In recent years, the relationship between health insurance and taxes has become a topic of significant interest and confusion for many taxpayers. The question of whether you owe taxes if you don't have health insurance stems from the Affordable Care Act's (ACA) individual mandate, which initially required most Americans to have health coverage or face a penalty. However, with the Tax Cuts and Jobs Act of 2017, the federal penalty for not having health insurance was effectively eliminated starting in 2019. Despite this change, some states have implemented their own mandates and penalties, creating a patchwork of rules that vary by location. Understanding these nuances is crucial for taxpayers to navigate their obligations and avoid potential state-level penalties.

| Characteristics | Values |

|---|---|

| Tax Penalty for No Health Insurance | As of 2023, there is no federal tax penalty for not having health insurance. |

| State-Level Penalties | Some states (e.g., California, Massachusetts, New Jersey, Rhode Island, Vermont) impose their own penalties for lacking health insurance. |

| Penalty Amount (Federal, Pre-2019) | The federal penalty was eliminated starting January 1, 2019, under the Tax Cuts and Jobs Act. |

| Penalty Calculation (Pre-2019) | The greater of: 2.5% of household income above the tax return filing threshold, or $695 per adult ($347.50 per child) up to a family cap of $2,085. |

| Impact on Tax Returns | No federal impact since 2019; state penalties may affect state tax returns. |

| Exemptions (Pre-2019) | Hardship exemptions, short coverage gaps (less than 3 months), income below tax filing threshold, etc. |

| Affordable Care Act (ACA) Mandate | The individual mandate still exists but has no federal penalty; states may enforce their own mandates. |

| Reporting Requirements | No federal requirement to report health insurance status on tax returns since 2019. |

| Future Changes | Federal penalties could be reinstated by legislative changes, but none are currently proposed. |

| State-Specific Rules | Check individual state laws for penalties, exemptions, and reporting requirements. |

Explore related products

What You'll Learn

- Penalty for No Coverage: Details on fines for lacking health insurance under certain tax laws

- Exemptions Available: Circumstances where you’re exempt from penalties for not having insurance

- State vs. Federal Rules: Differences in tax requirements for health insurance across states

- Affordable Care Act Impact: How ACA influences tax obligations for uninsured individuals

- Filing Without Insurance: Steps to report uninsured status accurately on tax returns

![]()

Penalty for No Coverage: Details on fines for lacking health insurance under certain tax laws

In the United States, the Affordable Care Act (ACA) introduced the individual shared responsibility payment, commonly known as the penalty for not having health insurance. This penalty was designed to encourage individuals to maintain health coverage, thereby reducing the number of uninsured and spreading the cost of healthcare more broadly. However, the Tax Cuts and Jobs Act of 2017 effectively eliminated this federal penalty starting in 2019, meaning that most individuals no longer face a federal fine for lacking health insurance.

Despite the federal penalty's elimination, some states have implemented their own mandates and penalties to ensure residents have health coverage. For example, California, New Jersey, Massachusetts, Rhode Island, and the District of Columbia have enacted state-level individual mandates. These states require residents to have qualifying health insurance or pay a penalty when filing their state taxes. The penalties vary; for instance, in California, the penalty for 2023 is calculated as either a flat fee of $800 per adult and $400 per child, or 2.5% of household income above the state’s tax filing threshold, whichever is greater.

Understanding whether you owe a penalty depends on your state of residence and the specifics of its mandate. For example, in Massachusetts, the penalty is based on the number of months you were uninsured and your income level. If you’re uninsured for the entire year and your income is above 300% of the federal poverty level, you could face a penalty of up to $1,570. It’s crucial to check your state’s regulations, as exemptions may apply for financial hardship, short coverage gaps, or religious beliefs.

To avoid penalties, individuals in states with mandates should ensure they have qualifying health insurance, which typically includes plans purchased through the marketplace, employer-sponsored plans, Medicare, Medicaid, or other government programs. If you’re unsure whether your coverage qualifies, consult the state’s health insurance marketplace or a tax professional. Additionally, keeping detailed records of your health insurance coverage throughout the year can simplify tax filing and help prove compliance if questioned.

While the federal penalty for lacking health insurance is no longer in effect, state-level mandates highlight the ongoing importance of maintaining coverage. Penalties can be significant, and the rules vary widely by state, making it essential to stay informed. Proactively securing health insurance not only avoids fines but also ensures access to necessary healthcare services, providing both financial and health-related peace of mind.

How Health Insurance Agents Earn Money: Commissions, Bonuses, and More

You may want to see also

Explore related products

![]()

Exemptions Available: Circumstances where you’re exempt from penalties for not having insurance

In the United States, the Affordable Care Act (ACA) introduced the individual mandate, requiring most individuals to have health insurance or face a tax penalty. However, not everyone is subject to this penalty. Certain circumstances qualify individuals for exemptions, providing relief from the financial burden of the mandate. Understanding these exemptions is crucial for those who may struggle to afford insurance or face unique situations that make coverage impractical.

Hardship Exemptions: A Lifeline for the Financially Strained

Individuals experiencing financial hardships can breathe a sigh of relief. The ACA recognizes that unforeseen circumstances can make insurance unaffordable. If you've faced eviction, bankruptcy, substantial medical debt, or other qualifying hardships, you may be eligible for an exemption. This exemption is not automatic; you must apply through the Health Insurance Marketplace, providing documentation to support your claim. It's a safety net for those facing temporary financial crises, ensuring they aren't penalized during already challenging times.

Religious Conscience and Health Care Sharing Ministries

For those with deeply held religious beliefs, the ACA offers a unique exemption. Members of recognized religious sects with objections to insurance can seek an exemption. Similarly, individuals participating in Health Care Sharing Ministries, where members share medical expenses, are also exempt. These exemptions cater to specific communities, acknowledging their alternative approaches to healthcare and financial responsibility.

Income-Based Exemptions: When Coverage is Unaffordable

The ACA's definition of 'affordable' insurance is crucial here. If the cost of the cheapest available plan exceeds 8.5% of your household income, you're exempt from the penalty. This exemption is automatically applied when filing taxes, ensuring that individuals and families aren't forced into financial strain to comply with the mandate. It's a practical adjustment, recognizing the diverse economic realities of Americans.

Short Coverage Gaps and Other Scenarios

Life is unpredictable, and the ACA accounts for this. If you were without coverage for less than three consecutive months, you're exempt from the penalty for that period. Additionally, individuals experiencing homelessness, those recently released from incarceration, or members of a federally recognized tribe also qualify for exemptions. These scenarios highlight the law's flexibility, accommodating various life situations and ensuring that penalties are not imposed unfairly.

Understanding these exemptions is essential for anyone navigating the complexities of health insurance and tax regulations. Each exemption serves a specific purpose, providing relief to those facing unique challenges. By recognizing these circumstances, the ACA aims to balance the need for widespread insurance coverage with the understanding that one-size-fits-all solutions can fall short in a diverse society.

Does Insurance Cover Mental Health Counseling? What You Need to Know

You may want to see also

Explore related products

![]()

State vs. Federal Rules: Differences in tax requirements for health insurance across states

The Affordable Care Act (ACA) introduced a federal mandate requiring most Americans to have health insurance or pay a penalty, known as the individual shared responsibility payment. However, this federal penalty was effectively eliminated starting in 2019, leaving the question of tax obligations for uninsured individuals largely to state-level regulations. This shift highlights the growing importance of understanding how state rules diverge from federal guidelines in taxing health insurance status.

State-Level Penalties: A Patchwork of Requirements

Several states have implemented their own health insurance mandates to fill the void left by the federal penalty’s repeal. For example, California, Massachusetts, New Jersey, Rhode Island, and the District of Columbia require residents to maintain minimum essential coverage or face a state tax penalty. In California, the penalty for 2023 is calculated as either a flat fee of $800 per adult and $400 per child (up to a family maximum of $2,400) or 2.5% of household income above the state’s tax filing threshold, whichever is greater. These state penalties are enforced through state tax returns, not federal ones, creating a layered compliance requirement for residents.

States Without Penalties: A Different Landscape

In contrast, the majority of states have not enacted individual mandates or penalties for lacking health insurance. In these states, residents are not required to report their insurance status on state tax returns, and there are no financial consequences for being uninsured. However, this lack of penalty does not exempt individuals from potential federal tax implications related to subsidies or other ACA-related provisions. For instance, if someone in a non-mandate state receives premium tax credits through the federal marketplace, they must reconcile these credits on their federal return, regardless of state rules.

Practical Tips for Navigating State vs. Federal Rules

To avoid surprises during tax season, individuals should first determine whether their state has an active health insurance mandate. State revenue agencies often provide clear guidelines on their websites, including penalty calculations and exemptions. For example, Massachusetts allows exemptions for financial hardship or religious beliefs, while California offers waivers for individuals who were uninsured for less than three consecutive months. Additionally, taxpayers should keep documentation of their health insurance status, such as Form 1095, to support their filings.

The Broader Impact: Compliance and Policy Implications

The divergence between state and federal rules underscores the complexity of health insurance taxation in the U.S. While federal policy has moved away from penalizing the uninsured, state-level mandates reflect varying priorities around healthcare access and cost containment. For taxpayers, this means that geographic location can significantly influence their tax obligations. As more states consider implementing or modifying mandates, staying informed about local regulations is essential for compliance and financial planning.

Reimbursing Employees for Health Insurance: A Comprehensive Guide for Employers

You may want to see also

Explore related products

![]()

Affordable Care Act Impact: How ACA influences tax obligations for uninsured individuals

The Affordable Care Act (ACA), often referred to as Obamacare, introduced significant changes to the U.S. healthcare system, including its intersection with tax obligations. One of its key provisions was the individual mandate, which required most Americans to have health insurance or pay a penalty. While the federal penalty for not having insurance was effectively eliminated in 2019, the ACA’s influence on tax obligations for uninsured individuals remains relevant, particularly at the state level and through indirect mechanisms. Understanding these nuances is crucial for anyone navigating the complexities of healthcare and taxes.

For instance, five states (California, Massachusetts, New Jersey, Rhode Island, and the District of Columbia) and Vermont (starting in 2024) have reinstated their own individual mandates, requiring residents to have health insurance or face a state-level penalty. This penalty is typically assessed when filing state taxes and can vary widely. For example, in California, the penalty for 2023 is calculated as either a flat fee of $800 per adult and $400 per child, or 2.5% of household income above the state’s tax filing threshold, whichever is higher. Uninsured individuals in these states must factor this into their tax planning, as it directly impacts their financial obligations.

Beyond state-level penalties, the ACA indirectly influences tax obligations through its emphasis on health insurance coverage. For example, uninsured individuals may miss out on tax benefits available to those with health savings accounts (HSAs) or marketplace subsidies. HSAs offer triple tax advantages—contributions are tax-deductible, grow tax-free, and can be withdrawn tax-free for qualified medical expenses—but require enrollment in a high-deductible health plan. Similarly, individuals who forgo insurance may not qualify for premium tax credits, which can significantly reduce the cost of marketplace plans. These missed opportunities highlight how the ACA’s framework incentivizes coverage through tax benefits.

Another critical aspect is the ACA’s expansion of Medicaid, which provides free or low-cost health coverage to eligible individuals. In states that have expanded Medicaid, uninsured individuals with incomes up to 138% of the federal poverty level may qualify for coverage at little to no cost. Failing to enroll not only leaves them uninsured but also means they forgo a benefit that could alleviate financial strain. While this doesn’t directly impact tax obligations, it underscores the ACA’s broader goal of reducing the uninsured rate and its indirect financial implications.

In conclusion, while the federal penalty for not having health insurance has been eliminated, the ACA continues to shape tax obligations for uninsured individuals, particularly through state-level mandates and missed tax benefits. Residents of states with individual mandates must account for potential penalties when filing taxes, while all uninsured individuals should consider the long-term financial advantages of securing coverage. The ACA’s legacy is one of interconnectedness between healthcare and taxes, making it essential to stay informed about both federal and state regulations to make financially sound decisions.

Invisalign and Medical Insurance: What's Covered?

You may want to see also

Explore related products

![TurboTax Deluxe Desktop Edition 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71OcM906MLL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UL320_.jpg)

![TurboTax Premier Desktop Edition 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71ofxs16-9L._AC_UL320_.jpg)

![TurboTax Home & Business Desktop Edition 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71-jbdrZxVL._AC_UL320_.jpg)

![TurboTax Deluxe Desktop Edition 2025, Federal Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71pX8Fh2sNL._AC_UL320_.jpg)

![]()

Filing Without Insurance: Steps to report uninsured status accurately on tax returns

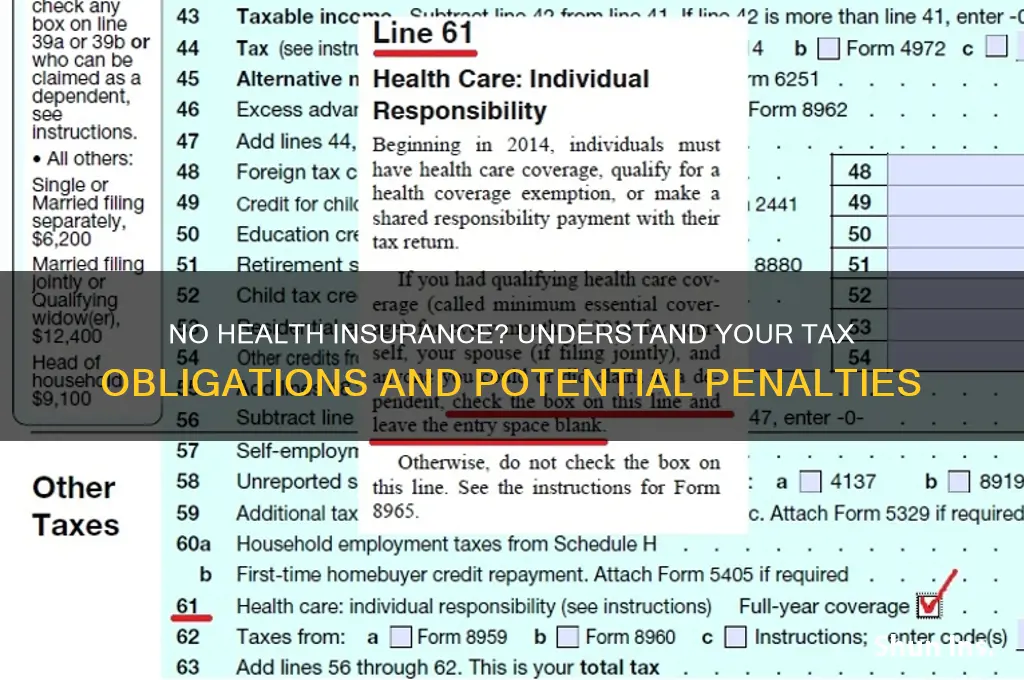

Reporting your uninsured status on tax returns requires precision to avoid penalties or delays. Start by understanding Form 1040, where the IRS asks about your health insurance coverage. Line 61 of this form includes a checkbox for indicating whether you had coverage for the entire year. If you lacked insurance, leave this box unchecked—a simple yet critical step that signals your uninsured status to the IRS.

Next, determine if you qualify for an exemption from the Shared Responsibility Payment, which was enforced under the Affordable Care Act (ACA). While the federal penalty for being uninsured was reduced to $0 starting in 2019, some states like California, Massachusetts, New Jersey, Rhode Island, and Washington still impose their own penalties. Use Form 8965 to claim exemptions, such as financial hardship or short coverage gaps (less than three consecutive months). Each exemption has specific criteria, so review IRS guidelines or consult a tax professional to ensure accuracy.

For those in states with mandates, accurately reporting uninsured status involves additional steps. For instance, California residents must file Form 3895 with their state return. This form requires details like the number of uninsured months and applicable penalties. Double-check calculations, as errors can lead to overpayment or underpayment. Online tax software often includes state-specific prompts, but manual filers should pay close attention to state instructions.

Finally, keep thorough records to support your uninsured status. Document attempts to obtain coverage, such as denied applications or quotes exceeding 8.5% of your household income (a common hardship threshold). If you had partial coverage during the year, gather policy details and dates. These records are essential if the IRS requests verification or if you need to amend a return later. Accurate reporting not only ensures compliance but also minimizes the risk of audits or penalties.

Why Bermuda Attracts Global Insurance Giants as Their Headquarters Hub

You may want to see also

Frequently asked questions

Yes, under the Affordable Care Act (ACA), you may owe a tax penalty for not having health insurance, though the federal penalty was eliminated starting in 2019. However, some states (like California, New Jersey, and Massachusetts) have their own mandates and penalties for lacking coverage.

The federal penalty was eliminated in 2019, so there is no longer a federal tax penalty. However, state penalties vary. For example, California’s penalty is calculated as a percentage of your income or a flat fee, whichever is higher. Check your state’s specific rules for details.

No, not everyone owes taxes for lacking health insurance. If you qualify for an exemption (e.g., low income, short coverage gaps, or religious reasons), you may not owe a penalty. Additionally, if your state does not have a mandate, you won’t owe anything.

If you can’t afford health insurance and don’t qualify for Medicaid or subsidies, you may be exempt from the penalty in states with mandates. However, you’ll need to claim the exemption when filing taxes. Always check your state’s specific rules and exemptions.

![H&R Block Tax Software Deluxe 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51Mlng5FWYL._AC_UL320_.jpg)

![H&R Block Tax Software Premium 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51dMIAMHkkL._AC_UL320_.jpg)

![TurboTax Business Desktop Edition 2025, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71iKclcd6ML._AC_UL320_.jpg)

![H&R Block Tax Software Premium & Business 2025 Win [PC Online code]](https://m.media-amazon.com/images/I/618kxmZlTGL._AC_UL320_.jpg)