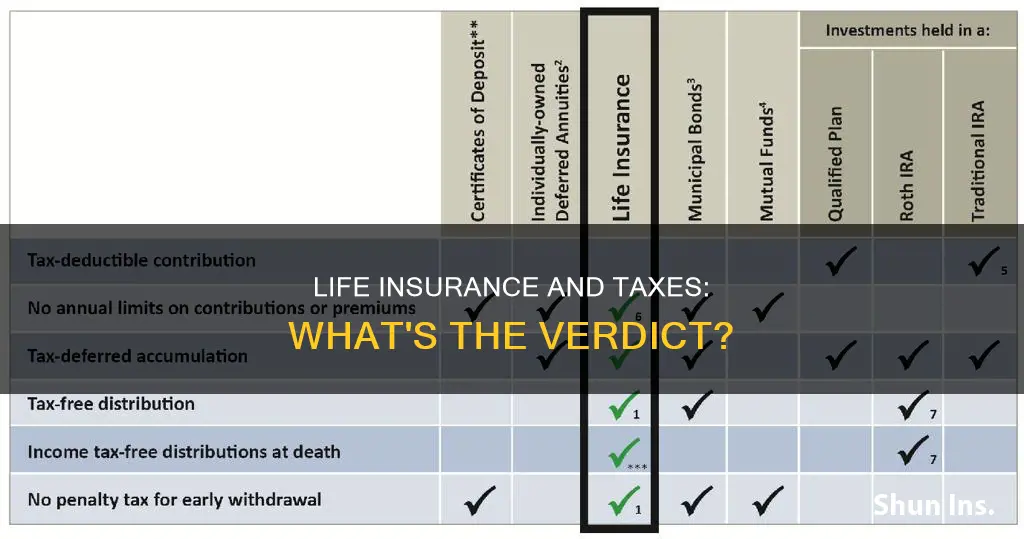

Life insurance payouts are usually tax-free, but there are situations where taxes may be incurred. For example, if the policy has grown in value, is part of a larger estate, or if the beneficiary is a minor. Additionally, if the benefit payout is delayed and the money is held by the insurance company, taxes may be owed on the interest generated. In the case of cash value life insurance, withdrawals up to the amount paid in are typically tax-free. However, certain tax advantages may be lost if too much money is put into the policy within its first seven years or after a material change. While life insurance proceeds are generally not considered taxable income, it's important to note that any interest received is taxable and should be reported accordingly.

| Characteristics | Values |

|---|---|

| Are life insurance proceeds taxable? | Generally, life insurance proceeds received by beneficiaries due to the death of the insured are not taxable. |

| Are there any exceptions? | Yes, if the beneficiary receives the payout in installments, they may be taxed on the interest generated during that period. |

| Are there taxes on cash value life insurance? | Withdrawals from the policy's cash value are usually tax-free as long as they don't exceed the amount paid in. |

| Are there other situations where taxes may apply? | Yes, if the policy has grown in value or is part of a larger estate, or if the proceeds are received by minor children from a previous marriage. |

| Can medical expenses be deducted? | Yes, eligible unreimbursed medical expenses may be deductible. |

Explore related products

What You'll Learn

![]()

Life insurance payouts to beneficiaries are usually tax-free

Life insurance payouts to beneficiaries are generally not considered taxable gross income and do not need to be reported on income taxes. This means that beneficiaries will receive the full amount, which can be used for expenses like funeral costs, paying off debts, or securing their future. However, there are a few situations where taxes may be incurred on life insurance proceeds.

Firstly, if the beneficiary receives the payout in installments rather than as a lump sum, it may be subject to hidden taxes. Secondly, if there are unpaid loans against the policy, they will be deducted from the death benefit, resulting in a lower payout for the beneficiaries. Thirdly, if the policy is a modified endowment contract (MEC), withdrawals are treated as taxable income until they equal all interest earnings in the contract.

Another scenario where taxes come into play is when the policyholder leaves the death benefit to their estate instead of directly naming a person as the beneficiary. In this case, the value of the life insurance proceeds is included in the gross estate, and the person(s) inheriting the estate may have to pay estate taxes. Additionally, if the policyholder delays the benefit payout and the money is held by the insurance company, earning interest, the beneficiary will likely have to pay taxes on the interest generated during that period.

To avoid paying taxes on life insurance proceeds, individuals can consider transferring ownership of the policy to another person or entity. This can be done by choosing a competent adult or entity as the new owner, contacting the insurance company for the proper assignment or transfer of ownership forms, and having the new owner pay the premiums. However, it's important to note that making such a transfer will result in the loss of rights to make changes to the policy in the future.

Insurance Adjuster Licensing Reciprocity: Florida and Texas' Agreement Explored

You may want to see also

Explore related products

$5.99 $19.99

![]()

Interest on life insurance is taxable

Life insurance payouts are usually tax-free, but there are situations where the IRS may get involved, especially if the policy has grown in value or is part of a larger estate. The death benefit paid out to beneficiaries is typically not taxed as income, but there are some exceptions.

If the death benefit from a term life insurance policy is paid out in installments rather than a lump sum, any interest that accumulates on those payments will be taxed as regular income. The beneficiary must report this interest as income received. Interest credited to a dividend accumulation account is currently taxable to the policyowner.

In the case of cash value life insurance, policyholders can generally borrow or withdraw money from the policy's cash value. As long as they don't withdraw more than they've paid in, those withdrawals are usually tax-free. However, if there are unpaid loans against the policy, they will be deducted from the death benefit, reducing the amount received by beneficiaries. If the policy is a modified endowment contract (MEC), withdrawals are treated as taxable income until they equal all interest earnings in the contract.

It is important to note that policy loans that are eliminated during a 1035 exchange are taxable if there is any gain in the policy at the time of the exchange. While premiums are generally not tax-deductible, it is advisable to consult a tax advisor to confirm if there are any exceptions in specific cases.

The Georgia Insurance Adjuster Exam: Open Book or Closed Book?

You may want to see also

Explore related products

![]()

Withdrawing more than you've paid into a policy may be taxed

Life insurance payouts to beneficiaries are generally not taxable. However, there are certain situations where taxes may be incurred. One such scenario is when the withdrawal amount exceeds the total premiums paid into the policy. In this case, the excess amount withdrawn may be subject to income tax.

The tax implications of withdrawing more than you've paid into a life insurance policy depend on various factors, including the type of policy, the timing of the withdrawal, and the specific tax regulations in your jurisdiction. It is always recommended to consult a tax professional for personalized advice.

When you withdraw more than the total premiums paid, the excess amount is typically considered a gain or earnings on the policy. These gains are treated as taxable income by the IRS. The portion of your withdrawal that exceeds your basis in the policy will generally be subject to income tax. Your basis in the policy refers to the amount of premiums you have paid, minus any prior withdrawals or dividends received.

It is important to note that different types of life insurance policies have varying tax treatments. For example, cash-value life insurance policies, such as whole life or universal life, allow policyholders to build cash value within the policy. With these policies, you can generally make tax-free withdrawals up to the amount of premiums you have paid. However, once your withdrawals exceed this amount, the gains become taxable.

Additionally, the timing of the withdrawal can also impact its tax treatment. For instance, if you surrender or cancel your policy during its early years, when the cash value is relatively low, you may be subject to surrender fees or early withdrawal penalties. These fees can reduce the amount of cash you receive and, consequently, impact the taxable portion of your withdrawal.

To summarize, while life insurance proceeds are generally tax-free, withdrawing more than you've paid into the policy may trigger tax consequences. The excess amount withdrawn is typically treated as taxable income. It is important to understand the specific rules of your policy and consult a tax advisor to navigate the tax implications of your life insurance proceeds.

Credit Union Money Market Accounts: Are They Insured?

You may want to see also

Explore related products

![]()

Death benefits paid to an estate may be taxed

Life insurance payouts to beneficiaries are typically tax-free. However, there are certain situations where the IRS may get involved, especially if the policy is part of a larger estate.

Death benefits from life insurance policies are generally not subject to ordinary income tax. However, if the beneficiary receives the death benefit in installments that include interest, then the interest will be taxable. If the death benefit is paid to the estate, it may be subject to federal or state estate tax if the estate exceeds the estate tax exemption amount. The death benefit may also be included in the estate if the beneficiary dies before the policyholder and the policyholder does not name a new beneficiary.

The IRS has rules to help determine the ownership of a life insurance policy when the insured person passes away. One such regulation, the three-year rule, subjects gifts made within three years of death to federal estate tax. This means that if the creator of the policy dies within three years of transferring ownership, the death benefits are included in their estate as if they still owned the policy.

The size of the estate, the type of policy, and the mode of payment to the beneficiaries are some of the determining factors for taxation. For example, if the policyholder delays the payout and the insurance company holds the money, allowing it to generate interest, that interest may be subject to tax. The same applies if beneficiaries elect to receive the payout as an annuity instead of a lump sum.

How Insurers Invest Policyowner Money in Dividends

You may want to see also

Explore related products

![]()

Policy transfers may be taxed

Life insurance payouts are often received tax-free by beneficiaries. However, there are certain situations where taxes could impact your life insurance proceeds. One such scenario is when a policy is transferred for value, which can trigger taxation under the "transfer-for-value" rule.

The transfer-for-value rule was established to discourage the practice of transferring life insurance policies between parties to obtain large tax-free windfalls. Under this rule, if a life insurance policy is transferred for any kind of material consideration, the death benefit payout may become partially or fully taxable. This rule removes the tax-exempt status of the policy, and the purchaser has to pay income tax on a portion or the entirety of the death benefit.

The definition of "consideration" in this context is crucial. While it typically refers to monetary payments, it can also include reciprocal agreements tied to the transfer of the policy. For example, if two shareholders in a closely held business take out life insurance policies on themselves and name each other as beneficiaries, the transfer-for-value rule applies. In this case, the receipt of consideration is established through their agreement to name each other as beneficiaries.

The transfer-for-value rule applies to transfers between family members in some cases, although these transfers may be classified as gifts. Additionally, there are exceptions to the rule that allow corporations and other policy owners to move their policies under specific circumstances. Policyowners who are unsure whether their policy transfer may result in taxation should consult their life insurance carrier or a tax advisor.

Furthermore, the taxation of policy transfers is not limited to life insurance. Transfer taxes are commonly imposed on the transfer of ownership or title to property, including real estate. These taxes are typically levied by state, county, or municipal authorities and are based on the value of the property being transferred. While the seller is usually liable for the real estate transfer tax, there may be agreements for the buyer to pay or cases where the buyer is responsible if the seller is exempt.

Insurance Adjusters and Sunday Calls: An Industry Norm?

You may want to see also

Frequently asked questions

Usually, beneficiaries do not pay taxes on life insurance payouts, which are typically not considered taxable income. However, there are some situations where taxes may be incurred, such as when the payout is made in installments rather than as a lump sum, or when the beneficiary is a minor.

If a life insurance policy has grown in value, the IRS may get involved, potentially triggering taxes.

Yes, if the beneficiary elects to delay the benefit payout and the money is held by the life insurance company for a given period, taxes may be incurred on the interest generated during that time.

Policyholders can generally borrow or withdraw money from the policy's cash value tax-free, as long as they do not take out more than they have paid in. However, certain tax advantages may no longer apply if too much money is put into the policy during its first seven years or within seven years of a "material change".