Term life insurance is a financial product that provides financial security to your family in the event of your death. The rates of premiums for term life insurance have been increasing in recent years, with a hike of 2.79% observed after April 2022, and predictions of a 20-40% increase in 2022. This increase is attributed to various factors, including rising inflation, changes in health, and lifestyle choices. While the rate increases may be concerning, it is still advisable to purchase term insurance early to secure lower premiums. Term insurance premiums are influenced by age, with older individuals typically paying more due to increased risks. Additionally, the type of term policy chosen can impact premium changes, with level or fixed-term policies offering predictable payments. Understanding these factors can help individuals make informed decisions about their term life insurance choices.

| Characteristics | Values |

|---|---|

| Do term insurance rates go up? | Yes, term insurance rates have gone up in recent years and are expected to continue increasing. |

| Factors influencing rate increases | - Age: Premiums increase with age as the risk of death is higher. |

- Health and lifestyle: Changes in health and lifestyle, such as starting to smoke, can impact rates.

- Economic conditions: Inflation and changes in the economy can cause rate adjustments.

- Industry factors: Advances in medical technology and changes in regulations can affect how insurers assess risk and set premiums.

- Reinsurance costs: Higher claims due to COVID-19 have increased costs for reinsurance companies, which has been passed on to customers through higher premiums. | | Ways to mitigate rate increases | - Buy term insurance early: Premiums are lower when purchased at a younger age due to good health conditions.

- Maintain a healthy lifestyle: Improving health and avoiding risky behaviours can lead to lower rates.

- Compare plans: Shopping around and comparing rates from multiple companies can help find more affordable options. |

Explore related products

What You'll Learn

![]()

Premium rates increase with age

Term life insurance rates are influenced by a variety of factors, including age, health, gender, and lifestyle choices. While age is a significant determinant, it is not the sole factor influencing premium rates.

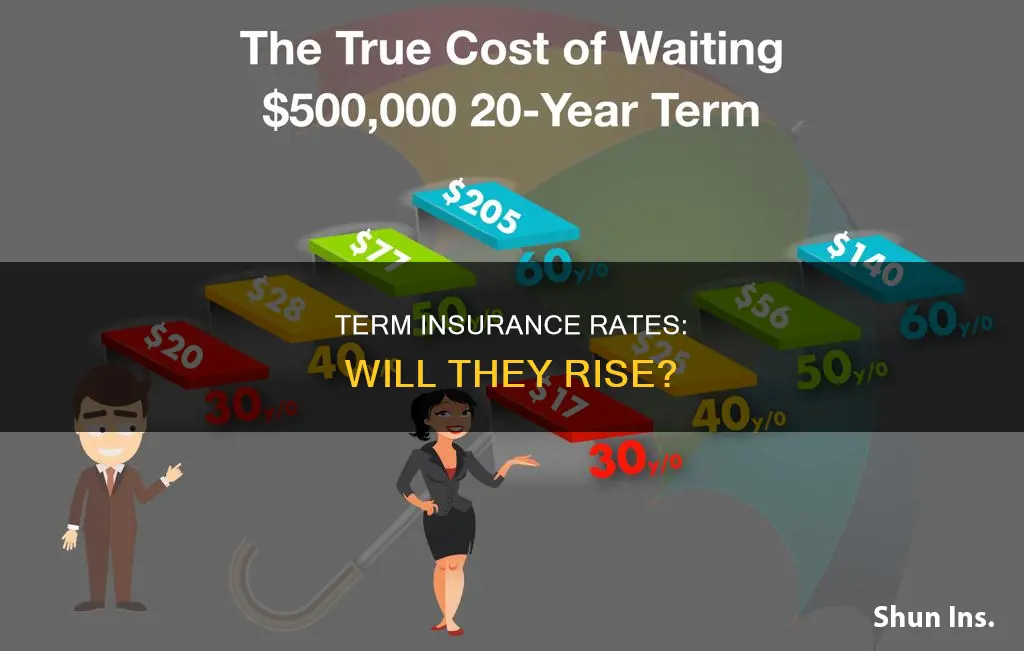

Age plays a pivotal role in determining life insurance premiums. As people age, the likelihood of passing away increases, elevating the risk to insurers. This increase in risk is reflected in higher premium rates for older individuals. The annual premium or "rate" for a term life insurance policy is typically determined when the policy is purchased and remains fixed for the duration of the term. However, if the insured outlives the initial term and renews the policy, the premium is adjusted to reflect their new age, resulting in a higher rate.

The impact of age on term life insurance rates can be significant. On average, the premium amount increases by about 8% to 10% for every year of age. For example, a 45-year-old male may pay an average of $1,125 for a new 20-year term policy with $1,000,000 in coverage. If he were to purchase the same policy at age 46, the cost would increase to $1,225, and it would further increase to $1,345 if purchased at age 47. These incremental increases in premium rates with each successive age are due to the rising mortality charges, which result in a bigger drain on the cash value of the policy.

In addition to age, other factors such as health, gender, and lifestyle choices can also affect term life insurance rates. Generally, women tend to pay lower premiums than men due to their longer life expectancy. Maintaining a healthy lifestyle, such as quitting smoking or losing weight, can improve an individual's insurance risk classification and lower their premiums. Additionally, the type of policy chosen, such as the length of the term and the amount of coverage, will also impact the premium rates.

It is important to note that term life insurance rates may also be influenced by broader economic conditions, regulatory changes, and advances in medical technology. These factors can cause insurers to adjust their risk assessment, resulting in changes to premium rates. Therefore, it is advisable to purchase term life insurance as early as possible to lock in lower premium rates and avoid the impact of age-related increases.

Vision Insurance: Cataract Care Covered?

You may want to see also

Explore related products

$15.45 $14.95

![]()

Premium rates depend on health and lifestyle

Term insurance premium rates depend on several factors, including an individual's health and lifestyle. Generally, younger and healthier individuals pay lower premiums as they are considered lower risk. Insurers charge lower premiums to younger individuals due to their good health conditions. Similarly, women tend to be offered more favourable premium rates than men because, on average, they have a longer life expectancy.

On the other hand, older individuals often face higher premiums due to potential health concerns. As a person grows older, the level of risk to be taken by the insurers increases, leading to higher premiums. Additionally, if an individual's health deteriorates over time, their term premiums may increase. Certain conditions, such as heart disease or kidney issues, can run in families, and a family medical history of these problems could potentially increase an individual's premium.

Lifestyle choices can also impact premium rates. For example, smoking increases the level of risk for insurers and will likely result in higher premiums. Maintaining a healthy lifestyle can help lower premiums, and avoiding behaviours like smoking can contribute to this.

When determining premium rates, insurers consider various factors, including age, gender, health, family medical history, current health conditions, and lifestyle. By assessing these factors, insurers can adjust their coverage plans to cater to the specific needs and risks of their clients.

How New Drivers Can Get Cheaper Insurance Rates

You may want to see also

Explore related products

![Life Insurance Premiums: How Computed, Tested, and Valued 1902 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

![]()

Premium rates are influenced by economic conditions

Premium rates are influenced by a multitude of factors, including economic conditions, regulatory changes, and technological advancements. Economic conditions play a significant role in shaping premium rates. For instance, during an economic downturn, consumer spending tends to decrease, which may prompt insurers to adjust their pricing strategies to maintain competitiveness. Insurers closely monitor economic trends and make adjustments to their pricing models to adapt to changing market conditions.

Economic factors, such as inflation, also contribute to the fluctuation of premium rates. As inflation rises, insurers may increase their premium rates to cover their own increased costs and maintain profitability. This ensures that they can continue to provide the promised coverage to their customers. Additionally, economic conditions can influence the investment portfolios of insurance companies. Changes in investment returns can impact the financial stability of insurers, leading them to adjust their premium rates accordingly.

Furthermore, economic conditions can affect the demand for certain types of insurance. For example, during challenging economic times, individuals may opt for more affordable insurance plans or reduce their overall spending on insurance products. This shift in consumer behaviour can influence premium rates as insurers adjust their pricing strategies to attract and retain customers.

It is worth noting that economic conditions do not operate in isolation when determining premium rates. Regulatory changes and advancements in technology also play a role. Legislation and market regulations can impact the pricing mechanisms of insurance companies, leading to adjustments in premium rates to comply with legal requirements and market standards.

Additionally, the adoption of data analytics and sophisticated algorithms has enabled insurers to refine their pricing models. By leveraging technological advancements, insurers can enhance their risk assessments, resulting in more dynamic premium rates that reflect the evolving economic landscape.

Male Insurance Rates: When Do They Drop?

You may want to see also

Explore related products

![]()

Premium rates can be lowered by buying early

Term insurance premium rates can be lowered by buying a policy early in life. This is because, as a person grows older, the level of premiums increases, as the risk to be taken by the insurers increases with age. Therefore, buying term insurance at a younger age can help you pay a lower price from the start.

Insurers charge lower premiums for younger individuals due to their good health conditions. A person may pay more when their lifestyle choices or health conditions make them riskier to insure. For example, smokers pay significantly higher premiums than non-smokers due to the increased health risks associated with smoking.

The rate of premium also depends on the type of term policy chosen. For instance, fixed-term policies have the same payment throughout the term, while annual renewable term policies allow the same premiums throughout the term but may increase the price upon renewal based on factors like age and health status. Decreasing term policies have premiums that decrease over time, while increasing term policies may increase premium payments to raise the value of the death benefit.

It is important to note that term insurance premium rates have been increasing in recent years, with a hike of 2.79% observed after April 2022. This was attributed to the second wave of COVID-19. Therefore, buying term insurance early can help lock in lower premium rates and avoid future increases.

Overall, buying term insurance early in life can help secure lower premium rates due to reduced health risks and the ability to choose from a variety of policy options.

TitleMax: Pawn Insurance?

You may want to see also

Explore related products

![]()

Premium rates can change during the term

Term insurance is a necessity for everyone, providing financial security to your family in the event of your untimely death. While the rate you pay for term life insurance is typically fixed for the duration of the term, it can change during the term or when you renew the policy.

There are several factors that can cause term life insurance rates to change over time. Firstly, as a person grows older, the level of premiums tends to increase because the risk to be taken by the insurers increases with age. Changes in health or lifestyle, such as developing a pre-existing health condition or taking up smoking, can also impact your rates.

Beyond individual factors, economic conditions, regulation changes, and medical technology advances can influence the insurance industry as a whole. For example, in 2022, reinsurance companies, which help limit the risk and loss for insurance companies, increased their charges due to higher claims during the COVID-19 pandemic. As a result, insurance companies passed on the higher costs to their customers by raising premiums.

Additionally, the type of term policy you choose can also affect whether your premium rates change during the term. With an annual renewable policy, your premiums may increase each year as you get older. On the other hand, a level or fixed-term policy guarantees that your premiums will stay the same for the duration of the term.

It is important to note that term life insurance rates can vary across different insurance providers. Therefore, it is advisable to shop around and compare rates from multiple companies to find the best option for your needs.

Insurance Coverage: Does It Carry Over?

You may want to see also

Frequently asked questions

Yes, term insurance rates can go up over time. While the rate usually stays the same for the duration of the term, it can change during the term or when you renew the policy.

Term insurance rates can go up due to a variety of factors, including age, health, lifestyle choices, and broader economic conditions. As a person grows older, the level of premiums increases as the risk to insurers increases. Changes in health and lifestyle, such as starting to smoke, can also impact rates. Additionally, economic factors such as inflation and advances in medical technology can influence rate adjustments.

There are several strategies to keep term insurance rates low. Buying term insurance at a younger age can help secure lower premiums due to better health conditions. Maintaining a healthy lifestyle, comparing rates from multiple companies, and choosing the right plan for your unique needs can also help minimize rate increases.