristics | Values |

|---|---|

| Average decrease in rates | $1,595 |

| Biggest decrease | Between 18 and 19 |

| Decrease in premiums | 25% |

| Second biggest decrease | At 21 (20% decrease) |

| Average decrease in rates between 16 and 25 | $4,400 annually or $368 monthly |

| Average decrease in rates at 25 | 7% |

| Average decrease in rates at Progressive | 8% |

| Average decrease in rates at 30 | 10-12% |

| Average increase in rates | 65-75 |

| Factors that influence rates | Driving history, location, vehicle type, credit score, insurance history, gender |

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

What You'll Learn

- Insurance rates are highest for teens, especially 16- and 17-year-olds

- Rates decrease as drivers gain experience, with major drops at 19, 21 and 25

- Young drivers are considered high-risk due to inexperience and unsafe behaviours

- Men pay more than women, especially at younger ages, due to higher accident rates

- Insurance rates can be lowered by improving credit scores, driving records and taking courses

![]()

Insurance rates are highest for teens, especially 16- and 17-year-olds

The cost of insurance typically decreases as drivers gain experience, with major drops around the ages of 19, 21, and 25. The biggest drop is usually from 18 to 19, when the average rate decreases by around $1,595. Insurance companies see drivers aged 19 as having more experience and being lower-risk.

While rates can go up for certain reasons, they usually go down as drivers hit key milestones or show they are low-risk. For example, drivers with a college education are seen as lower-risk by insurance companies, as they file fewer claims. Similarly, married drivers typically pay less than single or widowed drivers as they are seen as more financially stable and cautious.

Location is another factor that influences insurance rates. If you live in a city, you will likely pay more because urban areas tend to have more traffic, accidents, and car theft. In contrast, living in a rural area could mean lower premiums since there is less risk on the road.

The type of car you drive also matters. Cars with strong safety ratings, lower repair costs, or advanced safety features usually cost less to insure. On the other hand, sports or luxury cars can increase your insurance rates because they are more expensive to repair and may be more attractive to thieves.

Auto Insurance Duration: Progressive's Policy Lifespan Explained

You may want to see also

Explore related products

![]()

Rates decrease as drivers gain experience, with major drops at 19, 21 and 25

Car insurance rates are influenced by several factors, including age, driving history, location, vehicle type, credit score, and insurance history. While rates can increase for various reasons, they usually decrease as drivers reach certain milestones or demonstrate low-risk behaviour. Age is one of the most significant factors in determining car insurance rates, with younger drivers generally facing higher premiums due to their higher risk of accidents and unsafe driving behaviours.

Insurance companies classify young and inexperienced drivers as high-risk, and rates start to drop as drivers gain more experience and move away from this category. The transition from teenage years to early twenties brings about significant changes in driving behaviour and risk assessment, leading to notable drops in insurance rates at ages 19 and 21. At 19, drivers have often gained a few years of experience since obtaining their license, and insurers perceive them as less likely to engage in unsafe driving practices. This reduction in risk results in a substantial decrease in insurance premiums, with rates potentially dropping by 25%.

As drivers approach their 21st birthday, insurance rates take another significant dip, albeit slightly less pronounced than the decrease at age 19. Maintaining a clean driving record becomes increasingly important during these years, as accidents, speeding tickets, or violations can drive up insurance costs. By age 21, many drivers have accumulated sufficient experience to be considered lower-risk, resulting in a potential 20% decrease in insurance premiums.

While age 25 is often touted as a milestone for substantial insurance rate reductions, the reality is more gradual. Insurance companies view drivers aged 16 to 24 as high-risk, so rates gradually decrease throughout the early twenties as individuals gain experience and move out of this risk category. By age 25, drivers have typically graduated from the highest-risk group, and their premiums continue to decrease gradually through their late twenties and thirties. It is worth noting that a clean driving record is crucial for achieving significant rate reductions at this age, as accidents or violations can negate the expected discount.

In conclusion, while insurance rates do not solely depend on age, it is evident that rates decrease as drivers gain experience, with notable drops at ages 19, 21, and 25. These milestones signify transitions in driving behaviour and risk assessment, leading to lower premiums as insurers adjust their risk calculations. Maintaining a clean driving record, improving credit scores, and comparing insurance quotes can further enhance the cost savings associated with these age-related rate reductions.

Auto Insurance: Coverage for Canadians and American Visitors?

You may want to see also

Explore related products

![]()

Young drivers are considered high-risk due to inexperience and unsafe behaviours

Young drivers are considered high-risk due to a combination of inexperience and unsafe behaviours. Inexperience means young drivers are slower to react to hazards and are less able to spot them. Research has shown that young drivers who are overconfident in their self-assessment of their skills are more likely to crash in their first two years of driving than those who are insecure about their driving skills. This overconfidence can lead to dangerous driving behaviours, such as dangerous overtaking or speeding.

Young drivers are also more likely to engage in risky behaviours when travelling with multiple passengers. The presence of teenage peers increases the likelihood of risky behaviour, with the risk of a fatal crash increasing in direct relation to the number of teenagers in the car. This is due to peer pressure, which can encourage bad driving and lead to drivers 'showing off'. Newly qualified drivers with a car full of teenage passengers are four times more likely to be in a fatal crash compared to when driving alone.

In addition, young drivers are more likely to own their cars and take risks, such as speeding, especially at night. They are also more susceptible to distractions, with one in three teens admitting to texting while driving, which increases the risk of a crash by 23 times. Drinking and driving is another risk factor, with teenage drivers and young adults more likely to drink and drive, causing a disproportionate number of fatal crashes.

While age is a significant factor in insurance rates, other factors also come into play. Insurance companies consider drivers with a history of at-fault accidents, speeding tickets, and other violations to be high-risk, leading to higher premiums. Credit scores also impact insurance rates, with people who have bad credit seen as more likely to file claims, resulting in higher premiums. Location is another factor, with customers in areas of high theft or vandalism paying more for insurance.

Understanding Auto Insurance: Coverage Start Time

You may want to see also

Explore related products

![]()

Men pay more than women, especially at younger ages, due to higher accident rates

Insurance companies consider drivers aged 16 to 24 high-risk, and rates decrease as drivers gain experience. The biggest price cuts happen in the late teens and early 20s, especially between the ages of 18 and 19. By 25, rates tend to take one of their last noticeable dips before levelling out, assuming the driver has maintained a clean record.

Men pay more than women for car insurance, especially at younger ages. This is due to statistical data that indicates they pose a higher risk on the road, particularly in the younger age groups. Male drivers are more likely to engage in dangerous driving behaviours, such as speeding, drunk driving, and reckless driving. According to the Insurance Institute for Highway Safety (IIHS), male drivers were involved in a significantly higher number of passenger vehicle deaths compared to female drivers in 2021. There were 14,498 male passenger vehicle deaths in 2021, while there were 5,735 female passenger vehicle deaths. Men also tend to drive more miles every year than women, increasing their likelihood of being involved in an accident.

The Federal Highway Administration reports that men drive 16,550 miles per year while women drive around 10,142 miles annually. This means women drive 30% fewer miles each year than men, making them less exposed to the risk of accidents. Men also hold the majority of DUIs, with younger men, in particular, having a reputation for drinking and driving. A study by the University of Michigan found that while women cause slightly more accidents per capita than men, men were responsible for more fatal crashes.

While age is a significant factor in determining insurance rates, other aspects are also important to providers. New drivers pay more, regardless of age. Tickets, accidents, and DUIs make a driver high-risk, leading to higher premiums. The more violations on a driver's record, the more they will pay.

KBB or NADA: Which Guide Do Auto Insurance Companies Favor?

You may want to see also

Explore related products

![]()

Insurance rates can be lowered by improving credit scores, driving records and taking courses

While car insurance rates decrease as drivers gain experience, with significant drops around ages 19, 21, and 25, there are other factors that contribute to the cost of insurance. Insurance rates can be lowered by improving credit scores, improving driving records, and taking specific courses.

Firstly, insurance providers offer lower rates to drivers with good credit scores as it reflects how well they manage their finances. While improving one's credit may take time, it comes with long-term advantages. It is recommended to check one's credit report regularly for any changes or errors.

Secondly, maintaining a good driving record is crucial in keeping insurance rates low. Accidents, tickets, DUIs, and moving violations can all contribute to higher premiums as they indicate a higher-risk driver. By avoiding these incidents and being mindful of one's driving behaviour, individuals can maintain lower insurance rates.

Additionally, taking specific courses can help lower insurance costs. Defensive driving courses or driver's education courses are often seen as favourable by insurance companies, resulting in reduced rates. These courses demonstrate a commitment to safe driving and can lead to significant savings.

Furthermore, insurance rates can be lowered by taking advantage of various discounts offered by insurance providers. These include discounts for having multiple cars under one policy, being a long-time customer, having a higher deductible, or bundling home and auto insurance. Comparing quotes from different insurance companies and shopping around can also help identify opportunities to lower insurance rates.

By focusing on improving credit scores, maintaining a clean driving record, taking relevant courses, and exploring available discounts, individuals can effectively lower their insurance rates and manage their financial obligations more efficiently.

Driving Without Insurance: Is It a Risky Move?

You may want to see also

Frequently asked questions

Yes, insurance rates drop at 19, with the average rate decreasing by around $1,595. The biggest drop is typically from 18 to 19, with a 25% decrease in premiums.

Insurance rates are influenced by several factors, including driving history, location, vehicle type, credit score, and insurance history. Maintaining a clean driving record, improving your credit score, and comparing insurance quotes can help lower your insurance costs.

Yes, insurance rates typically continue to decrease gradually through the early twenties and stabilize around age 30 to 34. The most significant drops after 19 occur at ages 21 and 25, with rates increasing again around 65 to 75 years old.