Medicaid is a health insurance program that is jointly financed by the federal and state governments. While individuals do not pay taxes on their Medicaid insurance, states finance their share of the program through various sources, including taxes on healthcare providers and other entities. These taxes are subject to federal rules and oversight, with limits on the amount of revenue that can be generated through provider taxes. Eligibility for Medicaid is determined by income, with most states considering current monthly income, while some states may also need to take yearly income into account.

Explore related products

$30

$102.99 $99.99

What You'll Learn

![]()

Medicaid insurance and tax returns

Medicaid is a government-funded insurance program that provides free or low-cost health coverage to people with low incomes, including families and children, pregnant women, the elderly, and people with disabilities. Many states have expanded their Medicaid programs to cover all people below certain income levels.

Medicaid and Tax Returns:

If you are enrolled in a Marketplace plan with the premium tax credit, you must file a tax return. The premium tax credit is a tax credit that can be used to lower your monthly insurance payment. If you used more of the premium tax credit than you qualified for, you will owe taxes on the excess amount and will need to report it on your tax return by filing Form 8962, Premium Tax Credit. If you used less than you qualified for, you may be eligible for a refund or a reduction in the amount of tax you owe.

If you are enrolled in Medicaid, you will receive a Form 1095-B, Health Coverage, which provides information about your health insurance coverage. This form is not required to be included with your federal tax return, but you should keep it with your other tax documents. You will also need to answer questions about your health insurance coverage on your federal tax return to avoid being penalized. If you were covered by Medicaid for the entire year, you can simply answer "yes" to these questions.

In some states, there may be additional requirements to report health insurance coverage on your state tax return. It is important to review the specific requirements for your state.

Using Health Savings Accounts for Insurance Premiums: Is It Allowed?

You may want to see also

Explore related products

![]()

Premium tax credits

Premium Tax Credit

The Premium Tax Credit is a tax credit that helps eligible individuals and families afford health insurance purchased through the Health Insurance Marketplace. It lowers the out-of-pocket cost for your health insurance premiums. When you enrol, the Marketplace will determine if you are eligible for advance payments of the premium tax credit, also known as advance credit payments or APTC.

To be eligible for the premium tax credit, your household income must be at least 100 per cent and, for years other than 2021 and 2022, no more than 400 per cent of the federal poverty line for your family size. There are two exceptions for individuals with household incomes below 100 per cent of the applicable federal poverty line. The amount of the Premium Tax Credit is generally equal to the premium for the second lowest-cost silver plan available through the Marketplace that applies to the members of your coverage family, minus a certain percentage of your household income.

If you benefit from advance payments of the premium tax credit, it is important to report life changes to the Marketplace as they happen throughout the year. Certain changes to your household, income, or family size may affect the amount of your premium tax credit and, consequently, your tax refund.

If the advance credit payments made on your behalf are more than the allowed premium tax credit, you will have to repay some or all of the excess for any tax year other than 2020. For tax years other than 2021 and 2022, if your household income on your tax return is more than 400 per cent of the federal poverty line for your family size, you are not allowed a premium tax credit and will have to repay all of the advance credit payments.

Understanding OOP in Medical Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Modified adjusted gross income (MAGI)

MAGI is calculated by taking your gross income and then your AGI. Your gross income includes money earned from all sources, such as wages, tips, business income, alimony payments, investment income, capital gains, pensions, or rents. Your AGI is your gross income with certain allowable deductions subtracted, excluding standard or itemized deductions.

MAGI is then calculated by adding certain adjustments to your AGI. These adjustments can include foreign earned income, tax-exempt interest, and the tax-free portion of Social Security benefits. The specific adjustments added back to AGI to calculate MAGI will depend on the tax benefit in question. For example, when calculating eligibility for the Child Tax Credit, you would add back certain foreign income and tax-exempt interest to your AGI.

MAGI is used by the IRS to determine eligibility for specific tax programs and benefits. For instance, it helps determine the allowed amount of your Roth IRA contributions. Knowing your MAGI can also help you avoid tax penalties, as over-contributing to certain programs can trigger interest payments and fines. Additionally, your MAGI can determine eligibility for certain government programs, such as subsidized insurance plans available on the Health Insurance Marketplace.

Health Insurance Dependents: Who Can Authorize Medical Tests?

You may want to see also

Explore related products

![]()

State financing of Medicaid

Medicaid is a major source of financing for US states to provide health coverage and long-term care for low-income residents. It is jointly funded by states and the federal government through a federal matching program with no cap. The federal government pays a specified percentage of program expenditures, known as the Federal Medical Assistance Percentage (FMAP). The FMAP varies across states, for specific services, types of enrollees, and whether the costs are for medical care or program administration.

States must fund their share of Medicaid expenditures for the care and services available under their state plan. They can establish their own Medicaid provider payment rates within federal requirements and generally pay for services through fee-for-service or managed care arrangements. States that have implemented the Affordable Care Act (ACA) Medicaid expansion receive a 90% FMAP for adults covered. States that had not adopted the expansion as of 2021 when the American Rescue Plan Act was enacted are eligible for a 5% increase in the state’s traditional FMAP for two years if they implement the expansion. Administrative costs incurred by states are usually matched by the federal government at a 50% rate, but some functions, such as eligibility and enrollment systems, receive higher match rates.

Medicaid accounted for 30% of total state spending for all items in the state fiscal year 2023 budget. It accounted for 15% of expenditures from state funds and 57% of all expenditures from federal funds. States have an incentive to control Medicaid spending because they pay a share of the costs. However, research shows that federal matching dollars from Medicaid spending have positive effects on state economies. States that have adopted the ACA Medicaid expansion have realized budget savings, revenue gains, overall economic growth, and positive effects on the finances of hospitals and other healthcare providers.

Regarding the impact of Medicaid on taxes, individuals with Medicaid do not reimburse the government through their tax returns. However, in some states, there is a requirement to report health insurance coverage on tax returns.

HIV Medication: Insurance Coverage and Accessibility

You may want to see also

Explore related products

![]()

Federal requirements for state provider taxes

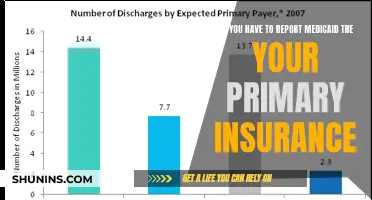

Medicaid is a joint federal-state program that provides comprehensive health care coverage for over 70 million people in the United States. The federal and state governments share the responsibility of financing the program. States pay health care providers and managed care organizations and report this spending to the Centers for Medicare & Medicaid Services (CMS) quarterly to receive federal reimbursement.

- Uniformity and broad-based: Federal law requires the tax to be broad-based and uniform, meaning states cannot pick and choose who to tax within a provider class. There are 19 classes of providers that the CMS uses to ensure that the tax programs are broad-based and uniform.

- Hold harmless requirement: States are prohibited from directly or indirectly guaranteeing that providers will receive their tax revenues back (i.e., be "held harmless"). This requirement does not apply when the tax revenues comprise 6% or less of net patient revenues from treating patients, a level sometimes referred to as a "safe harbor" limit.

- Waivers: States may receive waivers of the requirement that taxes be broad-based and uniform if the state can prove the net effect of the tax is "generally redistributive," and that the amount of tax is not directly related to Medicaid payments.

- Limits on revenue: There are limits on the amount of revenue that states can generate through provider taxes.

- Reporting: States must report their spending on health care providers and managed care organizations to the CMS quarterly to receive federal reimbursement.

Restricting the use of provider taxes or further limiting states' ability to impose taxes on health care providers would significantly cut state funding for Medicaid and create financing gaps for states. It would also put Medicaid expansion at serious risk in the states that have implemented it.

International Travel: Medical Insurance Coverage and Your Options

You may want to see also

Frequently asked questions

No, you do not reimburse the government with your tax return for having Medicaid. However, in some states, there is still a requirement to report health insurance coverage.

On your federal tax return, you need to answer the questions in the health insurance section under Federal Taxes so that you are not penalized. If you were covered all year, simply answer yes.

The Medicaid program is jointly financed by the federal and state governments. States finance the non-federal share of Medicaid spending through various sources, including general fund revenue and taxes on healthcare providers.