Pitchers, particularly those in professional baseball, often face significant financial risks due to the potential for career-ending arm injuries. Given the immense strain placed on their throwing arms, many pitchers explore options to protect their livelihoods, including insuring their arms. This practice, known as disability insurance or loss of value insurance, provides financial coverage in the event of a career-threatening injury. While not all pitchers choose to insure their arms, those who do often invest in policies that can cover millions of dollars, ensuring financial stability if their playing days are cut short. This topic raises questions about the cost, availability, and necessity of such insurance, as well as the broader implications for athlete financial planning and risk management.

| Characteristics | Values |

|---|---|

| Common Practice | Yes, many professional pitchers insure their arms, particularly their throwing arm, due to the high risk of injury. |

| Insurance Type | Disability insurance is the most common type, covering loss of income if the pitcher cannot play due to injury. |

| Coverage Amount | Policies can range from $1 million to $20 million or more, depending on the player's contract and risk assessment. |

| Premium Costs | Premiums vary widely, typically 1-5% of the coverage amount annually, influenced by the pitcher's health, age, and injury history. |

| Injury Risks Covered | Common injuries include UCL tears (requiring Tommy John surgery), rotator cuff injuries, and labrum tears. |

| Notable Examples | Players like Aaron Nola and Jacob deGrom have publicly discussed insuring their arms. |

| Team Involvement | Teams often encourage or require players to have insurance, but policies are usually purchased individually. |

| Policy Duration | Policies can be short-term (e.g., one season) or long-term, depending on the player's career stage and risk tolerance. |

| Underwriting Process | Involves medical exams, injury history review, and performance data analysis to determine premiums and coverage. |

| Tax Implications | Premiums are typically paid with after-tax dollars, and payouts may be tax-free depending on jurisdiction. |

Explore related products

$10.82 $22

$10.25 $17.99

![FORTRESS 7’ x 7’ L-Screen Frame & Net [Nimitz Edition] - Premium Protection for Pitchers & Coaches - Baseball Protector Screen](https://m.media-amazon.com/images/I/91hTHr6+14L._AC_UY218_.jpg)

What You'll Learn

- Cost of Arm Insurance - Premiums, coverage limits, and factors affecting insurance costs for pitchers

- Common Injuries Covered - Types of arm injuries typically included in insurance policies

- Insurance Providers - Companies offering specialized arm insurance for professional pitchers

- Contract Requirements - Team mandates for pitchers to have arm insurance in contracts

- Claim Process - Steps to file a claim and receive compensation for arm injuries

![]()

Cost of Arm Insurance - Premiums, coverage limits, and factors affecting insurance costs for pitchers

The cost of arm insurance for pitchers can be a significant investment, with premiums varying widely based on several factors. Typically, pitchers can expect to pay anywhere from $10,000 to $50,000 or more annually for a comprehensive policy. These premiums are influenced by the pitcher's age, health history, and the specific terms of the policy. For instance, a young, healthy pitcher with a clean medical record may secure a policy at the lower end of the spectrum, while an older pitcher with a history of arm injuries could face substantially higher costs. The insurance market for athletes is niche, and underwriters carefully assess risk before offering coverage.

Coverage limits for arm insurance policies are another critical aspect to consider. Most policies cap payouts between $5 million and $20 million, depending on the pitcher's contract value and the insurer's risk assessment. For example, a high-profile Major League Baseball (MLB) pitcher with a multi-million-dollar contract might opt for a higher coverage limit to protect their earning potential. In contrast, a minor league pitcher may choose a lower limit to keep premiums manageable. It’s essential for pitchers to evaluate their financial exposure and select a policy that aligns with their career stage and income level.

Several factors directly impact the cost of arm insurance for pitchers. One of the most significant is the pitcher's injury history. Insurers scrutinize past injuries, particularly those involving the elbow or shoulder, as these areas are most susceptible to damage in pitchers. Additionally, the pitcher's age plays a crucial role, as younger pitchers are often seen as lower-risk compared to their older counterparts. The pitcher's role and workload also matter; a starting pitcher who throws more innings annually will likely face higher premiums than a relief pitcher. Lastly, the pitcher's current contract and earning potential influence costs, as insurers must account for the potential loss of income due to injury.

Another factor affecting insurance costs is the specific terms and conditions of the policy. Some policies may exclude coverage for pre-existing conditions or require a waiting period before claims can be filed. Others might include clauses that reduce payouts if the pitcher fails to adhere to a prescribed training or recovery regimen. Pitchers must carefully review these details to ensure they are adequately protected. Working with a specialized insurance broker who understands the unique needs of professional athletes can help pitchers navigate these complexities and find a policy that offers the best value.

Finally, the cost of arm insurance is also shaped by broader market trends and the insurer's appetite for risk. During periods of high-profile pitching injuries, insurers may raise premiums across the board to mitigate potential losses. Conversely, in years with fewer injuries, premiums might stabilize or even decrease. Pitchers should monitor these trends and be prepared to adjust their coverage as needed. Ultimately, while arm insurance can be expensive, it provides invaluable financial security, allowing pitchers to focus on their performance without the added stress of potential career-ending injuries.

The Catholic Church and Insurance: An Unlikely Partnership

You may want to see also

Explore related products

![]()

Common Injuries Covered - Types of arm injuries typically included in insurance policies

Pitchers, given the repetitive and high-velocity nature of their throwing motions, are particularly susceptible to arm injuries. As a result, many pitchers and their teams invest in specialized insurance policies to protect against financial losses due to career-threatening injuries. These policies often cover a range of arm injuries that are common in pitching. Below are the types of arm injuries typically included in such insurance policies.

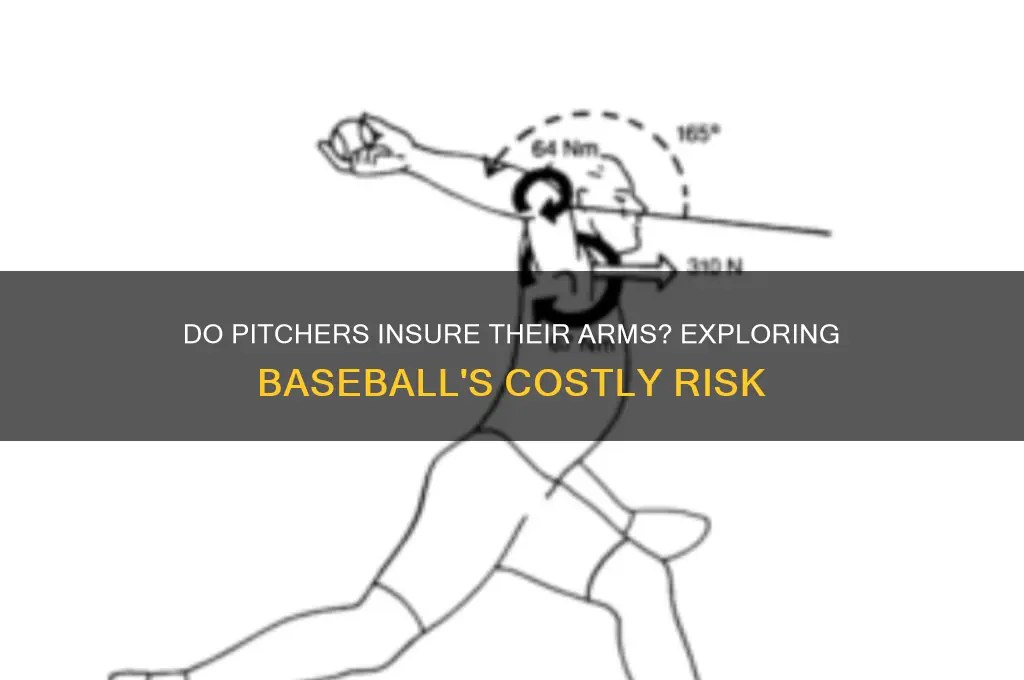

Rotator Cuff Injuries are among the most common issues pitchers face. The rotator cuff, a group of muscles and tendons stabilizing the shoulder, can be strained or torn due to overuse. Insurance policies often cover surgeries like rotator cuff repairs, arthroscopic debridement, and rehabilitation costs associated with these injuries. Given the critical role of the shoulder in pitching, such coverage is essential for a pitcher’s career longevity.

Ulnar Collateral Ligament (UCL) Tears are another frequently covered injury, often requiring Tommy John surgery. This procedure involves reconstructing the UCL using a tendon from another part of the body. Due to the high cost and lengthy recovery period, insurance policies typically include coverage for the surgery, post-operative care, and physical therapy. UCL injuries are prevalent in pitchers due to the extreme stress placed on the elbow during throwing.

Labrum Tears in the shoulder or hip are also commonly covered. The labrum, a ring of cartilage surrounding the socket of the shoulder or hip joint, can tear from repetitive motion or acute trauma. Insurance policies often account for arthroscopic surgeries to repair labrum tears, as well as the extensive rehabilitation required to regain strength and mobility. Pitchers are particularly prone to shoulder labrum injuries due to the overhead throwing motion.

Flexor Tendon Injuries in the forearm and elbow are included in many policies as well. These injuries occur when the tendons connecting the forearm muscles to the elbow bone become strained or torn. Coverage typically extends to surgical repairs, such as tendon reattachment or grafting, and the subsequent rehabilitation process. Flexor tendon injuries can sideline pitchers for months, making insurance coverage crucial.

Biceps Tendon Ruptures are less common but still covered in many policies. The biceps tendon, which attaches the biceps muscle to the shoulder, can rupture from overuse or sudden stress. Insurance often covers surgical repair, which may involve reattaching the tendon to the bone, as well as the rehabilitation needed to restore function. While not as frequent as other injuries, biceps tendon ruptures can significantly impact a pitcher’s performance.

In summary, insurance policies for pitchers typically cover a range of arm injuries, including rotator cuff injuries, UCL tears, labrum tears, flexor tendon injuries, and biceps tendon ruptures. These policies are designed to mitigate the financial risks associated with the high-stress demands of pitching, ensuring that pitchers can focus on recovery and return to the game.

Unbelievably Strange: Exploring the World of Bizarre Insurance Policies

You may want to see also

Explore related products

![]()

Insurance Providers - Companies offering specialized arm insurance for professional pitchers

In the high-stakes world of professional baseball, pitchers often seek ways to protect their most valuable asset—their throwing arm. While traditional disability insurance covers general injuries, specialized arm insurance tailored for pitchers is a niche but crucial offering. Several insurance providers recognize the unique risks pitchers face, such as ligament tears, tendon injuries, or repetitive stress damage, and have developed policies to address these specific concerns. These specialized plans typically offer coverage for medical expenses, rehabilitation costs, and lost income due to arm-related injuries, ensuring pitchers can focus on recovery without financial strain.

One notable provider in this space is Lloyd's of London, a renowned insurance marketplace known for its willingness to underwrite unique and high-risk policies. Lloyd's has historically offered customized arm insurance for professional athletes, including pitchers. These policies are often tailored to the individual's contract value, playing style, and injury history, providing comprehensive protection. Pitchers working with Lloyd's can expect detailed assessments and coverage that extends beyond standard disability insurance, including provisions for career-ending injuries.

Another key player is The Hartford, a company that has expanded its disability insurance offerings to include specialized coverage for professional athletes. While not exclusively focused on pitchers, The Hartford provides policies that can be adapted to cover arm injuries, including those specific to pitching. Their plans often include benefits like rehabilitation coverage, which is critical for pitchers recovering from surgeries like Tommy John. The Hartford's reputation for reliability and its focus on long-term recovery make it a preferred choice for many athletes.

For pitchers seeking more localized options, Specialized Insurance Services (SIS) is a boutique provider that caters specifically to professional athletes. SIS offers arm insurance policies designed to meet the unique needs of pitchers, including coverage for both acute injuries and chronic conditions. Their policies often include additional benefits like access to top sports medicine specialists and personalized recovery programs. SIS's focus on athlete-specific risks and their commitment to individualized care set them apart in this niche market.

Lastly, Aon plc, a global professional services firm, provides specialized insurance solutions for athletes through its Aon Sports division. Aon works with pitchers to create bespoke policies that cover arm injuries, factoring in the athlete's earning potential and career trajectory. Their expertise in risk management and their extensive network of insurers allow them to offer competitive premiums and comprehensive coverage. Aon's policies often include provisions for both on-field and off-field risks, ensuring pitchers are protected in all aspects of their careers.

When considering arm insurance, pitchers should carefully evaluate the terms, coverage limits, and exclusions of each policy. Working with an experienced agent who understands the demands of professional baseball can help ensure the chosen plan provides adequate protection. As the industry evolves, more insurers are likely to enter this space, offering pitchers even greater options to safeguard their careers.

Unlocking Cash from Life Insurance Policies

You may want to see also

Explore related products

![]()

Contract Requirements - Team mandates for pitchers to have arm insurance in contracts

In recent years, the topic of arm insurance for pitchers has gained traction in professional baseball, prompting teams to reevaluate their contract requirements. As pitchers are among the most valuable assets in a team’s roster, protecting their health and financial stability has become a priority. Teams are increasingly mandating that pitchers secure arm insurance as part of their contracts to mitigate risks associated with career-threatening injuries. These mandates ensure that both the player and the team are financially protected in the event of a catastrophic arm injury, such as a torn UCL requiring Tommy John surgery or a rotator cuff tear. By incorporating arm insurance into contracts, teams aim to safeguard their investments while providing pitchers with peace of mind regarding their long-term financial security.

Contract requirements for arm insurance typically outline specific terms and conditions that pitchers must adhere to. These provisions often include the minimum coverage amount, which is usually based on the player’s salary and potential earnings. For instance, a contract might stipulate that a pitcher must carry a policy covering at least 50% of their annual salary for a defined period, such as three to five years. Additionally, teams may require that the insurance policy cover both on-field and off-field injuries to the pitcher’s arm, ensuring comprehensive protection. The contract may also specify that the team has the right to review and approve the insurance policy to ensure it meets their standards and adequately addresses potential risks.

Another critical aspect of these mandates is the inclusion of clauses that address premium payments and policy maintenance. Teams often require pitchers to bear the cost of the insurance premiums, though some organizations may offer to cover a portion or all of the expenses as an added benefit. Contracts may also include provisions that obligate pitchers to maintain continuous coverage throughout the duration of their contract, with penalties for non-compliance. This ensures that the insurance remains active and effective, providing uninterrupted protection for both the player and the team. Failure to maintain the policy could result in fines, contract adjustments, or other consequences as outlined in the agreement.

Furthermore, teams are increasingly incorporating language into contracts that clarifies the claims process and the role of the team in the event of an injury. This includes specifying the steps a pitcher must take to file a claim, such as providing medical documentation and adhering to team-approved treatment plans. Contracts may also outline how the insurance payout will be distributed, whether it goes directly to the player, the team, or a combination of both. Some teams may use a portion of the payout to offset medical expenses or lost salary, while ensuring the pitcher receives adequate compensation for their injury. This transparency helps prevent disputes and ensures all parties understand their responsibilities.

Lastly, as arm insurance becomes more prevalent, teams are beginning to view it as a standard component of player contracts, particularly for high-value pitchers. This shift reflects a broader trend in professional sports toward prioritizing player health and financial security. By mandating arm insurance, teams not only protect their investments but also demonstrate a commitment to the well-being of their athletes. As the industry evolves, it is likely that more teams will adopt these requirements, making arm insurance a non-negotiable element of pitcher contracts. This proactive approach benefits both the organization and the player, fostering a more stable and supportive environment in professional baseball.

Life Insurance and Experimental Vaccines: What's Covered?

You may want to see also

Explore related products

$13.99 $19.99

![]()

Claim Process - Steps to file a claim and receive compensation for arm injuries

Pitchers, particularly those in professional baseball, often insure their arms as a safeguard against career-threatening injuries. When an arm injury occurs, understanding the claim process is crucial to receiving timely compensation. The first step in filing a claim is to notify your insurance provider immediately. Most policies require prompt notification to initiate the process. Contact your insurance agent or the company’s claims department via phone or email, providing your policy number and a brief description of the injury. Delaying this step could result in complications or denial of the claim.

Once the insurer is notified, the next step is to gather and submit all necessary documentation. This typically includes medical records detailing the injury, diagnostic reports (such as MRIs or X-rays), and a physician’s statement confirming the injury’s severity and its impact on your ability to perform as a pitcher. Additionally, you may need to provide proof of the injury’s occurrence, such as incident reports or witness statements. Ensure all documents are accurate and complete to avoid delays in processing.

After submitting the required documentation, the insurance company will review your claim and conduct an investigation. This may involve an independent medical examination (IME) to verify the extent of the injury and its relation to your profession. The insurer may also review your policy terms to ensure the injury is covered. During this stage, it’s essential to cooperate fully with the insurer’s requests and provide any additional information promptly.

Once the investigation is complete, the insurer will determine the claim’s validity and calculate compensation. If approved, compensation may cover medical expenses, rehabilitation costs, and lost income due to the inability to play. The amount is typically based on the policy’s terms, the injury’s severity, and the impact on your career. If the claim is denied, you have the right to appeal the decision, often by providing further evidence or requesting a review by a third party.

Finally, upon approval, you will receive compensation as outlined in your policy. This may be a lump sum or periodic payments, depending on the agreement. It’s important to review the payment terms and ensure they align with your needs. Throughout the process, maintaining open communication with your insurer and seeking legal advice if necessary can help ensure a smooth and fair outcome. Filing a claim for an arm injury requires diligence and attention to detail, but it can provide critical financial support during recovery.

High Blood Pressure: Getting Life Insurance Coverage

You may want to see also

Frequently asked questions

Yes, some professional pitchers purchase insurance policies to protect their throwing arms, which are essential to their careers. These policies can cover loss of income due to career-ending injuries.

The cost varies widely based on the pitcher’s salary, injury history, and policy terms. Premiums can range from tens of thousands to millions of dollars annually, with payouts often matching the player’s potential earnings.

Arm insurance typically covers loss of income if a pitcher’s career is ended or significantly impacted by an injury to their throwing arm. It may also include coverage for medical expenses related to the injury.