The taxability of insurance settlements depends on the nature of the settlement proceeds and the claims being made in the lawsuit. Generally, money received as part of an insurance claim or settlement is not taxed, as the purpose of insurance is to make you whole, meaning you should only receive enough payment to bring you back to the state you were in before an incident occurred. However, some types of payouts resulting from a legal settlement are taxable, whether the case is settled in or out of court. For example, punitive damages are taxable, while compensation for medical bills is not. When it comes to medical insurance settlements, it is important to note that any medical claim, whether part of a settlement after an accident or a claim for a medical appointment, is typically not taxed. If you do receive a taxable payment from a lawsuit, you will likely be required to file a Form 1099 when reporting your income to the IRS.

| Characteristics | Values |

|---|---|

| Do you get a 1099 for a medical insurance settlement? | You will not receive a 1099 form for a medical insurance settlement because it is not taxed. However, if you receive taxable payment from a lawsuit, you will likely receive a 1099 form. |

| When do you receive a 1099 form? | You will receive a 1099 form when you receive taxable payment from a lawsuit. |

| What is a 1099 form? | A 1099 form is used to report certain miscellaneous income for each person you have paid during the year. |

| What are the exceptions to getting a 1099 form? | If the settlement qualifies for one of the tax exceptions, you may not receive a 1099 form. For example, if the settlement is for personal physical injuries or physical sickness, you should not receive a 1099 form. |

| What are the different types of 1099 forms? | There are different types of 1099 forms, including Form 1099-MISC and Form 1099. Form 1099-MISC is used to report miscellaneous income, such as medical and healthcare payments, rents, royalties, prizes, and awards. |

| What are the tax implications of settlements? | The general rule is that all income is taxable unless specifically exempted. However, there are exceptions, such as amounts paid for certain discrimination claims and physical injuries. |

| How do you avoid getting a 1099 form? | You can include a "no-1099" provision in your settlement agreement stating that the defendant agrees not to send a 1099 form to the plaintiff. |

| What are the tax implications of insurance settlements? | Money received as part of an insurance claim or settlement is typically not taxed because it is meant to "make you whole" and bring you back to your previous state. However, income from certain types of claims and insurance-related events may still be taxable. |

| What are the tax implications of life insurance payouts? | Life insurance payouts are generally not taxed as income, but they may be subject to estate taxes depending on the size of the insured's estate. Any interest gained from a life insurance payout or withdrawal from a cash-value life insurance policy is counted as income and taxed accordingly. |

Explore related products

What You'll Learn

![]()

Medical insurance settlements are typically not taxed

Generally, medical insurance settlements are not taxed. The IRS only levies taxes on income, which is money or payment received that results in you having more wealth than you did before. Because the purpose of insurance is to "make you whole", you should only receive enough payment to bring you back to the state you were in before an incident occurred. For example, if you're in a car accident and incur $500 in medical expenses, your personal injury protection (PIP) coverage will reimburse you. But since the $500 is only reimbursing you for money you previously spent, it’s not taxed. When you're making a health insurance claim, it's likely that you won't touch any money at all because health insurance companies most commonly pay doctors directly.

However, there are some exceptions. If the settlement includes punitive damages or interest, those portions may be subject to taxation. For example, if someone hits you in a car accident, you won't be taxed for a payment you receive for your medical bills. However, if the judge also awards you punitive damages, you will have to pay tax on those. In addition, any interest gained from a life insurance payout, or any money you withdraw from a cash-value life insurance policy while the insured person is still alive, is counted as income and taxed as such.

The taxation of insurance settlements also varies by state. Generally, settlements for personal injury are exempt from state taxes, just like federal taxes. However, portions of the settlement for things like emotional distress, punitive damages, or interest earned might be subject to state taxes depending on the state’s tax laws. It’s important to consult with a tax professional or local tax authority to determine your specific obligations.

If you do have to pay taxes on an insurance claim, you'll receive a 1099 form to help you file. However, defendants or their insurers will often send plaintiffs a 1099, even though the underlying claim is for personal physical injuries (and therefore should not be sent a 1099). To avoid this, plaintiff attorneys should include a "no-1099" provision in the settlement agreement stating that the defendant agrees not to send a 1099 to the plaintiff.

Life, Medical Insurance: Schedule C Claims Explained

You may want to see also

Explore related products

![]()

Medical claim reimbursements are not taxed

In general, money received as part of an insurance claim or settlement is not taxed. This is because the purpose of insurance is to "make you whole", meaning that you should only receive enough payment to bring you back to the state you were in before an incident occurred. For example, if you are in a car accident and incur $500 in medical expenses, your personal injury protection (PIP) coverage will reimburse you, but since the $500 is only reimbursing you for money you previously spent, it is not taxed.

However, it is important to note that there are some exceptions to this rule. If you receive a taxable payment from a lawsuit, you will likely receive a 1099 form to use when filing your taxes. This includes punitive damages awarded by a judge. Additionally, defendants or their insurers may send plaintiffs a 1099 form, even though the underlying claim is for personal physical injuries and should not be taxed. To avoid this, plaintiff attorneys should include a "no-1099" provision in the settlement agreement, stating that the defendant agrees not to send a 1099 to the plaintiff.

It is also worth noting that while medical claim reimbursements are not taxed, other types of insurance payouts may be subject to taxes. For example, life insurance payouts may be subject to estate taxes, depending on the size of the insured's estate and the state in which the insured and beneficiaries live. Additionally, any interest gained from a life insurance payout or any money withdrawn from a cash-value life insurance policy while the insured person is still alive is counted as income and taxed accordingly.

In terms of tax deductions, there are certain medical and dental expenses that you may be able to deduct if they exceed a certain percentage of your adjusted gross income (AGI). These include unreimbursed expenses for preventative care, treatment, surgeries, dental and vision care, visits to psychologists and psychiatrists, prescription medications, and appliances such as glasses, contacts, false teeth, and hearing aids. Transportation costs to and from medical care may also be deductible, as well as certain health insurance costs for self-employed individuals. It is important to note that expenses paid using money from a flexible spending account or health savings account are not deductible because the money in those accounts is already tax-advantaged.

Understanding Medical Insurance: Coverage, Benefits, and Claims

You may want to see also

Explore related products

![]()

Life insurance payouts are not taxed as income

Generally, life insurance payouts are not taxed as income. However, there are some exceptions to this rule. For instance, if you are the policyholder and you cancel a whole life or universal life insurance policy, you will receive the cash surrender value, which is the policy's cash value minus any fees. While you don't have to pay taxes on the principal amount, any cash value the policy has accrued will be taxed as income. Additionally, if you receive the proceeds in installments, this may also expose you to tax liability.

Moreover, any interest gained from a life insurance payout or any money withdrawn from a cash-value life insurance policy while the insured person is still alive is considered income and is taxed accordingly. This interest income is reported using Form 1099-INT or Form 1099-R. On the other hand, if you are the beneficiary of a life insurance policy, the payout, known as a death benefit, is typically exempt from income tax. However, if the payout exceeds the total amount of premiums paid, the excess amount may be taxed.

It is important to note that life insurance payouts may be subject to estate taxes, depending on the size of the insured's estate. Additionally, the state where the insured and beneficiaries reside may impose an estate or inheritance tax. While medical insurance settlements are typically not taxed, punitive damages awarded in a lawsuit are taxable, and you will likely receive a 1099 form in this case.

To summarise, while life insurance payouts are generally not taxed as income, there are specific circumstances, such as interest gains, withdrawals from certain policies, and installment payments, that may result in tax liability. Additionally, life insurance payouts may be subject to estate or inheritance taxes in certain states. Understanding the specific details of your situation is crucial for determining the tax implications of a life insurance payout.

Divorced Parents: Medical Insurance Options and Challenges

You may want to see also

Explore related products

![]()

Defendants or their insurers must issue a 1099 to the plaintiff

When it comes to the tax implications of settlements, the general rule is that all income is taxable, as outlined in Internal Revenue Code (IRC) Section 61. However, there are exceptions, and not all amounts received from a settlement are subject to tax. The purpose of the settlement payment must be considered to determine if it is taxable. For example, amounts paid for certain discrimination claims and physical injuries are typically not taxed.

In the context of defendants or their insurers issuing a 1099 to the plaintiff, it is important to understand the circumstances. Firstly, defendants or their insurers are generally required to issue a 1099 to the plaintiff when a settlement payment is made, unless the settlement qualifies for a tax exception. This is outlined in IRC Section 6041. The nature of the settlement and the claims being made in the lawsuit determine the specific reporting requirements.

It is worth noting that defendants or their insurers may sometimes send plaintiffs a 1099 even when the underlying claim is for personal physical injuries, which should not typically trigger a 1099. In such cases, plaintiff attorneys can include a "no-1099" provision in the settlement agreement, stating that the defendant agrees not to send a 1099 to the plaintiff. This provision ensures that the defendant or their insurer will not send a 1099, as it would violate the terms of the settlement agreement.

Additionally, if the settlement proceeds are jointly payable to the attorney and the plaintiff, the situation can be avoided by requesting a single check made out to the "Attorney in trust for Client." This way, the attorney can deposit the check into their client trust account and distribute the net settlement proceeds without issuing a 1099 to the client.

Furthermore, when it comes to insurance claims or settlements, it is important to understand that the IRS typically does not levy taxes on these payments because they are meant to make the recipient whole rather than increase their wealth. However, income from certain types of claims and insurance-related events may still be taxable, and a 1099 form may be required for reporting purposes.

Adding Your Newborn to Your Medical Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

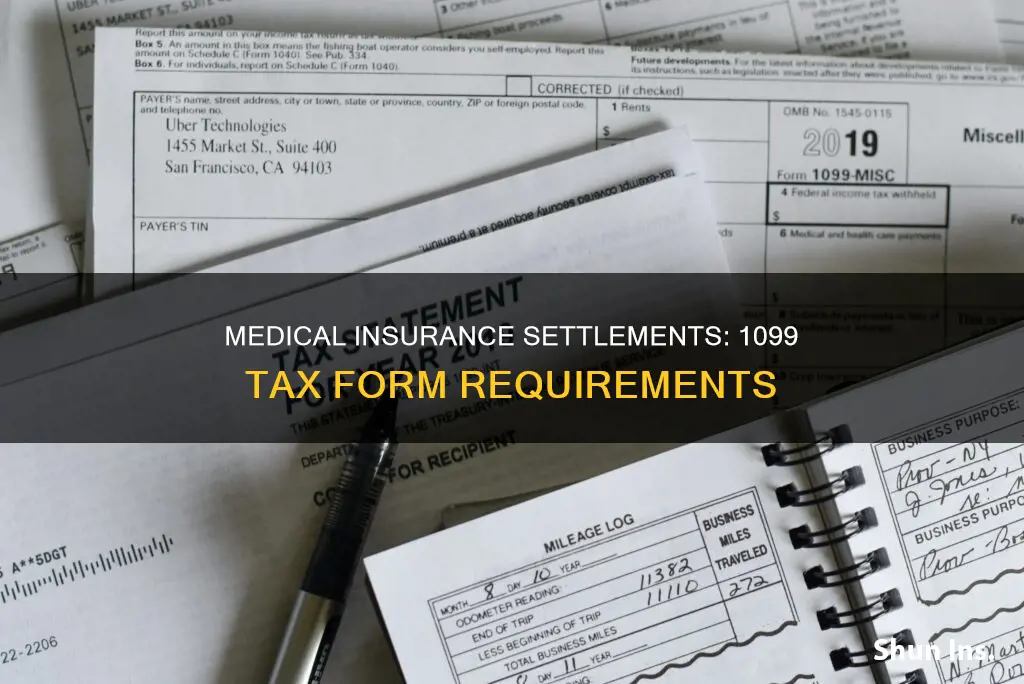

Form 1099-MISC is used to report certain miscellaneous income

Generally, money received as part of an insurance claim or settlement is not taxed. This is because the purpose of insurance is to "make you whole", meaning that the payment should only bring you back to your state before the incident. However, income from certain types of claims and insurance-related events may be taxable. For example, if you receive a payout for your medical bills after a car accident, this is not taxed. But if the judge also awards you punitive damages, you will have to pay tax on that amount.

If you receive a taxable payment from a lawsuit, you will likely receive a 1099 form to help you file your taxes. Form 1099-MISC is used to report certain types of miscellaneous compensation, including rent, royalties, prizes, awards, healthcare payments, and payments to an attorney. It is also used to report direct sales of at least $5,000 in consumer products to a buyer for resale anywhere other than a permanent retail establishment.

Form 1099-MISC is not used to report nonemployee compensation; instead, this is reported on Form 1099-NEC. Before 2020, Form 1099-MISC was used to report the income of non-employees, such as independent contractors, freelancers, sole proprietors, and self-employed individuals. A taxpayer will receive a Form 1099-MISC if they are paid at least $10 in royalties or $600 or more in other types of miscellaneous income during a calendar year.

The form has different box numbers for reporting various types of payments. For example, Box 1 is for rental income, Box 2 is for royalties, and Box 4 is for federal income tax withheld. It is important to note that you do not have to file Form 1099-MISC with your taxes, but you should keep it for your records.

Understanding Medicaid: Working Alongside Other Insurance Plans

You may want to see also

Frequently asked questions

Money received as part of an insurance claim or settlement is usually not taxed. However, income from certain types of claims and insurance-related events may be taxable.

Form 1099 is used to report certain miscellaneous income for each person you have paid during the year. This includes medical and healthcare payments.

If you receive a taxable payment from a lawsuit, you will likely receive a 1099 form to help you file your taxes. However, if your settlement qualifies for a tax exemption, you won't need to fill out a 1099 form.

Compensation for medical bills and property repair is typically non-taxable. Punitive damages, on the other hand, are taxable.

You can use a flexible spending account (FSA) or a health reimbursement arrangement (HRA) to pay for medical expenses. These are employer-sponsored benefit plans that can help you save on taxes.