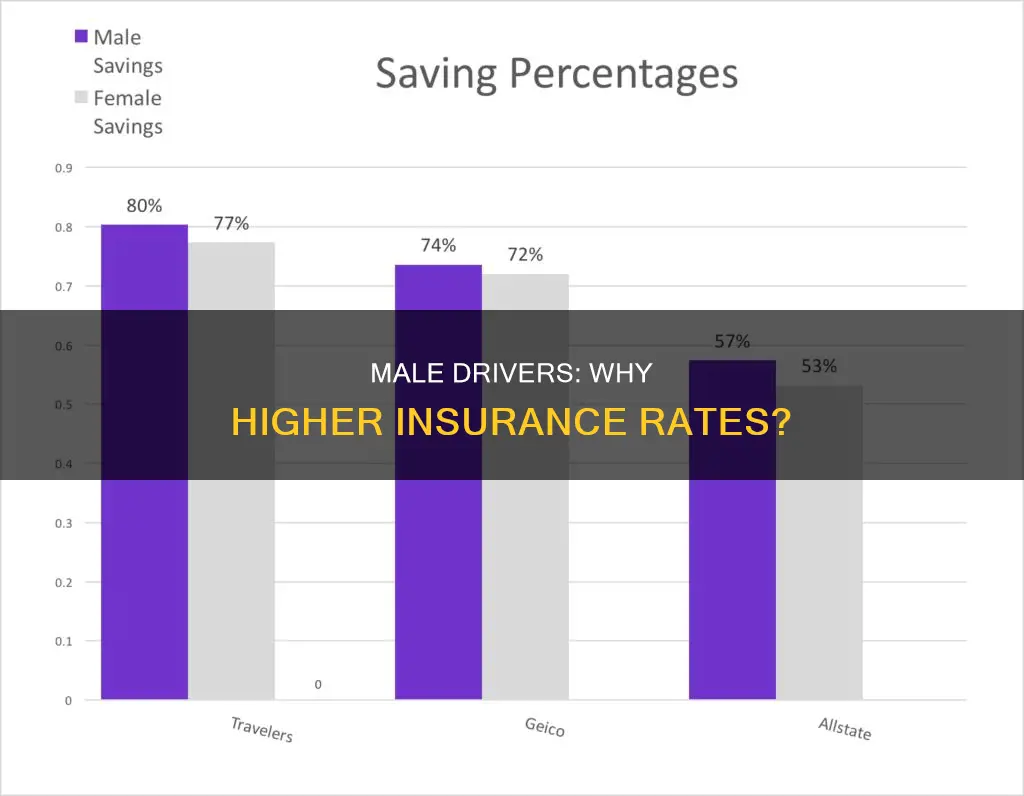

Male drivers often face higher insurance rates than their female counterparts due to various factors, including age, accident history, and driving behaviour. While the difference in rates between men and women is generally slim, it can become more pronounced during teenage years and after the age of 60. This is because younger male drivers are statistically more prone to accidents and risky driving behaviours, such as speeding and driving under the influence. In addition, the severity of accidents involving males tends to result in higher property damage and more severe injuries, leading to increased insurance claims and costs. However, it's important to note that insurance rates are not solely based on gender, and individual circumstances, driving records, age, vehicle type, and location also play a role in determining insurance premiums.

| Characteristics | Values |

|---|---|

| Accident Statistics | Historically, males have been involved in more accidents and higher-risk driving behaviors, such as speeding or driving under the influence. |

| Severity of Accidents | Accidents involving males tend to result in higher property damage and more severe injuries, leading to increased insurance claims and costs. |

| Mileage and Driving Habits | Males may tend to drive more miles and spend more time on the road, increasing their exposure to potential accidents. |

| Age Demographics | Younger male drivers, especially teenagers, are statistically more prone to accidents and risky driving behaviors, leading to higher insurance rates for this demographic. |

| Gender-Based Pricing | In the US, it is legal to determine car insurance rates based on gender in most states. States that prohibit gender-based pricing include California, Hawaii, Massachusetts, Michigan, Montana, North Carolina, and Pennsylvania. |

| Gender Gap | The gender gap in insurance rates narrows with age and driving experience, with rates becoming nearly equal during middle age. |

| DUI Statistics | Men are more likely to be arrested for driving under the influence (DUI) across all age groups. |

Explore related products

What You'll Learn

![]()

Male drivers are more prone to accidents and risky behaviour

Male drivers, especially teenagers and those under 25, are statistically more prone to accidents and risky driving behaviour. This includes speeding, reckless activities, driving under the influence of alcohol, and not wearing seat belts. Men in this age group are also more likely to drive with an excessive number of passengers. As a result of these behaviours, young male drivers are involved in more crashes and have higher insurance rates.

The severity of accidents also tends to be higher for male drivers, resulting in increased insurance claims and costs. This is due to a combination of factors, including the higher speed of collisions and the fact that men are more likely to drive cars that are more costly to insure. For example, a 16-year-old male driver pays on average $843 more than a female of the same age. At 19, males pay $241 per year compared to $219 for females, and at 25, the difference is still $107.

The gender gap in insurance rates narrows with age and driving experience. By the time male drivers reach their mid-twenties, their insurance rates decrease significantly. This is because insurance companies reassess risk profiles and driving maturity at ages 18, 21, and 25. As a result, the difference in insurance rates between men and women becomes minimal throughout most adult years, with only a slight difference of less than 1% between the ages of 30 and 60.

While gender is a factor in determining insurance rates, it is important to note that other factors also come into play, such as age, marital status, state requirements, driving record, vehicle type, and location. Additionally, some states and countries have implemented regulations that restrict or prohibit the use of gender as a rating factor. It is always advisable to shop around and compare insurance rates to find the most suitable plan.

High-Speed Chases: Insurance Claims and Coverage Complexities

You may want to see also

Explore related products

![]()

Men are more likely to drive under the influence

Men typically pay higher car insurance rates than women, especially when they are young. This is due to several factors, including accident statistics, the severity of accidents, and riskier driving behaviours. One of the key reasons is that men are more likely to drive under the influence of alcohol or drugs, which significantly increases their risk of accidents.

According to the National Survey on Drug Use and Health (NSDUH) in 2021, 13.5 million people aged 16 or older drove under the influence of alcohol, and 11.7 million drove under the influence of illicit drugs, with marijuana being the most common. The survey also revealed that men are more prone to driving under the influence than women. This trend is particularly pronounced in the 21-25 age group, where 15% of men drive under the influence compared to 7.5% of young adults aged 16-20 and 7.7% of adults over 26.

The higher incidence of drunk driving among men contributes to their increased accident risk. Men are more likely to be involved in crashes with a blood alcohol content (BAC) of .08 g/dL or higher, with four male drunk drivers for every female drunk driver in this category. This is a serious issue, as a BAC of .08 makes drivers approximately four times more likely to crash than those with a BAC of zero. The risk increases exponentially, with a BAC of .15 making drivers at least 12 times more likely to crash.

Young male drivers specifically tend to engage in riskier behaviours such as speeding, not wearing seat belts, and driving with excessive passengers. They are also more susceptible to driving under the influence, which is the leading cause of teenage deaths in car accidents. The combination of these factors results in higher insurance rates for young men compared to their female counterparts.

While drunk driving is a significant concern, it is important to note that driving under the influence of drugs, including prescription medications, can be equally dangerous. Men are more likely to drive after consuming drugs or alcohol, and this behaviour increases the risk of accidents and severe crashes. The presence of drugs in the system can impair driving abilities, affect judgement, and increase aggression and recklessness. Therefore, it is illegal and unsafe to drive under the influence of any substance.

Best Mile-Based Auto Insurance Companies: Pay-Per-Mile Plans

You may want to see also

Explore related products

![]()

Accidents involving males tend to be more severe

Male drivers, especially teenagers, are statistically more prone to accidents and risky driving behaviours, leading to higher insurance rates for this demographic. This is due to a variety of factors, including speeding, reckless activities, driving under the influence, and not wearing seat belts. Accidents involving males tend to be more severe, resulting in higher property damage and more severe injuries. This leads to increased insurance claims and costs. For example, drunk driving accidents are the number one cause of teenage deaths, and the statistics double for young men. Men made up 71% of all traffic fatalities in 2019, according to the National Highway Traffic Safety Administration.

The gender gap in insurance rates narrows with age and driving experience, with rates stabilising for men and women around 30 years old. However, the gap widens again for senior drivers, with 90-year-old males paying more due to driving more miles and potentially riskier conditions.

While gender is a significant factor in determining insurance rates, other factors such as age, marital status, state requirements, driving record, vehicle type, and location also play a role. It's worth noting that some states and countries have implemented regulations prohibiting the use of gender as a rating factor, recognising the need for equal rights and gender equality.

Auto Insurance Exceptions in Michigan

You may want to see also

Explore related products

![]()

Men drive more miles and spend more time on the road

Men typically drive more miles and spend more time on the road than women. This is supported by data from the National Household Travel Survey, 2001-2002, which shows that men drive longer distances (67 to 44 minutes per day) than women (21 to 38 miles per day). The survey also reveals that Americans make about 1,500 trips per person annually, with 45% of these trips being for shopping and errands, and 27% for social and recreational purposes.

The COVID-19 pandemic has significantly impacted driving patterns, with many people working from home or becoming unemployed, resulting in a notable decrease in daily commutes and vehicle travel. Despite these recent changes, motor vehicles in the US still travelled 3.2 trillion miles in 2022, a 10% increase from 2020. The average daily commute has also increased over the years, from 25 minutes in 2006 to 27.6 minutes in 2019, contributing to the overall annual mileage.

The higher mileage and time spent on the road by men increase their exposure to potential accidents, which is a factor considered by insurance companies when setting rates. Men's driving habits, including speeding and driving under the influence, also contribute to higher-risk behaviours that lead to more severe accidents and increased insurance costs.

While gender is a factor in determining insurance rates, other considerations, such as age, driving record, credit score, vehicle type, and location, also play a role. For example, younger male drivers, especially teenagers, are statistically more prone to accidents and risky driving behaviours, resulting in higher insurance rates for this demographic group. Additionally, adult men and women often pay similar insurance rates, with a price difference of less than 1% between men and women in their 30s.

When Accidents Happen: Understanding Total Loss Claims in Auto Insurance

You may want to see also

Explore related products

![]()

Gender-neutral insurance options

The use of gender as a factor in determining insurance rates has been a long-standing practice. In most states, insurance companies are allowed to consider gender when setting car insurance rates, with men paying about 1% more than women for car insurance coverage. The difference is more pronounced among younger drivers, with teenage boys paying the most. This is because insurers have found that young male drivers are more likely to be involved in car accidents and engage in riskier driving behaviours, such as speeding or driving under the influence.

However, there is a growing trend towards gender-neutral insurance options, with an increasing recognition of non-binary and gender-fluid identities. As of mid-2022, more than 20 states in the US offer gender-neutral options on driver's license forms, allowing individuals to choose "X" as their gender instead of "M" or "F". Some insurance companies in certain states also provide the option to list oneself as something other than male or female. Additionally, some states have implemented regulations that restrict or prohibit the use of gender as a rating factor, such as Washington, D.C. and Hawaii.

While the recognition of non-binary genders in insurance is a positive step, there are still challenges. For example, some insurers may still recommend that transgender or non-binary individuals list their sex designation at birth, which can impact their rates. Additionally, even when gender-neutral options are available, individuals may need to provide documentation to change their gender on their license, which can be a barrier.

To find affordable insurance rates, it is important to shop around and compare rates from different companies. Factors such as speeding tickets or at-fault accidents can impact rates, and the difference in pricing between insurers may be greater than the difference between genders. Other factors that can influence insurance rates include age, driving record, vehicle type, location, and credit score. By considering these factors and comparing rates, individuals can find the best coverage that suits their needs, regardless of gender.

Understanding Auto Insurance: What Does Deduce Mean?

You may want to see also

Frequently asked questions

Yes, males tend to have higher insurance rates. This is due to several statistical factors and risk assessments made by insurance companies. Some reasons include accident statistics, the severity of accidents, and mileage and driving habits.

Males have higher insurance rates because they are involved in more accidents and risky driving behaviours, such as speeding or driving under the influence. Men are also more likely to drive a car that is more costly to insure.

The difference in insurance rates between males and females varies with age. Teenage boys pay the most for car insurance, with rates dropping significantly between the ages of 16 and 25. After age 25, the difference in insurance rates between males and females becomes smaller, with rates stabilising around $106 per month for both genders by age 30.