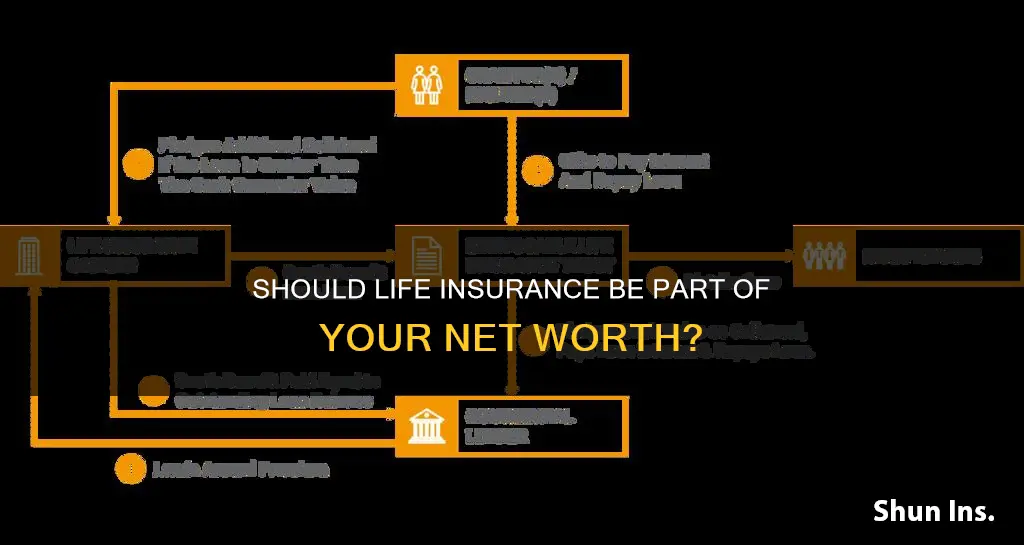

Life insurance is a necessity for most people, but it can also be an asset that adds to your net worth. The primary purpose of life insurance is to provide financial stability for beneficiaries after the policyholder's death. However, certain types of life insurance policies, such as whole life insurance, can accumulate cash value over time, which is considered an asset. This cash value can be accessed during the policyholder's lifetime, providing additional financial stability and flexibility. While term life insurance does not build cash value and is not considered an asset, it can still be a valuable tool for protecting your family's financial future. Understanding the differences between these types of life insurance policies is essential when deciding whether to include life insurance in your net worth calculations.

| Characteristics | Values |

|---|---|

| Is life insurance considered an asset? | Only some types of life insurance are classified as an asset. |

| What types of life insurance are considered an asset? | Whole life insurance and other types of permanent life insurance with a cash value component are considered assets. |

| Why are these types of life insurance considered an asset? | You can withdraw funds from your policy while you’re alive. |

| What types of life insurance are not considered an asset? | Term life insurance is not considered an asset because you can’t get value from it when you’re alive. |

| When might term life insurance be considered an asset? | In rare cases, proceeds from a term life policy might become an asset if you sell the policy for a profit or if your assets total $13.61 million or more. |

| What is the main benefit of life insurance? | The primary goal of life insurance is to provide financial stability for your family and/or your beneficiaries after you are gone through a lump-sum payment. |

| How does life insurance add to your net worth? | Life insurance can help increase your net worth by providing a death benefit, acting as a retirement savings tool, and assisting in debt repayment. |

Explore related products

What You'll Learn

![]()

Term life insurance is not an asset

Term life insurance is not considered an asset because it does not have a cash value component. In other words, you can't benefit financially from your policy while you're alive. Term life insurance is designed to provide coverage for a set period, usually 10 to 30 years, and if you live longer than the policy lasts, you won't receive any money. This is in contrast to whole life insurance or other types of permanent life insurance, which accumulate cash value and allow you to withdraw funds while you're alive, making them assets.

The main benefit of term life insurance is the death benefit it provides to your beneficiaries in the event of your death. This death benefit is not considered an asset because it is not something you own that has economic value while you are alive. Instead, it is a form of protection that ensures your family doesn't suffer financially if you die. While this benefit is invaluable to your loved ones, it does not contribute positively to your finances and, therefore, does not meet the definition of an asset.

The distinction between term and whole life insurance as assets is important, especially during divorce proceedings or mortgage underwriting. Whole life insurance, with its cash value component, is considered an asset and must be listed as such when dividing property during a divorce. Term life insurance, on the other hand, is not relevant in these proceedings as it does not have a cash value.

Although term life insurance is not an asset, it still plays a crucial role in financial planning. By providing temporary coverage at a lower cost than permanent life insurance, it offers peace of mind and ensures your family's financial stability in the event of your untimely death. Additionally, term life insurance can protect your assets by ensuring that your beneficiaries receive the full death benefit, which can then become a liquid asset for them.

In rare cases, proceeds from a term life insurance policy might become an asset. For example, if you sell the policy for a profit, any earnings would be subject to income tax and could be considered an asset. Similarly, if your total assets exceed a certain threshold, your beneficiaries may need to pay an estate or gift tax on the inherited assets, including any life insurance proceeds.

Life Insurance Denial: Overweight and Uninsured?

You may want to see also

Explore related products

![]()

Whole life insurance is an asset

Whether or not life insurance is considered an asset depends on the type of policy and whether you can benefit financially from the policy while you are alive. Whole life insurance is considered an asset because it is a form of permanent life insurance with a cash value component.

The cash value component in whole life insurance can grow tax-deferred, providing additional tax benefits. It is also a strategic tool for wealth building and personal finance beyond just its death benefit. The guaranteed cash value growth offers a stable, non-correlated asset, providing a hedge against market risk and volatility.

When considering assets, it is important to distinguish between tangible and intangible assets. Tangible assets are those that can be touched, such as real estate, precious metals, and commodities. Intangible assets, on the other hand, cannot be touched and include things like use rights for land, air, and water. Whole life insurance falls into the category of intangible assets as it is not something that can be physically touched.

In summary, whole life insurance is considered an asset because it provides a financial benefit to the policyholder while they are alive, through the ability to withdraw funds from the policy's cash value. It also offers tax advantages and can be a valuable tool for wealth building and financial protection.

Life Insurance and Credit Reports: What's the Connection?

You may want to see also

Explore related products

![]()

Life insurance as a retirement savings tool

Life insurance can be a valuable tool for retirement planning if your situation allows for it. Life Insurance Retirement Plans (LIRPs) are essentially over-funded policies, with amounts above the premiums required to keep the policy active. The goal is to maximize the cash value for future loans. You fund a universal or whole life insurance policy and borrow against the accumulating cash value by taking out a tax-free loan.

LIRPs offer several benefits, including tax-deferred accumulation, asset protection, and penalty- and tax-free distributions. Because life insurance is taxed on a "first-in, first-out" basis, this tax-free "loan" can be made up to the basis, or whatever you have already put in. Each year, it will accumulate interest, and your account value will grow.

However, LIRPs may not be suitable for everyone and should not replace other retirement savings plans such as 401(k)s or IRAs. It is recommended to prioritize maxing out contributions to these plans first, as employers often match contributions up to a certain limit, which is essentially free money. LIRPs can be a good alternative for those who have already maxed out their tax-advantaged retirement savings plans or for high-net-worth individuals who require higher contribution limits.

Additionally, life insurance policies tend to have significant upfront costs, including initial fees that can eat up half of the first year's premiums, steep investment fees, and surrender charges if the policy lapses within the first few years. As a result, it can take up to ten years for the policy to break even. Therefore, life insurance as a retirement savings tool is most beneficial for wealthier individuals who can absorb these costs and for those who have already maximized contributions to other retirement accounts.

For most people, a simple term life insurance policy with an adequate death benefit, combined with investing any disposable income in tax-advantaged retirement accounts, is the best approach to incorporating life insurance into retirement planning. Term life insurance provides basic financial protection for dependents at a relatively low cost, freeing up more income for other investments.

In summary, life insurance can be a valuable component of retirement planning, particularly for high-net-worth individuals or those who have maximized other retirement savings options. However, for the majority, a term life insurance policy combined with other investment strategies is the most effective approach.

Cigna Life Insurance: Depression History and Rejection Risk

You may want to see also

Explore related products

![Property and Casualty Insurance License Exam Study Guide: Property Casualty Insurance Book and Practice Test Questions [3rd Edition]](https://m.media-amazon.com/images/I/71MhA+5nDML._AC_UY218_.jpg)

![]()

Life insurance for debt repayment assistance

Life insurance is an asset that can be included in your net worth calculations. It is a necessity for most people, and its inclusion in net worth calculations depends on whether you can benefit financially from your policy while you are still alive.

Term life insurance, which only pays out to your dependents upon your death, is not considered an asset. On the other hand, whole life insurance and other types of permanent life insurance with a cash value component are considered assets as they allow you to withdraw funds while you are alive.

Now, let's discuss life insurance in the context of debt repayment assistance:

Life insurance can be a valuable tool for debt repayment assistance for both yourself and your loved ones. Here are some key points to consider:

Using Life Insurance for Debt Repayment

The primary purpose of life insurance is to replace your income after your death. If you have significant debts that your loved ones may inherit, such as cosigned loans or joint debts, a life insurance payout can help them pay off these debts. Additionally, even if your debts are not passed on, a life insurance payout can ensure that your beneficiaries can preserve their inheritance by using the funds to settle your debts.

Term Life Insurance vs. Permanent Life Insurance for Debt Repayment

Term life insurance is often sufficient for covering debts. These policies are designed for a set period, such as 10 or 20 years, and can match the length of loans like mortgages. Permanent life insurance, on the other hand, is more expensive and offers lifelong coverage. It may be a good option if you want your beneficiaries to receive a payout regardless of when you pass away.

Credit Life Insurance

Credit life insurance is a specific type of coverage offered by lenders to pay off a particular loan in the event of your death. While it ensures the loan is repaid, it does not provide additional funds to your beneficiaries. Additionally, credit life insurance is typically more expensive than traditional life insurance and may not be necessary if you have sufficient coverage through other means.

Borrowing Against Life Insurance

In some cases, you may be able to borrow against the cash value of your life insurance policy to consolidate debt. This option is available for certain types of policies, such as whole life or universal life insurance, and can provide funds to pay off credit card debt or other financial obligations. However, it is important to weigh the pros and cons, as there may be tax implications, and failing to repay the loan could reduce your death benefits.

In conclusion, life insurance can play a crucial role in debt repayment assistance, providing financial protection for both yourself and your loved ones. It is important to carefully consider your options, including the type of life insurance policy and whether to borrow against its value, to ensure you make the best decision for your specific circumstances.

Whole Foods: Free Life Insurance for Employees?

You may want to see also

Explore related products

![]()

Life insurance for families with young children

Life insurance is often included in a person's net worth calculation, but this depends on the type of life insurance. Term life insurance is not considered an asset because it doesn't have a cash value component, whereas whole life insurance is considered an asset because it has a cash value that can be withdrawn while the policyholder is still alive.

Now, here is a detailed discussion on life insurance for families with young children.

As a parent, you want to ensure your children are protected and provided for, even in unforeseen circumstances. Life insurance for children can be a sensitive topic, but it is an important aspect of financial planning for families. Here are some key considerations and options for life insurance when it comes to young children:

Standalone Policies vs. Riders:

You have the option to purchase a standalone life insurance policy for your child, or you can add them to your own policy as a rider. Standalone policies are permanent life insurance policies that provide coverage for the child's entire life, as long as premiums are paid. Riders, on the other hand, are typically added to a parent's term or permanent policy and offer coverage for the child until they reach adulthood. Riders can often be converted into standalone policies when the child becomes an adult.

Benefits of Child Life Insurance:

One advantage of securing life insurance for your child at a young age is that it guarantees their future insurability. This is especially important if your family has a history of medical issues, as it can become challenging and expensive to obtain life insurance later in life. Additionally, in the unfortunate event of a child's death, life insurance can provide financial support for funeral expenses and give grieving parents the flexibility to take time off work.

Types of Policies:

When it comes to life insurance for children, there are two main types of policies: term life insurance and whole life insurance. Term life insurance provides coverage for a fixed period, usually until the child reaches adulthood, and it only offers death benefits. Whole life insurance, on the other hand, provides lifelong coverage and includes a savings component called the cash value, which can be borrowed against or paid out.

Affordability and Coverage:

Life insurance for children tends to be more affordable than policies for adults, with premiums as low as $5 to $10 for a $10,000 policy. Coverage amounts vary, but they typically range from $10,000 to $50,000 for term policies and can go up to $500,000 for whole life policies.

When to Purchase:

Most companies offer coverage for children from 14 days to 17 years old, with some extending coverage up to 18 years. It's important to note that the earlier you purchase life insurance for your child, the lower the premiums are likely to be, as rates are locked in at the time of coverage.

Choosing a Provider:

When selecting a life insurance provider for your child, it's essential to consider factors such as the company's financial stability, customer satisfaction ratings, and the availability of riders and policy options. Reputable companies like American Family, Mutual of Omaha, Aflac, and Foresters offer flexible payment options, high coverage amounts, and additional riders to enhance your child's coverage.

In conclusion, while the topic of life insurance for young children may be difficult to contemplate, it can provide invaluable peace of mind and financial security for your family. By understanding the different types of policies, coverage options, and reputable providers, you can make an informed decision that aligns with your family's needs and ensures your children's future is protected.

Life Insurance for Expecting Mothers: What You Need to Know

You may want to see also

Frequently asked questions

Net worth is the combined value of your assets, or the things you own that have monetary value, minus the value of your liabilities (the accounts or loans that you’re paying off).

Only permanent life insurance policies, like whole life insurance, are considered assets because they can grow cash value. Term life insurance is not considered an asset because it does not accumulate cash value.

Your net worth is the sum of all your assets minus the sum of all your liabilities. Assets include the money in your checking and savings accounts, your retirement accounts, life insurance, and any other investments you’ve made. Liabilities include any money you owe, such as student loans, auto loans, personal loans, consumer debt, and mortgages.