When considering health insurance through the marketplace, it’s important to factor in your estimated income for the upcoming year, as this directly impacts your eligibility for premium tax credits and cost-sharing reductions. The health insurance marketplace uses your projected annual income to determine whether you qualify for financial assistance, which can significantly lower your monthly premiums and out-of-pocket costs. Accurately estimating your income for the next year is crucial, as underestimating could result in higher premiums, while overestimating might mean missing out on potential savings. Factors such as job changes, bonuses, or other income fluctuations should be carefully considered to ensure you select the most appropriate plan and maximize available subsidies.

| Characteristics | Values |

|---|---|

| Income Projection | Yes, the Health Insurance Marketplace requires an estimate of next year's income for plan eligibility and subsidy calculations. |

| Purpose of Income Estimation | Determines eligibility for premium tax credits and cost-sharing reductions. |

| Accuracy Requirement | Best estimate based on current information; intentional over/underestimation may result in financial penalties or loss of subsidies. |

| Income Sources Considered | Wages, self-employment income, unemployment benefits, Social Security, pensions, alimony, and other taxable/non-taxable income. |

| Life Changes to Report | Job changes, marriage/divorce, birth/adoption, or other income fluctuations must be updated during the year. |

| Verification Process | Income estimates may be cross-checked with IRS data or require documentation during tax filing. |

| Impact of Underestimation | May owe repayment of excess subsidies when filing taxes. |

| Impact of Overestimation | May receive lower subsidies upfront but can claim the difference as a tax credit. |

| Open Enrollment Period | Typically November 1 to January 15 (varies by state); income estimates are finalized during this period. |

| Special Enrollment Period (SEP) | Allows income updates if qualifying life events occur outside open enrollment. |

| State-Based Marketplaces | Some states may have additional rules or variations in income projection requirements. |

| 2024 Updates | No major changes to income projection rules as of the latest data (October 2023). |

Explore related products

What You'll Learn

- Income Estimation Methods: How to accurately predict next year’s income for health insurance marketplace applications

- Income Fluctuations Impact: How changes in income affect health insurance premiums and coverage eligibility

- Reporting Income Changes: Steps to update income information if it changes during the coverage year

- Tax Credits and Income: How estimated income influences eligibility for premium tax credits

- Income Verification Process: What documents are required to verify income for health insurance marketplace plans

![]()

Income Estimation Methods: How to accurately predict next year’s income for health insurance marketplace applications

Accurate income estimation is crucial when applying for health insurance through the marketplace, as it directly impacts your eligibility for subsidies and the cost of your premiums. Predicting next year’s income may seem daunting, but several methods can help you make an informed estimate. Start by reviewing your current income sources, including wages, self-employment earnings, investments, and any anticipated changes. For example, if you’re expecting a raise, bonus, or promotion, factor these into your projection. Conversely, if you plan to reduce work hours or retire, adjust your estimate downward. Consistency in tracking income throughout the year can provide a solid foundation for your prediction.

One effective method is the historical trend analysis, which involves examining your income patterns over the past 2–3 years. Identify seasonal fluctuations, bonuses, or irregular earnings and use these trends to forecast next year’s income. For instance, if you consistently earn 10% more in the fourth quarter due to holiday work, include this in your estimate. Self-employed individuals should pay particular attention to client contracts, project pipelines, and industry trends to anticipate future earnings. Tools like tax returns, bank statements, and payroll records can serve as valuable data points for this analysis.

Another approach is the scenario planning method, where you create multiple income projections based on best-case, worst-case, and most likely scenarios. For example, if you’re in a commission-based job, estimate your income assuming high, average, and low sales performance. This method accounts for uncertainty and helps you prepare for different financial outcomes. It’s especially useful for individuals with variable income, such as freelancers or gig workers. By averaging these scenarios, you can arrive at a more balanced and realistic estimate for your health insurance application.

For those with stable, predictable income, a straightforward extrapolation method works best. Multiply your current monthly income by 12, then adjust for known changes like cost-of-living increases or scheduled pay raises. For instance, if you earn $4,000 per month and expect a 3% raise, your estimated annual income would be $48,480. This method is ideal for salaried employees with minimal income variability. However, always include additional sources like rental income, alimony, or retirement distributions to ensure accuracy.

Lastly, consider consulting a financial advisor or tax professional for complex income situations. They can help you navigate factors like business income, capital gains, or anticipated life changes (e.g., marriage, divorce, or starting a business). Their expertise can ensure your estimate aligns with IRS guidelines and marketplace requirements. Remember, overestimating or underestimating income can lead to unexpected tax liabilities or subsidy repayments, so precision is key.

In conclusion, accurate income estimation for health insurance marketplace applications requires a combination of historical data, forward-looking analysis, and practical adjustments. By employing these methods, you can confidently predict next year’s income and secure the appropriate coverage at the right cost. Always review your estimate periodically and update it if your financial situation changes significantly.

Who Oversees Insurance Accountability in Texas? A Comprehensive Guide

You may want to see also

Explore related products

![]()

Income Fluctuations Impact: How changes in income affect health insurance premiums and coverage eligibility

Income fluctuations can significantly alter your health insurance landscape, impacting both premiums and eligibility for certain plans. Imagine a freelancer whose income varies monthly. During a lucrative quarter, they might fall into a higher income bracket, potentially disqualifying them from subsidies that make marketplace plans affordable. Conversely, a sudden drop in income could open doors to cost-saving programs like Medicaid. This dynamic underscores the importance of understanding how income changes ripple through the health insurance marketplace.

For instance, let's consider a single individual earning $40,000 annually. They qualify for a premium tax credit, reducing their monthly premium significantly. However, if their income surges to $55,000 mid-year due to a promotion, they might exceed the income threshold for subsidies, leading to a higher premium burden. Conversely, a job loss resulting in an income drop to $30,000 could make them eligible for Medicaid, offering comprehensive coverage at little to no cost.

The health insurance marketplace operates on a system of income-based subsidies. These subsidies, in the form of premium tax credits and cost-sharing reductions, are designed to make health insurance more affordable for individuals and families with moderate incomes. However, these subsidies are calculated based on your estimated income for the upcoming year. This is where the challenge lies – predicting your income with accuracy can be difficult, especially for those with variable incomes.

Overestimating your income could lead to receiving less subsidy than you're entitled to, resulting in higher out-of-pocket costs. Conversely, underestimating your income might result in receiving more subsidy than warranted, which would need to be repaid when you file your taxes. This highlights the need for careful income projection and regular updates to your marketplace application if your income situation changes.

To navigate this complexity, consider these practical tips:

- Estimate conservatively: If your income fluctuates, err on the side of caution when estimating your income for the year. This minimizes the risk of subsidy repayment.

- Report changes promptly: Notify the marketplace of any significant income changes throughout the year. This ensures your subsidies are adjusted accordingly, preventing unexpected costs.

- Explore all options: Don't solely focus on marketplace plans. If your income drops, investigate Medicaid eligibility. Conversely, if your income rises, consider private insurance options that might offer more comprehensive coverage.

- Seek professional guidance: Consulting a certified insurance navigator or broker can provide valuable insights and help you make informed decisions based on your unique circumstances.

Strategies to Overcome Health Insurance Denials for Treatment Approval

You may want to see also

Explore related products

![]()

Reporting Income Changes: Steps to update income information if it changes during the coverage year

Income fluctuations during your health insurance coverage year can significantly impact your premium tax credits and cost-sharing reductions. Failing to report these changes promptly may result in owing money at tax time or missing out on financial assistance you’re entitled to. The Health Insurance Marketplace requires you to update your income information within 30 days of any change to ensure your subsidies remain accurate. This proactive approach not only keeps you compliant but also helps you avoid unexpected financial burdens.

To update your income information, log in to your Healthcare.gov account or contact the Marketplace Call Center. Navigate to the "Report a Life Change" section and select "Income Change." You’ll need to provide details about the nature of the change, such as a new job, raise, or loss of income. Be prepared to submit supporting documents, like pay stubs or unemployment records, to verify the update. Accuracy is key—double-check all figures before submitting to prevent processing delays or errors.

One common pitfall is underestimating the impact of sporadic income changes, such as bonuses or freelance earnings. For instance, a $5,000 year-end bonus could push your annual income into a higher tax bracket, reducing your eligibility for subsidies. Conversely, a sudden job loss might qualify you for additional assistance. The Marketplace uses your estimated annual income to calculate subsidies, so report changes as soon as they occur to reflect your current financial situation accurately.

If you’re unsure how to estimate your income for the year, consider using the Marketplace’s estimation tool or consulting a tax professional. For example, if you’re self-employed, track your monthly earnings and expenses to project an annual figure. Keep in mind that overestimating your income won’t penalize you, but underestimating could lead to repaying excess subsidies. Regularly reviewing and updating your income ensures you receive the correct level of financial assistance throughout the year.

Finally, remember that reporting income changes isn’t just about compliance—it’s about maximizing your benefits. For instance, a family of four earning $40,000 annually might qualify for substantial premium tax credits, but a $10,000 increase in income could reduce their subsidy. By promptly updating their information, they can adjust their monthly premiums and avoid a large repayment at tax time. Stay vigilant, act quickly, and leverage the Marketplace’s tools to maintain affordable coverage tailored to your evolving financial circumstances.

Virginia Medical Insurance: Anytime Access and Availability

You may want to see also

Explore related products

![]()

Tax Credits and Income: How estimated income influences eligibility for premium tax credits

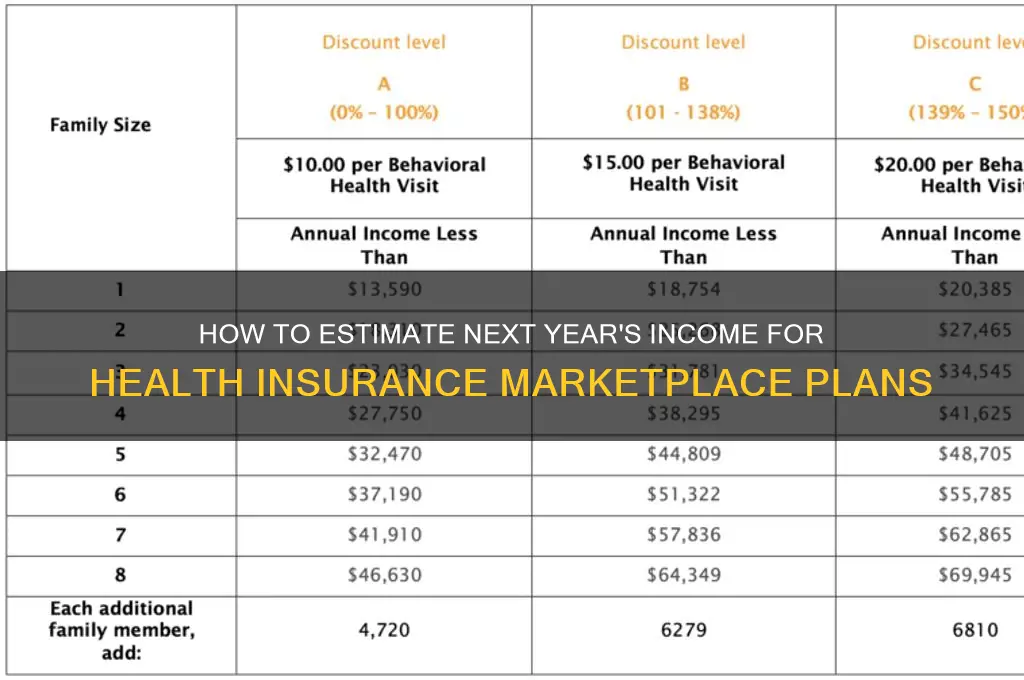

Estimating your income for the upcoming year is a critical step when applying for health insurance through the Marketplace, as it directly impacts your eligibility for premium tax credits. These credits, designed to reduce your monthly insurance premiums, are calculated based on a percentage of the federal poverty level (FPL). For 2023, individuals earning between 100% and 400% of the FPL qualify for subsidies, with the exact amount tapering off as income rises. For example, a single individual earning $20,000 annually (approximately 167% of the FPL) could receive a substantial subsidy, while someone earning $54,000 (around 433% of the FPL) would likely receive none. Accurately projecting your income ensures you neither overestimate and miss out on savings nor underestimate and face repayment at tax time.

To estimate your income effectively, consider all sources of revenue, including wages, self-employment earnings, unemployment benefits, and investment income. Seasonal workers or those with fluctuating income should average earnings over the past few years to create a realistic projection. For instance, a freelance graphic designer might review their income from the past three years, factoring in slow and busy seasons, to arrive at a conservative estimate. Tools like the Marketplace’s income estimator can assist, but manual calculations using pay stubs, tax returns, and anticipated changes (e.g., a new job or reduced hours) are equally valuable.

One common pitfall is failing to account for life changes that could alter income. Marriage, divorce, job loss, or a new business venture can significantly shift your financial landscape. For example, a couple planning to marry mid-year should combine their projected incomes to assess eligibility. Similarly, someone retiring in the coming year should exclude future pension income if it hasn’t yet begun. Ignoring these adjustments could lead to incorrect subsidy amounts and unexpected costs.

If your actual income deviates from your estimate, the IRS will reconcile the difference during tax season. Underestimating income may result in repaying excess credits, while overestimating could mean missing out on additional subsidies. To mitigate this, update your income information through the Marketplace whenever significant changes occur. For instance, if you receive a raise or lose a side job, promptly report these changes to ensure your premium tax credits remain accurate.

In summary, estimating your income for the next year is both an art and a science, requiring careful consideration of past earnings, anticipated changes, and potential life events. By taking a methodical approach, you can maximize your eligibility for premium tax credits while avoiding financial surprises. Whether you’re a salaried employee, self-employed, or navigating income fluctuations, precision in your estimate ensures you receive the appropriate level of assistance for your health insurance needs.

Mastering Insurance Company Interviews: Key Questions and Winning Strategies

You may want to see also

Explore related products

$9.99

![]()

Income Verification Process: What documents are required to verify income for health insurance marketplace plans

The income verification process is a critical step in determining eligibility for health insurance marketplace plans, particularly for subsidies like the Advanced Premium Tax Credit (APTC). To ensure accuracy, the marketplace requires specific documents that reflect your current and, in some cases, projected income for the upcoming year. This process is not just a formality; it directly impacts the affordability of your health coverage.

Documents for Current Income Verification

For most applicants, verifying current income involves submitting recent pay stubs, tax returns, or employer-issued forms like W-2s. Self-employed individuals may need profit and loss statements or 1099 forms. If you receive income from sources like Social Security, unemployment benefits, or alimony, official letters or statements from the issuing agency are typically required. The key is to provide clear, up-to-date evidence of all income streams to avoid discrepancies that could delay approval or result in incorrect subsidy amounts.

Projecting Next Year’s Income

When factoring in income for the next year, the marketplace may ask for additional documentation if your income is expected to change significantly. This could include job offer letters, contracts, or written estimates from employers. For self-employed individuals, projected income statements or business forecasts may be necessary. While not always required, providing these documents can help ensure your subsidy aligns with your actual financial situation, preventing potential repayment obligations if your income is overestimated.

Special Considerations and Tips

If your income fluctuates or is difficult to predict, consider submitting a detailed explanation or working with a marketplace navigator. Keep copies of all submitted documents for your records, and double-check that the information matches your application. For households with multiple income sources, organize documents by type and individual to streamline the verification process. Remember, accuracy is paramount—underestimating or overestimating income can lead to financial penalties or unexpected costs.

The income verification process for health insurance marketplace plans is designed to ensure fairness and accuracy in subsidy allocation. By gathering the right documents—whether pay stubs, tax forms, or projections for next year—you can navigate this process efficiently. Taking the time to prepare and submit thorough, accurate information not only secures your eligibility but also maximizes the affordability of your health coverage.

Is Scan Health Insurance Publicly Traded? Exploring Ownership and Market Status

You may want to see also

Frequently asked questions

Yes, the Health Insurance Marketplace uses your estimated income for the upcoming year to calculate eligibility for premium tax credits and other cost-saving programs. It’s important to provide an accurate estimate to avoid discrepancies later.

If your actual income differs significantly from your estimate, it may affect your eligibility for subsidies or the amount you owe. You may need to repay excess subsidies if you overestimated your income or receive additional credits if you underestimated.

To estimate your income, consider your expected wages, self-employment earnings, investments, and any other sources of income. Review your previous year’s income and factor in any anticipated changes, such as raises, job changes, or reduced hours.