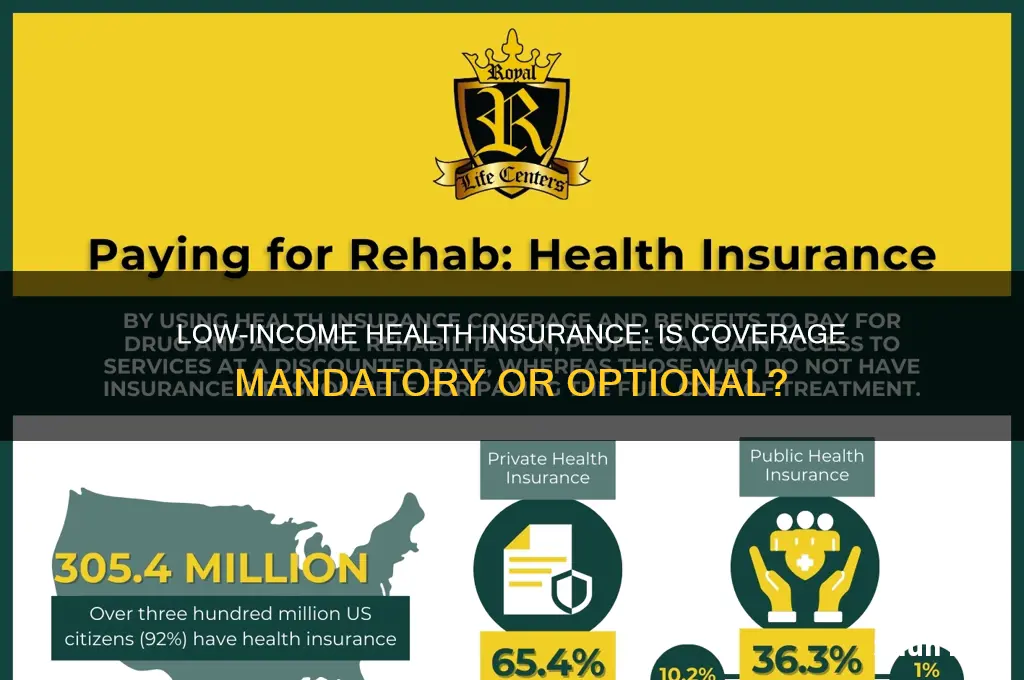

The question of whether a low-income person has to have health insurance is a critical issue that intersects with broader concerns about affordability, accessibility, and policy mandates. In many countries, including the United States, health insurance requirements often come with provisions aimed at assisting those with limited financial resources, such as subsidies, Medicaid expansion, or exemptions from penalties for not having coverage. However, even with these measures, low-income individuals may still face significant barriers, including high out-of-pocket costs, limited provider networks, and the complexity of navigating available programs. This raises important questions about the effectiveness of current policies in ensuring that everyone, regardless of income, can access essential healthcare services without undue financial burden.

| Characteristics | Values |

|---|---|

| Mandated Coverage | In the U.S., the Affordable Care Act (ACA) mandates health insurance, but penalties for not having it were removed at the federal level in 2019. Some states (e.g., California, Massachusetts) still impose penalties. |

| Medicaid Eligibility | Low-income individuals may qualify for Medicaid, a state and federal program providing free or low-cost health coverage. Eligibility varies by state and income level. |

| Children’s Health Insurance Program (CHIP) | CHIP provides low-cost health coverage for children in families who earn too much for Medicaid but cannot afford private insurance. |

| ACA Subsidies | Low-income individuals may qualify for premium tax credits or cost-sharing reductions through the ACA marketplace to reduce insurance costs. |

| Exemptions | Some low-income individuals may be exempt from the insurance mandate if coverage is considered unaffordable (costs > 8.5% of household income). |

| State-Specific Programs | Some states offer additional low-cost or free health insurance programs for low-income residents beyond Medicaid and CHIP. |

| Undocumented Immigrants | Undocumented immigrants are generally ineligible for Medicaid or ACA subsidies but may access emergency services or state-funded programs. |

| Affordability Challenges | Despite subsidies, some low-income individuals still find insurance unaffordable due to high premiums, deductibles, or out-of-pocket costs. |

| Enrollment Periods | Open enrollment for ACA plans typically occurs annually (November 1 to January 15), with special enrollment for qualifying life events. |

| Coverage Gaps | Low-income individuals in states that did not expand Medicaid may fall into the "coverage gap," earning too much for Medicaid but too little for ACA subsidies. |

| Preventive Services | Most insurance plans, including Medicaid and ACA plans, cover preventive services at no cost to the insured. |

| Impact of Income Changes | Changes in income may affect eligibility for Medicaid, CHIP, or ACA subsidies, requiring periodic updates to ensure continued coverage. |

Explore related products

What You'll Learn

![]()

Affordable Care Act Subsidies

Low-income individuals often face a daunting question: Can they afford health insurance? The Affordable Care Act (ACA) addresses this through subsidies, financial assistance designed to make health coverage more accessible. These subsidies, officially known as Advanced Premium Tax Credits (APTC), directly reduce the monthly cost of health insurance premiums purchased through the ACA Marketplace.

For those earning between 100% and 400% of the Federal Poverty Level (FPL), subsidies can significantly lower monthly premiums. For example, a single individual earning $12,880 to $51,520 annually (in 2023) may qualify. Families of four with incomes ranging from $26,500 to $106,000 are also eligible. The subsidy amount is calculated based on income and the cost of the benchmark plan in your area, ensuring that individuals don't spend more than a certain percentage of their income on premiums.

Imagine a single mother earning $30,000 annually. Without subsidies, her monthly premium might be $400. With an APTC, her premium could be reduced to $150 or less, making health insurance far more affordable. It's crucial to note that subsidies are only available for plans purchased through the ACA Marketplace. Enrolling during the annual Open Enrollment Period (typically November 1 to January 15) is essential to access these benefits.

Additionally, cost-sharing reductions (CSRs) are another form of subsidy available to those earning between 100% and 250% of the FPL. CSRs lower out-of-pocket costs like deductibles, copayments, and coinsurance, further easing the financial burden of healthcare.

While subsidies make health insurance more attainable for low-income individuals, understanding eligibility and application processes is key. Utilizing resources like Healthcare.gov and seeking assistance from certified navigators can ensure you maximize these benefits and secure affordable health coverage.

Medical Records and Insurance Adjusters: What's the Custom?

You may want to see also

Explore related products

![]()

Medicaid Eligibility Requirements

Low-income individuals often face the question of whether they are required to have health insurance, and the answer frequently leads to an exploration of Medicaid, a joint federal and state program designed to provide health coverage to eligible low-income individuals and families. Understanding Medicaid eligibility requirements is crucial for those who may qualify, as it can significantly reduce healthcare costs and improve access to essential medical services.

Eligibility Criteria: A Complex Landscape

Medicaid eligibility is a multifaceted process, varying across states due to the program's federal-state partnership. The Affordable Care Act (ACA) aimed to simplify and expand eligibility, but nuances remain. Generally, eligibility is based on income, household size, and specific categorical criteria. For instance, in most states, non-disabled adults without dependent children must meet income limits at or below 138% of the federal poverty level (FPL) to qualify. This translates to an annual income of approximately $18,754 for an individual in 2023. However, some states have more restrictive criteria, creating a patchwork of eligibility rules.

Categorical Requirements: Beyond Income

Income is a primary factor, but Medicaid also considers categorical eligibility. This includes groups such as pregnant women, children, parents, seniors, and individuals with disabilities. For example, children in families with incomes up to 205% of the FPL may qualify, ensuring that a broader range of low-income families can access healthcare for their children. Pregnant women, another priority group, can have income levels up to 138% of the FPL in most states, providing critical prenatal and postnatal care.

Application Process and Documentation

Applying for Medicaid involves submitting an application through the state's designated agency or healthcare marketplace. Applicants must provide documentation to verify income, household composition, and other eligibility factors. This may include pay stubs, tax returns, birth certificates, and proof of residency. The process can be streamlined by gathering these documents beforehand and understanding the specific requirements of your state. Many states offer online applications, making it more accessible and efficient.

The Impact of Medicaid Expansion

The ACA's Medicaid expansion significantly influenced eligibility, particularly for low-income adults without dependent children. As of 2023, 38 states and the District of Columbia have adopted expansion, raising the income eligibility threshold to 138% of the FPL for this group. This expansion has been pivotal in reducing the uninsured rate among low-income adults, offering a safety net for those who previously fell into the 'coverage gap'—earning too much for traditional Medicaid but too little to afford private insurance.

In summary, Medicaid eligibility requirements are a critical aspect of ensuring low-income individuals can access affordable healthcare. While income is a central criterion, categorical eligibility and state-specific variations play significant roles. Understanding these requirements empowers individuals to navigate the application process effectively, potentially securing essential health coverage.

Strategies for Negotiating Medical Bills After Insurance Payouts

You may want to see also

Explore related products

![]()

Penalty for No Coverage

In the United States, the Affordable Care Act (ACA) previously imposed a federal penalty for individuals who did not have health insurance, known as the individual mandate. However, this penalty was effectively eliminated starting in 2019, as the Tax Cuts and Jobs Act reduced the penalty to $0. Despite this change, some states have implemented their own penalties for uninsured residents. For low-income individuals, understanding these penalties is crucial, as they may already face financial strain and limited access to affordable coverage options.

Analyzing the impact of state-level penalties reveals a patchwork of policies. For instance, California, New Jersey, and Massachusetts have reinstated penalties for uninsured residents, with fines calculated as a percentage of income or a flat fee, whichever is higher. In California, the penalty for 2023 is $800 per adult and $400 per child, or 2.5% of household income, whichever is greater. These penalties are designed to encourage enrollment in health plans, but they can disproportionately affect low-income individuals who may struggle to afford coverage even with subsidies.

From a practical standpoint, low-income individuals should explore exemptions from these penalties. Common exemptions include having a household income below the tax filing threshold, experiencing a coverage gap of less than three consecutive months, or qualifying for hardship exemptions due to homelessness, domestic violence, or bankruptcy. For example, if a person’s income is below the federal poverty level (FPL), they may be exempt from state penalties, as they are likely eligible for Medicaid but not required to purchase private insurance.

Persuasively, it’s worth noting that penalties are not the only consideration for low-income individuals. The long-term financial risks of being uninsured—such as high out-of-pocket costs for emergencies or chronic care—often outweigh the immediate cost of penalties. Programs like Medicaid and the Children’s Health Insurance Program (CHIP) offer no-cost or low-cost coverage for eligible individuals, making penalties largely avoidable for those who qualify. However, navigating these programs can be complex, and outreach efforts are essential to ensure awareness and enrollment.

Comparatively, states without penalties may see lower uninsured rates among low-income populations, but this does not necessarily translate to better health outcomes if affordable care remains inaccessible. For instance, Texas, which has no state penalty, has one of the highest uninsured rates in the nation, particularly among low-income residents. This highlights the need for comprehensive solutions beyond penalties, such as expanding Medicaid eligibility and increasing subsidies for marketplace plans. Ultimately, while penalties can incentivize coverage, they are just one piece of a broader strategy to ensure health insurance access for low-income individuals.

Applying for Geisinger Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Free Clinics and Resources

In the United States, low-income individuals often face the daunting question of whether they must have health insurance. While the Affordable Care Act (ACA) mandates coverage, exemptions exist for those whose premiums would exceed 8.5% of their household income. For these individuals, free clinics and resources emerge as vital lifelines, offering essential healthcare services without the burden of insurance. These facilities, often community-based and nonprofit, provide a range of services from primary care to dental and mental health support, ensuring that lack of insurance doesn’t equate to lack of care.

Consider the operational model of free clinics: they rely on volunteer healthcare professionals, grants, and donations to function. For instance, the National Association of Free & Charitable Clinics (NAFC) reports that its member clinics serve over 1.9 million patients annually, delivering care valued at $2.7 billion. These clinics typically operate on a first-come, first-served basis or through appointments, with eligibility often tied to income level rather than insurance status. Practical tip: bring proof of income, such as pay stubs or tax returns, to streamline the registration process. Some clinics also offer sliding-scale fees for medications, ensuring affordability even for those with limited means.

Beyond clinics, low-income individuals can access resources like federally qualified health centers (FQHCs), which receive federal funding to provide comprehensive care on a sliding fee scale. These centers often integrate services like prenatal care, chronic disease management, and preventive screenings, making them one-stop solutions for underserved populations. For example, a 45-year-old diabetic patient without insurance could receive regular glucose monitoring, insulin prescriptions, and dietary counseling at an FQHC, significantly reducing the risk of complications. To locate these centers, visit the Health Resources and Services Administration (HRSA) website and use their "Find a Health Center" tool.

Another critical resource is prescription assistance programs, which help low-income individuals access medications at reduced or no cost. Programs like NeedyMeds and RxAssist provide databases of patient assistance programs offered by pharmaceutical companies. For instance, a patient needing a $300 monthly asthma inhaler could apply for a manufacturer’s program, potentially receiving it for free. Caution: these programs often require detailed applications and proof of financial need, so allow ample time for processing. Additionally, some free clinics have on-site pharmacies, further simplifying access to essential medications.

Finally, mobile clinics and community health fairs extend the reach of free healthcare services, particularly in rural or underserved areas. These initiatives often provide screenings for conditions like hypertension, diabetes, and cancer, alongside vaccinations and health education. For example, a mobile clinic might offer free flu shots to seniors or blood pressure checks for adults over 30, addressing gaps in preventive care. To find such events, check local health department websites or community bulletin boards. These transient resources, while not permanent solutions, play a crucial role in early detection and health promotion for low-income populations.

In conclusion, while health insurance remains a complex issue for low-income individuals, free clinics and resources offer tangible, immediate solutions. By understanding and utilizing these options—from brick-and-mortar clinics to mobile units and prescription assistance—individuals can navigate the healthcare system more effectively. Practical takeaway: combine these resources with preventive measures like maintaining a healthy diet and regular exercise to maximize long-term health outcomes, even without insurance.

Medical History: Privacy and Health Insurance Compatibility

You may want to see also

Explore related products

![]()

State-Specific Insurance Options

In the United States, the Affordable Care Act (ACA) mandates that most individuals have health insurance or pay a penalty, but low-income individuals may qualify for exemptions or subsidized coverage. However, the specifics of these options vary significantly by state, as each state has its own Medicaid program and insurance marketplace. For instance, states that have expanded Medicaid under the ACA offer coverage to adults with incomes up to 138% of the federal poverty level (FPL), while non-expansion states often limit eligibility to much lower income thresholds, leaving a coverage gap for many low-income residents.

Analytical Perspective:

States like California and New York have embraced Medicaid expansion, providing comprehensive coverage to low-income adults, including preventive care, prescription drugs, and mental health services. In contrast, states like Texas and Florida have not expanded Medicaid, leaving millions of low-income individuals without affordable options. This disparity highlights the critical role state policies play in determining access to healthcare. For example, in California, a single adult earning up to $18,754 annually (138% of FPL) qualifies for Medi-Cal (California’s Medicaid program), while in Texas, eligibility is restricted to parents with incomes below 17% of FPL, or roughly $4,600 annually.

Instructive Approach:

To navigate state-specific insurance options, low-income individuals should first check their state’s Medicaid eligibility criteria. If ineligible for Medicaid, they can explore subsidized plans through their state’s health insurance marketplace. For example, in Colorado, individuals earning between 138% and 400% of FPL may qualify for premium tax credits, reducing monthly premiums significantly. Practical steps include using the Healthcare.gov tool to determine eligibility and comparing plans based on coverage, costs, and provider networks. Additionally, some states offer Basic Health Programs (BHPs), like Minnesota’s MinnesotaCare, which provides low-cost coverage to residents earning up to 200% of FPL.

Comparative Analysis:

While Medicaid expansion states generally offer broader coverage, non-expansion states often rely on alternative programs to fill the gap. For instance, Utah implemented a partial expansion with federal waivers, extending Medicaid to individuals earning up to 100% of FPL but requiring enrollees to pay premiums. Meanwhile, Arkansas’s "private option" model uses Medicaid funds to purchase private insurance for low-income residents. These variations underscore the importance of understanding state-specific programs, as they can significantly impact affordability and coverage levels.

Descriptive Example:

In Washington State, low-income residents have access to Apple Health, the state’s Medicaid program, which covers adults earning up to 138% of FPL. Additionally, the state offers Cascade Care plans for those who don’t qualify for Medicaid but still need affordable coverage. These plans include standardized benefits and cap out-of-pocket costs at $1,600 annually for individuals. Washington also provides financial assistance for premiums and cost-sharing reductions, making coverage more accessible for low-income families. This comprehensive approach serves as a model for other states seeking to expand healthcare access.

Persuasive Takeaway:

Oregon's Health Insurance Pioneer: Unveiling the State's First Provider

You may want to see also

Frequently asked questions

While the Affordable Care Act (ACA) mandates most individuals to have health insurance, low-income individuals may qualify for exemptions if coverage is considered unaffordable or if they fall within certain income thresholds.

Low-income individuals can access health insurance through Medicaid, the Children’s Health Insurance Program (CHIP), or subsidized plans available on the Health Insurance Marketplace, depending on their state and income level.

Penalties for not having health insurance were eliminated at the federal level starting in 2019, but some states (like California, New Jersey, and Massachusetts) have their own mandates and may impose penalties for lacking coverage.

No, while Medicaid is a primary option, low-income individuals may also qualify for subsidized plans through the Health Insurance Marketplace or receive free or low-cost care through community health centers.