Health insurance premiums have been rising rapidly, causing financial strain for many. There are several factors contributing to this increase, including market concentration among fewer insurance companies, age, inflation, and medical inflation driven by advancements in medical treatments and procedures. These rising costs impact both individuals and employers, who may struggle to balance spending and coverage. While some measures, such as rate reviews and the 80/20 rule, aim to hold insurance companies accountable and curb unreasonable premium hikes, consumers often have limited control over the factors influencing health insurance prices. This situation underscores the importance of strategic approaches, such as investing in wellness programs and exploring alternative coverage options, to mitigate the financial burden of increasing health insurance premiums.

| Characteristics | Values |

|---|---|

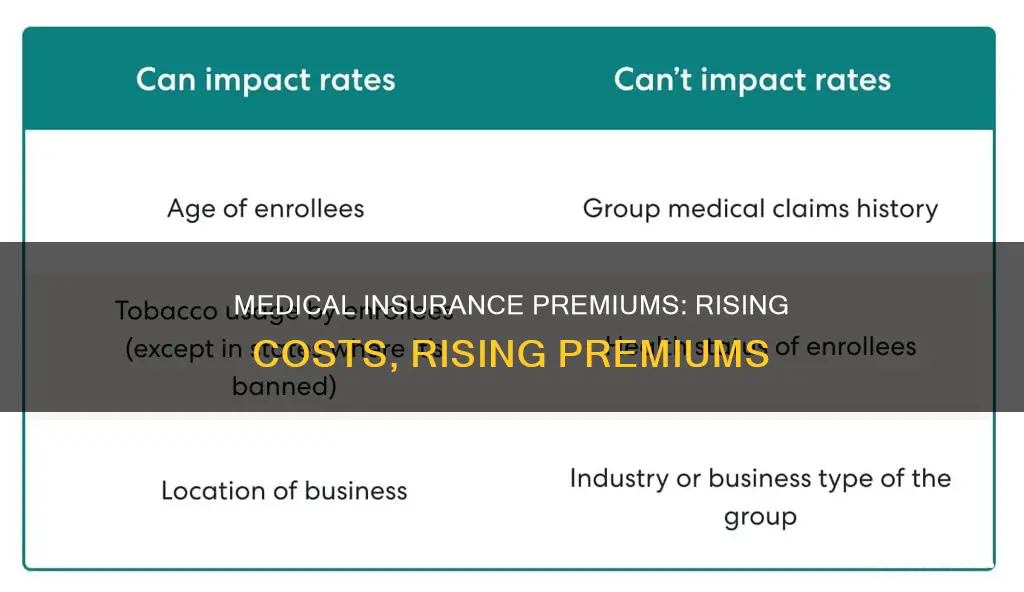

| Reason for increase in medical insurance | Inflation, claims, age, medical inflation |

| Factors that influence health insurance prices | Age, market concentration, medical breakthroughs |

| Ways to fight unreasonable health insurance premium increases | Rate review, 80/20 rule, medical loss ratio regulation |

| Ways to keep coverage affordable | Switch to a cheaper plan, invest in wellness programs, use a Health Reimbursement Arrangement (HRA) |

Explore related products

What You'll Learn

![]()

Inflation and medical inflation

Inflation refers to the rate at which the cost of goods and services increases over time, resulting in a decrease in the purchasing power of money. In other words, with inflation, you will need to spend more money to buy the same goods and services as before. Inflation can affect various sectors of the economy, including healthcare.

Medical inflation specifically refers to the increase in the cost of medical goods and services, such as doctor visits, treatments, procedures, prescription drugs, and insurance. Medical inflation can be influenced by various factors, including medical breakthroughs, new technologies, and an aging population. While medical inflation has historically outpaced overall economic inflation, there have been periods, such as after the 2008 financial crisis, where economic inflation slowed while medical inflation continued to grow.

According to data from the Bureau of Labor Statistics (BLS) and the Bureau of Economic Analysis (BEA), the overall inflation rate between December 2020 and December 2021 was 5.8%, while the healthcare services inflation rate during the same period was 2.7%. More recently, in June 2024, overall prices increased by 3.0% year-over-year, while prices for medical care increased by 3.3%. This marks a return to medical inflation outpacing overall economic inflation after a period of rapid increases in non-medical goods and services.

In addition to medical inflation, health insurance premiums are influenced by other factors such as age, claims, and overall economic inflation. Insurers take into account the likelihood of policyholders needing to make a claim as they get older, which can result in higher premiums. Claims made by other policyholders can also impact the cost of premiums for everyone. Furthermore, market concentration among insurance companies can contribute to higher insurance costs, as fewer companies in the market can lead to higher premiums and decreased access to affordable health insurance.

Hospitals and Lapsed Insurance: Treatment Access Barriers

You may want to see also

Explore related products

![]()

Market concentration

The consequences of market concentration in health insurance are significant. Firstly, it can lead to higher insurance costs and premiums due to reduced competition. With fewer insurers in the market, there is less incentive to keep prices competitive, and consumers may face limited choices and decreased access to affordable health insurance. Secondly, market concentration can impact the quality of care and patient satisfaction. Studies have shown a positive association between insurance concentration and patient satisfaction, while hospital concentration has a negative impact. This suggests that patients in markets with higher insurance concentration tend to have a better experience, possibly due to hospitals competing for favourable insurance contracts and improved quality of care.

The reasons behind the increasing market concentration include consolidation through mergers and acquisitions among insurance companies, as well as existing insurers exiting the market, reducing the number of options for consumers. This concentration of power can make it challenging for new issuers to enter the market and compete with established players.

The implications of market concentration in health insurance have drawn the attention of researchers, policymakers, and health insurance groups. The American Medical Association's 2013 report highlighted the prevalence of highly concentrated health insurance markets across the country, as defined by the Department of Justice (DOJ) and Federal Trade Commission (FTC) guidelines. The impact of market concentration on insurance premiums and patient care underscores the importance of addressing this issue to ensure competitive pricing and maintain quality healthcare services for Americans.

In conclusion, market concentration in the health insurance industry has significant implications for consumers and the overall healthcare landscape in the United States. As the market becomes more concentrated, it is crucial to explore measures that promote competition, ensure affordable insurance options, and maintain high standards of patient care.

Pregnancy and Insurance: What's Covered?

You may want to see also

Explore related products

![]()

Ageing

The impact of ageing on health insurance premiums is influenced by several factors. Firstly, the decline in the immune system's effectiveness makes older individuals more prone to infections and illnesses, necessitating more medical interventions. Secondly, the recovery process from injuries or illnesses tends to take longer as the body ages, leading to prolonged treatments and higher medical costs. Thirdly, older individuals are more likely to require costly surgeries due to the wear and tear of the body or chronic conditions, which further drives up insurance premiums.

The cost of health insurance varies with age, and it tends to increase as individuals get older. For instance, the average cost of health insurance at age 24 is approximately $486 per month, while at age 26, it rises to $498 per month. The rates continue to climb, with individuals facing even higher premiums in their sixties. According to federal rules, insurance companies can charge older adults up to three times the premium of younger adults, although this varies across states. For example, in Washington, D.C., the impact of age on health insurance costs is less pronounced, with smaller and more gradual rate increases.

To mitigate the financial burden of ageing, individuals can explore various options. Firstly, purchasing health insurance at a younger age can result in lower premiums. Secondly, comparing different insurance plans and opting for super top-up plans or family discount options can provide more affordable coverage. Additionally, customising insurance plans with add-ons like critical illness cover can enhance protection. For those over 65, enrolling in Medicare can significantly reduce costs, with monthly expenses ranging from $185 to $409 depending on the chosen plan.

Insurance Backpay: Can It Cover Past Medical Expenses?

You may want to see also

Explore related products

![]()

Medical breakthroughs

While there is no direct correlation between medical breakthroughs and insurance rates, there are some breakthroughs that could potentially lower insurance costs in the long run.

One of the most significant ways in which medical breakthroughs can impact insurance rates is by reducing the need for expensive treatments and procedures. For example, the development of a blood test to easily detect a disease that affects one in nine people over the age of 65 can lead to earlier diagnosis and treatment, potentially reducing the need for costly interventions later on. Similarly, advancements in organ transplantation, such as the successful transplantation of organs from pigs into humans, may offer a more accessible and cost-effective alternative to traditional organ donation, which has been struggling to meet the rising demand. This could reduce the financial burden on insurance providers and potentially lead to lower insurance rates over time.

Additionally, breakthroughs in the field of women's health could have an impact on insurance rates. With a better understanding of why women are more vulnerable to autoimmune diseases, there may be opportunities to develop more targeted and cost-effective treatments, reducing the overall financial burden associated with these conditions. Furthermore, the availability of the first-ever birth control pill without a prescription in the United States could improve access to contraception and potentially reduce unintended pregnancies, which could have a positive impact on insurance costs over time.

It is important to note that the impact of medical breakthroughs on insurance rates is complex and influenced by various factors, including the adoption and accessibility of these advancements. Additionally, insurance rates are influenced by a wide range of market features, such as provider and insurer competition, as well as broader economic trends. While medical breakthroughs can play a role in reducing costs, there are also social and economic factors that need to be addressed to ensure equitable access to healthcare and insurance coverage.

To directly address the issue of high insurance rates, policymakers and state commissions have implemented various strategies. These include increasing antitrust enforcement, reducing providers' incentives to consolidate, expanding site-neutral payment policies in Medicare, and lowering the threshold for premerger filings. Additionally, the American Rescue Plan Act of 2021 and the Inflation Reduction Act have expanded savings and lower costs for individuals, with more people qualifying for help with their health coverage. These legislative changes, combined with medical breakthroughs, may contribute to reducing insurance rates over time.

Supplemental Medical Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Employer-sponsored plans

Employer-sponsored health insurance, also known as employer-sponsored insurance, employer-provided health insurance, or group health insurance, is health insurance offered to employees and their dependents through their job. It is the most common way Americans obtain insurance, with nearly 60% of insured Americans securing coverage through an employer-sponsored plan.

Employers with at least 50 full-time employees or equivalents are typically required to provide health coverage to their workers. Applicable large employers (ALEs) that fail to do so may be subject to penalties. Small employers are not required to provide coverage, but they may qualify for the Tax Credit for Small Employer Health Insurance Premiums if they choose to do so.

In addition to major medical plans, employers may also offer supplemental coverage such as dental, vision, life, and short- and long-term disability insurance. Group health plans, including small-group, large-group, and self-insured plans, must be guaranteed issue, meaning the plan must cover all enrollees whose employment qualifies them for coverage.

As of 2024, a health plan is considered "affordable" if the premium is not more than 8.39% of the employee's household income. This threshold will increase to 9.02% in 2025. If an employer's plan meets the standard for minimum value and affordability, employees will not qualify for premium tax credits if they choose to purchase a Marketplace insurance plan instead.

Medicaid as Secondary Insurance: A Doctor's Billing Dilemma

You may want to see also

Frequently asked questions

Insurance companies raise rates when actual medical costs are lower than projected, allowing them to maintain higher rates while spending less.

The Affordable Care Act mandates that large proposed increases are evaluated by experts to ensure they are based on reasonable cost assumptions. This scrutiny helps moderate premium hikes and provides consumers with greater value.

If your insurance company is unresponsive, you can file a complaint with the Department of Insurance (DOI).

You can file an internal appeal with your insurer. If the insurer denies your appeal, you can request an external review through the relevant state authority, such as the Massachusetts Office of Patient Protection (OPP).