Life insurance is a financial product that provides peace of mind to those with financial dependents. While its primary role is to protect your loved ones in the event of your death, life insurance can also be used as a savings vehicle. Permanent life insurance policies, including whole life insurance and universal life insurance, offer a death benefit and a cash value component, which can be used for various purposes while the policyholder is still alive. This cash value grows over time, either by earning interest or by accruing gains from subaccounts or other investment vehicles. The rate of return and the level of risk depend on the type of policy chosen. Whole life insurance, for example, offers a fixed interest rate, while universal life insurance policies may offer a variable rate depending on the performance of the funds within the policy's subaccounts. It's important to note that the cash value component of life insurance policies may not offer the same high returns as other investment options, and the premiums for permanent life insurance tend to be much higher than those for term life insurance.

Explore related products

What You'll Learn

![]()

Whole life insurance interest rates

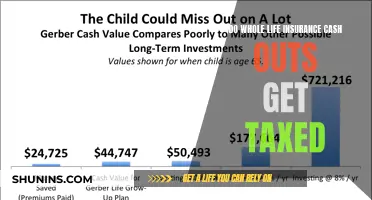

Whole life insurance is a type of permanent life insurance that offers lifelong coverage and a guaranteed death benefit as long as premiums are paid. It combines life insurance with an investment component, allowing policyholders to build cash value over time. This cash value can be borrowed against, but it is important to note that the interest rate may not be as high as other investment options.

The actual interest rate offered by insurance companies may vary, and it is essential to review the terms and conditions of the policy before purchasing. The rate of return within a whole life insurance policy can be influenced by various factors, including the length of the policy, the cost and amount of coverage, the terms of the contract, and the insurance company itself.

It is worth noting that whole life insurance policies are generally more expensive than term life insurance policies due to the permanent coverage and guaranteed payout. However, the interest rate on the cash value component may not be as competitive as other investment options available in the market.

Overall, whole life insurance interest rates provide a stable and guaranteed return on the cash value component of the policy, but it may not be the most lucrative investment option available. The interest rate offered will depend on several factors, and it is crucial to carefully review the policy details before making a decision.

Life Insurance: Banks and Your Options

You may want to see also

Explore related products

![]()

Universal life insurance

The cash value component of universal life insurance functions similarly to a savings account, with interest accruing daily. Policyholders can borrow against the cash value or withdraw it, usually without tax implications, though some withdrawals may be taxed. The interest rate on the cash value is set by the insurer and can change frequently, though there is typically a minimum rate guaranteed. This interest rate may be based on the current market rate or the policy's minimum rate, depending on which is higher.

However, universal life insurance carries some risks. If the cash value falls too low, the policy may lapse or require large premium payments to remain active. Additionally, if interest rates drop, the cash value may not perform as well as expected. It is important to carefully manage the policy and monitor the cash value to avoid these potential issues.

Cancer Patients: Finding Life Insurance Options

You may want to see also

Explore related products

![]()

Term life insurance

- Level term life insurance is the most common type, where the death benefit remains the same throughout the policy's term.

- Decreasing term life insurance is a renewable policy with coverage that decreases over the life of the policy at a predetermined rate.

- Convertible term life insurance allows policyholders to convert their term policy into permanent insurance.

- Renewable term life insurance provides a quote for the first year, with premiums increasing annually upon renewal, making it the least expensive option in the initial year.

While term life insurance does not directly earn interest, insurance companies are required by law to maintain a cash reserve against their obligation to pay death claims. They do this by investing the insurance premiums from policyholders in a conservative portfolio of stocks, bonds, cash equivalents, and treasuries. The growth of this cash reserve, along with new contributions from policyholders, drives interest rate and dividend growth for life insurance policy owners. However, the interest and dividends earned on these reserves are typically not forwarded to term life policyholders by stock companies. On the other hand, some mutual company term policies are eligible for dividends, which are usually credited as a discounted premium for the investor.

Liquidity in Life Insurance: Understanding Cash Value and Options

You may want to see also

Explore related products

![]()

Cash value life insurance

Universal life insurance is similar to whole life insurance, but with one key difference. Many universal life insurance plans allow you to change the value of premium payments, giving you more adjustability. With universal life insurance, you can scale the death benefit up or down depending on your unique circumstances. The cash value of a universal life insurance policy can be used to pay for the premiums or other expenses as needed.

There are also variable and indexed life insurance policies that can build cash value. Variable life insurance provides greater access to investment tools, like cash value. This type of plan tends to involve more risk, as the cash value will grow or diminish depending on how the investments perform. Indexed life insurance has a greater relationship with the stock market, as this is used to determine growth.

The cash value portion of a life insurance plan can be particularly appealing because you may be able to access the money early. You can do this by taking out a loan against the policy, surrendering the policy, or making a withdrawal.

The cash value in permanent life insurance policies can generate impressive returns, but it also comes with risks. Cash value policies tend to have higher premiums than term life insurance. Managing policies often requires a hands-on approach, and unpaid loans can reduce the death benefit paid to your beneficiaries.

Who Gets the Life Insurance Payout?

You may want to see also

Explore related products

![]()

Permanent life insurance

There are two main types of permanent life insurance: whole life insurance and universal life insurance. Whole life insurance offers fixed premiums, guaranteed cash value growth, and a guaranteed death benefit. The premiums are set at a level that guarantees a buildup of cash reserves, which will eventually equal the death benefit. Whole life policies generally guarantee a modest minimum interest rate and may also pay dividends to policyholders, further increasing the cash value.

Universal life insurance, on the other hand, offers more flexibility. Premium payments can be adjusted over time, and the death benefit amount may be changed. The cash value in a universal life policy grows at a variable interest rate and may be influenced by the performance of investments. This can lead to faster growth but also carries more risk.

Variable universal life insurance and indexed universal life insurance are two variations of universal life insurance that offer additional flexibility in how the cash value is managed. Variable universal life insurance allows policyholders to invest their cash value in sub-accounts tied to the market, offering the potential for higher growth but also the risk of decline in value. Indexed universal life insurance ties the growth of the cash value to the performance of a chosen stock market index, with a minimum guaranteed rate of growth.

Felons Selling Life Insurance: Is It Possible?

You may want to see also

Frequently asked questions

Life insurance is a policy that pays out a sum of money to your beneficiaries after you die.

Whole life insurance provides permanent coverage that accumulates a cash value. When you pay your premium, the insurer invests a portion to give your policy a cash value. The cash value grows over time at a fixed rate guaranteed by your insurer.

Term life insurance offers temporary coverage, while whole life insurance offers permanent coverage. Whole life insurance policies are generally more expensive than term life insurance policies.

Whole life insurance offers guaranteed returns and can supplement retirement income. It can also offer peace of mind to anyone with lifelong financial dependents.

Whole life insurance is expensive and not suitable for most people. The cash value is slow to grow and the rate of return can be low.