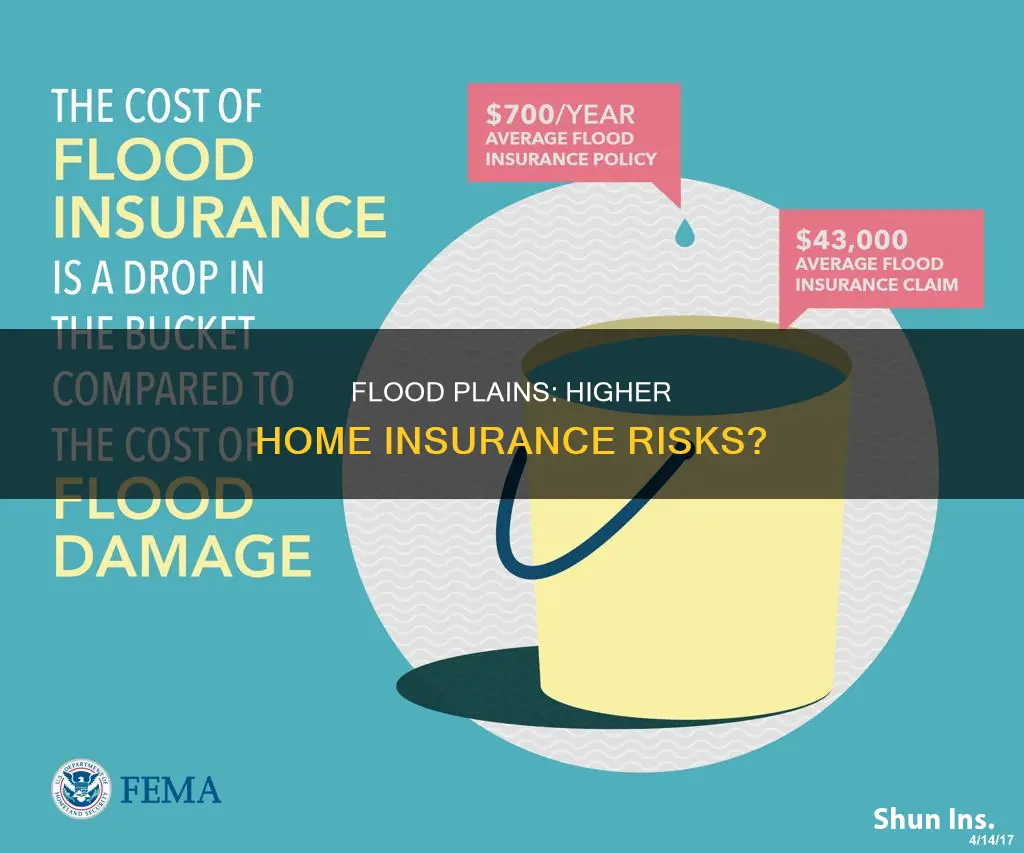

Floodplains are critical for the natural management of floodwaters, but they also pose risks to properties and lives. Flood insurance is mandatory for buildings in high-risk flood zones, including 100-year flood plains, if the property owner has a mortgage from a federally regulated or insured lender. The National Flood Insurance Program (NFIP) calculates flood insurance rates based on a combination of rating variables for each property to reflect its flood risk. FEMA maps the areas with a 1% annual chance of flooding, which is also known as the 100-year floodplain or Special Flood Hazard Area (SFHA). This designation is essential as it determines whether flood insurance is required for a property. The likelihood of flooding, building characteristics, and elevation all impact insurance rates. Living in a 100-year floodplain significantly affects insurance requirements and rates, so homeowners must regularly review their flood risk and insurance coverage.

| Characteristics | Values |

|---|---|

| Flood Factor | A number from 1-10 indicating the likelihood of flooding and the potential height of floods. |

| Flood Plains | Floodway, 100-year floodplain, 500-year floodplain, 50-year floodplain, 25-year floodplain, 10-year floodplain |

| Flood Insurance | Mandatory for buildings in high-risk flood zones (100-year flood plain or zones marked by the letters A or V) if the property owner has a mortgage from a federally-regulated or insured lender. |

| Flood Insurance Cost | Determined by factors such as the building's square footage, zip code, and replacement cost value. |

| Flood Insurance Reduction Options | Choosing a higher deductible, building in a location with a lower flood risk, and increasing the building's elevation above the base flood elevation. |

Explore related products

What You'll Learn

- Flood insurance is mandatory for properties in high-risk flood zones

- Flood Factors range from minimal to extreme, but aren't used by the NFIP

- The NFIP calculates flood insurance rates based on unique property variables

- Flood plains are categorised by their likelihood of flooding, from floodways to 500-year flood plains

- Flood insurance costs are based on factors like building characteristics and elevation

![]()

Flood insurance is mandatory for properties in high-risk flood zones

In the United States, flood insurance is required by law for buildings in high-risk flood zones if the property owner has a mortgage from a federally regulated or insured lender. These high-risk zones are identified as 100-year flood plains or zones marked by the letters "A" or "V" on FEMA flood maps. FEMA's flood maps indicate areas with a 1% annual risk of flooding, which is the minimum standard for mandatory flood insurance purchase.

The National Flood Insurance Program (NFIP) handles the majority of flood insurance policies in the U.S. and works in partnership with the Federal Emergency Management Agency (FEMA). The NFIP provides flood insurance to property owners, renters, and businesses, aiding in their recovery after flood events. While the NFIP calculates flood insurance rates based on a property's flood risk, it is important to note that flood insurance costs can be influenced by factors such as property value, building characteristics, and elevation.

Living in a high-risk flood zone, such as the 100-year floodplain, significantly impacts insurance considerations for property owners. Even a slight difference in location concerning the 100-year flood line can impact the mandatory insurance requirement. Additionally, factors like the building's elevation relative to the base flood elevation can affect insurance rates, with elevated buildings sometimes qualifying for lower premiums.

It is recommended that homeowners and businesses regularly review their flood risk and insurance options. While flood insurance is mandatory in high-risk zones, it is also available and advisable for properties outside these zones, as flooding can still occur, and most homeowners' insurance does not cover flood damage.

Home Insurance: Bed Bug Damage Covered?

You may want to see also

Explore related products

![]()

Flood Factors range from minimal to extreme, but aren't used by the NFIP

Flood Factors are indicators of a property's 30-year risk of flooding and range from minimal (1) to extreme (10). A higher Flood Factor means a higher likelihood of flooding or experiencing high floods. However, it's important to note that Flood Factors are not used by the National Flood Insurance Program (NFIP) to calculate rates, even though the NFIP handles the majority of flood insurance policies in the US.

The NFIP calculates flood insurance rates based on a unique combination of rating variables for each property to reflect its flood risk. These variables include factors such as the likelihood of different types of floods (e.g., flash flooding, floods caused by waves or high water levels), building characteristics (e.g., foundation type, first-floor elevation), elevation and distance from flooding sources, and the replacement cost value of the building.

In the United States, flood insurance is mandatory for buildings in high-risk flood zones, including 100-year flood plains or zones marked by the letters "A" or "V". These zones have a 1% annual risk of flooding, which translates to a 26% chance of being flooded over a 30-year period, the average mortgage length. It's important to note that even if a property is outside of the 100-year flood zone, it may still be at risk of flooding, and purchasing flood insurance is recommended.

While the NFIP does not use Flood Factors to calculate rates directly, understanding the Flood Factor of a property can still be helpful in assessing the overall flood risk. Homeowners and businesses should regularly review their flood risk and insurance coverage to ensure they are adequately protected against potential losses due to flooding. Additionally, properties in flood-prone areas that are elevated above the base flood elevation may qualify for lower premiums.

Earthquake Insurance in Petaluma: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

The NFIP calculates flood insurance rates based on unique property variables

The National Flood Insurance Program (NFIP) calculates flood insurance rates based on a unique combination of rating variables for each property to reflect its flood risk. The NFIP handles the majority of flood insurance policies in the US.

NFIP's pricing approach is an actuarially sound approach to setting flood insurance premiums. The previous methodology set rates based on geographic zones and elevation. The new approach uses the best available flood risk data to set premiums based on each property's individual risk. This enables FEMA to set rates that are fairer and ensures up-to-date actuarial principles based upon new technology, including modelling.

NFIP's pricing approach is part of an ongoing process to bring rates in line with risks. The approach leverages industry best practices and cutting-edge technology to enable FEMA to deliver rates that are actuarially sound, easier to understand and better reflect a property's flood risk.

The average RCV (Replacement Cost Value) is the estimated cost of replacing the building and any insured contents after a disaster. This calculation is based on a number of factors such as the building's square footage and zip code. Risk-Based Cost of Insurance is what policyholders would pay if they were paying their full actuarial rate as evaluated under the rates implemented on October 1, 2021. This rate is based on the expected costs of losses and programmatic expenses, without subsidies. Many policyholders pay less than their full rate.

The likelihood of different types of flood perils (flash flooding, floods caused by waves or high-water levels, coastal erosion, and more), characteristics of the building (foundation type, first-floor elevation, etc.), elevation and distance from flooding sources (coasts, rivers, lakes), and ways a building is adapted to withstand floods (such as flood vents) are some of the factors that determine the flood risk of a property.

Roof Replacement: Insurer Threat Tactics

You may want to see also

Explore related products

![]()

Flood plains are categorised by their likelihood of flooding, from floodways to 500-year flood plains

Flood plains are categorised by their likelihood of flooding, with floodways being the most prone to flooding, followed by 100-year flood plains and 500-year flood plains. Flood plains play a critical role in the natural management of flood waters, but they also pose risks to properties and lives.

The Federal Emergency Management Agency (FEMA) uses flood maps to determine areas with a 1% or higher chance of experiencing a flood each year as high-risk zones. These areas are deemed to have a 1-in-4 chance of flooding during a 30-year mortgage. The 100-year flood plain, despite its name, does not flood once every 100 years; instead, it has a 1% chance of flooding in any given year, which translates to a 26% chance of flooding over 30 years. This is the minimum requirement for mandatory flood insurance purchase, and it is important to note that even areas outside of this zone are still at risk of flooding.

The 500-year flood plain has a 6% chance of flooding over 30 years, which is significantly lower than the 100-year flood plain. However, it is still considered a high-risk area. Flood Zone A, which encompasses various sub-zones like AE, AH, A99, and AO, is also considered a high-risk area by FEMA. Properties in this zone have a 26% chance of experiencing flooding over a 30-year mortgage, and mortgage companies often require mandatory flood insurance.

The National Flood Insurance Program (NFIP) calculates flood insurance rates based on a combination of rating variables for each property, reflecting its flood risk. Factors such as the building's characteristics, elevation, and distance from flooding sources are considered. Higher-valued properties may have higher premiums due to the greater amount at risk. Additionally, the age of the building, construction materials, and the presence of a basement can affect rates.

Counselors' Duty: Report Illegal Activity to Insurance?

You may want to see also

Explore related products

![]()

Flood insurance costs are based on factors like building characteristics and elevation

Flood insurance is mandatory for buildings in high-risk flood zones (100-year flood plains or zones marked by the letters A or V) if the property owner has a mortgage from a federally regulated or insured lender. A 100-year floodplain does not mean a flood will occur once every 100 years. Instead, it has a 1% annual chance of flooding, translating to a 26% chance of flooding over 30 years, which is the average mortgage length.

Building characteristics such as the age of the building, construction materials, and whether it has a basement affect rates. For instance, elevated utilities, flood vents, and certain types of foundations can significantly reduce costs. The replacement cost value of the building (cost to rebuild after a disaster) is also considered. This calculation is based on factors such as the building's square footage and ZIP code.

Elevation is another critical factor in determining flood insurance costs. Homes built above the Base Flood Elevation (BFE)—a benchmark set by FEMA—typically qualify for lower rates. There are discounts for each foot the house is elevated off the ground. Comparing your home's elevation to the estimated height of floodwater can reduce your insurance costs.

Unlocking Mortgage Insurance Savings: Strategies for Homeowners

You may want to see also

Frequently asked questions

Yes, if your home is in a 100-year floodplain, you are required to purchase flood insurance. This is because these areas have a 1% annual risk of flooding, or a 26% chance of flooding over 30 years (the average length of a mortgage).

The cost of flood insurance varies depending on a combination of rating variables that reflect your property's flood risk. These include the likelihood of different types of flooding, the characteristics of the building, and the elevation and distance from flooding sources.

Yes, you can work with your insurance agent to discuss your options. Choosing a higher deductible will lower your premium, but it will also reduce your claim payment. You can also look into mitigation actions that will lower your flood risk, such as elevating your building above the base flood elevation.