When considering whether Aetna POS II insurance is better, it’s essential to evaluate its flexibility, coverage, and cost compared to other plans. Aetna POS II, a Point of Service plan, combines features of both HMO and PPO models, allowing members to choose in-network providers for lower costs or out-of-network providers with higher out-of-pocket expenses. This plan often appeals to those seeking a balance between managed care and freedom of choice. However, whether it’s better depends on individual needs, such as preferred doctors, budget constraints, and health requirements. Comparing it to alternatives like HMO or PPO plans can help determine if its benefits align with personal priorities.

Explore related products

What You'll Learn

![]()

Coverage Comparison: POS II vs. Other Plans

When comparing Aetna's POS II plan to other insurance options, it's essential to understand the unique features and coverage levels that set it apart. POS (Point of Service) plans, in general, offer a hybrid approach, combining elements of both HMO (Health Maintenance Organization) and PPO (Preferred Provider Organization) plans. Aetna's POS II plan is designed to provide policyholders with flexibility and comprehensive coverage, making it a popular choice for those seeking a balance between cost and accessibility.

In terms of provider networks, POS II typically allows members to choose from a broad network of healthcare providers, similar to a PPO. However, to maximize benefits, policyholders are encouraged to select in-network providers, a trait borrowed from HMO plans. This network flexibility is a significant advantage over HMO plans, which often restrict members to a specific group of providers. When compared to PPOs, POS II may offer more cost savings when staying within the network, making it an attractive option for those who prioritize both choice and affordability.

Coverage for services is another critical aspect of the comparison. Aetna's POS II plan usually covers a wide range of medical services, including preventive care, specialist visits, and hospitalization. Similar to PPOs, it provides coverage for out-of-network providers, although at a higher cost to the policyholder. This is in contrast to HMO plans, which often provide little to no coverage for out-of-network services. For individuals who require specialized care or prefer the freedom to choose providers outside the network, POS II offers a more comprehensive solution than HMO plans, while still providing better in-network rates compared to PPOs.

The cost structure of POS II plans is an essential factor in the comparison. These plans often feature lower premiums than PPOs, making them a more budget-friendly option for individuals and families. While HMO plans might offer even lower premiums, the restricted provider network can be a significant drawback. POS II plans strike a balance by providing competitive premiums and the flexibility to access out-of-network providers, albeit with higher out-of-pocket costs. This cost-effectiveness, combined with comprehensive coverage, makes POS II a strong contender against both HMO and PPO plans.

Lastly, referral requirements differentiate POS II from other plans. Like HMO plans, POS II may require a referral from a primary care physician to see a specialist, ensuring coordinated care. This is in contrast to PPO plans, which typically allow members to self-refer to specialists. While some may view this as a limitation, it can lead to better-managed care and potentially lower costs. For those who value a more guided healthcare approach, POS II offers a structured system that can be advantageous over the more open-ended PPO model.

In the context of 'does Aetna POS II in insurance better', the plan's ability to merge the benefits of HMO and PPO structures makes it a compelling choice. It provides the network flexibility of a PPO with the cost-saving incentives of an HMO, all while offering comprehensive coverage. For individuals seeking a balanced insurance option, POS II presents a strong case, especially when considering the trade-offs of other plan types. This comparison highlights how POS II can be a superior choice for those who want both freedom and value in their healthcare coverage.

Whole Life Insurance: Two Major Drawbacks

You may want to see also

Explore related products

![]()

Out-of-Pocket Costs: Deductibles, Copays, Coinsurance

When considering Aetna POS II insurance, understanding out-of-pocket costs is crucial for evaluating whether it’s a better option for your healthcare needs. Out-of-pocket costs primarily include deductibles, copays, and coinsurance, each playing a distinct role in how much you pay for medical services. A deductible is the amount you must pay out of pocket before your insurance coverage kicks in. With Aetna POS II, the deductible varies based on the plan, but it typically applies to most services except preventive care, which is often covered at 100%. Knowing your deductible is essential because until it’s met, you’ll be responsible for the full cost of most medical services, except for those with a copay.

Copays are fixed amounts you pay for specific services, such as doctor visits or prescription medications, regardless of whether you’ve met your deductible. Aetna POS II plans often have lower copays for in-network providers, making it cost-effective to stay within the network. However, out-of-network services may require you to pay the full cost until your deductible is met, followed by coinsurance. Coinsurance is the percentage of costs you share with the insurance company after the deductible is paid. For example, if your plan has 80/20 coinsurance, Aetna pays 80% of the cost, and you pay 20%. Understanding these cost-sharing mechanisms is key to determining if Aetna POS II aligns with your budget and healthcare usage.

One advantage of Aetna POS II is its flexibility in combining features of both HMO and PPO plans. This flexibility can influence out-of-pocket costs, as you can choose to use in-network providers for lower costs or go out-of-network with higher out-of-pocket expenses. For instance, in-network services often have lower deductibles and copays, while out-of-network services may require you to pay more upfront and have higher coinsurance rates. If you frequently see specialists or prefer out-of-network providers, the higher out-of-pocket costs associated with out-of-network care under Aetna POS II may be a significant factor in your decision.

Another aspect to consider is how Aetna POS II handles preventive care, which is often exempt from deductibles and may have no copay. This can reduce your overall out-of-pocket costs if you prioritize regular check-ups and screenings. However, for non-preventive services, the deductible and coinsurance structure will directly impact your expenses. Comparing these costs to other plans can help you determine if Aetna POS II offers better value based on your anticipated healthcare needs.

Finally, it’s important to review the annual out-of-pocket maximum for Aetna POS II plans. This cap limits the total amount you’ll pay for covered services in a year, providing financial protection against high medical expenses. If you have chronic conditions or anticipate significant medical needs, a plan with a lower out-of-pocket maximum may be more beneficial. By carefully examining deductibles, copays, coinsurance, and the out-of-pocket maximum, you can assess whether Aetna POS II is a better insurance option for managing your healthcare costs effectively.

Life Insurance Trusts: Defective Income for Beneficiaries?

You may want to see also

Explore related products

![]()

Provider Network: In-Network vs. Out-of-Network Benefits

When considering Aetna POS II insurance, understanding the differences between in-network and out-of-network benefits is crucial for maximizing your coverage and minimizing out-of-pocket costs. The provider network is a key component of this plan, as it determines the level of coverage you receive based on where you seek care. In-network providers have agreements with Aetna to offer services at pre-negotiated rates, which generally result in lower costs for the insured. Out-of-network providers, on the other hand, do not have such agreements, often leading to higher expenses for the policyholder. Aetna POS II typically covers a larger portion of the costs for in-network services, making it financially advantageous to stay within the network whenever possible.

In-network benefits under Aetna POS II are designed to provide comprehensive coverage with lower copays, coinsurance, and deductibles. When you visit an in-network provider, the plan’s cost-sharing structure is more favorable, meaning you pay less out of pocket for services. Additionally, in-network providers handle claims submissions directly with Aetna, simplifying the billing process for you. This streamlined approach reduces the likelihood of unexpected bills and ensures that you receive the full benefits of your insurance plan. Staying in-network also means you’re more likely to have preventive care services fully covered, as required by the Affordable Care Act.

Out-of-network benefits, while available under Aetna POS II, come with higher costs and more complex processes. When you see an out-of-network provider, you may be responsible for a larger portion of the bill, including higher deductibles and coinsurance rates. Additionally, out-of-network providers may charge more than the allowed amount, leaving you with a balance bill—the difference between what the provider charges and what Aetna agrees to pay. Unlike in-network providers, out-of-network providers may require you to submit claims manually, adding an extra layer of administrative burden. These factors make out-of-network care less cost-effective and more cumbersome to manage.

One of the advantages of Aetna POS II is its flexibility, allowing you to see out-of-network providers if necessary, though at a higher cost. However, it’s important to weigh the convenience of out-of-network care against the financial implications. If you choose to go out-of-network, ensure the provider is worth the additional expense and understand the potential for balance billing. Aetna POS II may also require prior authorization for certain out-of-network services, so it’s essential to check your plan details before proceeding. This flexibility can be beneficial in situations where in-network options are limited, but it’s generally more cost-effective to prioritize in-network providers.

To make the most of your Aetna POS II plan, regularly review the provider network directory to identify in-network doctors, specialists, and facilities. Planning ahead and choosing in-network providers can significantly reduce your healthcare expenses and simplify the claims process. If you have a preferred provider who is out-of-network, consider discussing your options with them or Aetna to explore potential solutions. Understanding the in-network vs. out-of-network benefits of your Aetna POS II plan empowers you to make informed decisions that align with your healthcare needs and financial goals.

Haven Insurance Retreat Offices: Innovative Workspaces for Productivity and Wellness

You may want to see also

Explore related products

![]()

Prescription Drug Coverage: Tiers and Costs

When considering prescription drug coverage under Aetna POS II, it’s essential to understand how the plan organizes medications into tiers and how these tiers impact out-of-pocket costs. Most insurance plans, including Aetna POS II, categorize prescription drugs into tiers based on their cost and therapeutic value. Typically, these tiers range from Tier 1 (generic drugs) to Tier 4 or 5 (specialty medications). Tier 1 drugs are the most affordable, often requiring only a small copayment, while Tier 4 and 5 drugs, which are usually brand-name or specialty medications, come with higher copays or coinsurance. Understanding these tiers is crucial for managing prescription costs effectively.

Aetna POS II often provides comprehensive coverage for Tier 1 and Tier 2 drugs, which include generic and preferred brand-name medications, respectively. Generic drugs (Tier 1) are the most cost-effective option and are typically covered with a minimal copay. Preferred brand-name drugs (Tier 2) are slightly more expensive but still more affordable than non-preferred brands. Members should prioritize medications within these tiers whenever possible to minimize costs. Aetna’s formulary, which lists covered drugs and their tier placements, is a valuable resource for determining the most cost-effective options for your prescriptions.

Non-preferred brand-name drugs (Tier 3) and specialty medications (Tier 4 or 5) often require higher out-of-pocket costs under Aetna POS II. These medications may necessitate prior authorization or step therapy, where the insurer requires you to try a lower-cost alternative before approving coverage for a more expensive drug. For specialty medications, which treat complex or rare conditions, coinsurance rates can be as high as 30% or more, depending on the plan. It’s important to review your plan’s specifics and discuss alternatives with your healthcare provider to manage these costs.

Another factor to consider is the plan’s deductible and out-of-pocket maximum. Some Aetna POS II plans may require you to meet a deductible before prescription drug coverage kicks in, particularly for higher-tier medications. However, once the out-of-pocket maximum is reached, the plan covers all additional prescription costs for the remainder of the year. This can provide significant financial relief for individuals with high medication needs. Reviewing your plan’s deductible and out-of-pocket limits is essential for budgeting and understanding your potential expenses.

Lastly, Aetna POS II may offer additional cost-saving programs, such as mail-order pharmacies or manufacturer coupons, to reduce prescription drug costs. Mail-order services often provide a 90-day supply of medication at a lower cost than retail pharmacies, making them an excellent option for maintenance medications. Manufacturer coupons or patient assistance programs can also offset the cost of expensive brand-name or specialty drugs. By leveraging these programs and understanding the tier system, Aetna POS II members can optimize their prescription drug coverage and minimize out-of-pocket expenses.

Supplemental Life Insurance: Enhancing Your Coverage and Peace of Mind

You may want to see also

Explore related products

![]()

Preventive Care: Free Services and Wellness Programs

Preventive care is a cornerstone of maintaining good health, and Aetna POS II insurance plans excel in this area by offering a robust suite of free services and wellness programs. Under this plan, members have access to a wide range of preventive care services at no out-of-pocket cost, including annual check-ups, vaccinations, and screenings for conditions such as cancer, diabetes, and heart disease. These services are designed to detect potential health issues early, when they are most treatable, and to promote overall well-being. By covering these essential services fully, Aetna POS II ensures that policyholders can take proactive steps toward their health without worrying about additional expenses.

One of the standout features of Aetna POS II is its emphasis on wellness programs that go beyond traditional medical care. Members can participate in programs focused on nutrition, fitness, stress management, and smoking cessation, often at no additional cost. These programs are tailored to individual needs and may include access to health coaches, digital fitness tools, and educational resources. For example, the Aetna HealthSM app provides personalized wellness plans, activity tracking, and reminders for preventive screenings, empowering members to take charge of their health in a convenient and engaging way.

In addition to wellness programs, Aetna POS II offers free preventive services for all age groups, including children and adults. For children, this includes immunizations, developmental screenings, and vision and hearing tests. Adults benefit from services like mammograms, colonoscopies, and blood pressure screenings, all covered at 100%. These services align with guidelines from organizations like the U.S. Preventive Services Task Force (USPSTF), ensuring that members receive evidence-based care that meets national standards.

Another advantage of Aetna POS II is its flexibility in accessing preventive care. Members can visit in-network providers without a referral, making it easier to schedule and attend preventive appointments. Additionally, the plan often covers telehealth services for preventive consultations, allowing individuals to receive care from the comfort of their homes. This accessibility is particularly beneficial for those with busy schedules or limited mobility, removing barriers to staying on top of their health.

Finally, Aetna POS II integrates preventive care with broader health management tools, such as health risk assessments and personalized care plans. These tools help identify potential health risks and provide actionable steps to mitigate them. By combining free preventive services with comprehensive wellness programs, Aetna POS II not only helps members avoid costly health issues down the line but also fosters a culture of proactive health management. This holistic approach makes Aetna POS II a strong contender for those seeking better insurance coverage that prioritizes preventive care and long-term wellness.

Misrepresentation in Life Insurance: Understanding the Fine Print

You may want to see also

Frequently asked questions

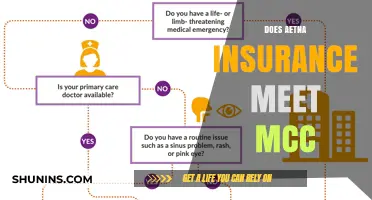

Aetna POS II is a type of Point of Service (POS) health insurance plan offered by Aetna. It combines features of both Health Maintenance Organization (HMO) and Preferred Provider Organization (PPO) plans, allowing members to choose in-network providers for lower costs or go out-of-network with higher out-of-pocket expenses.

Aetna POS II can be better than a traditional HMO plan for those who want more flexibility in choosing healthcare providers. Unlike HMOs, which typically require you to stay within a network and choose a primary care physician, POS II allows you to see out-of-network providers, though at a higher cost.

Aetna POS II is similar to a PPO in that both allow you to see out-of-network providers. However, POS II typically requires you to choose a primary care physician and get referrals for specialists, whereas PPOs usually do not have these requirements. POS II may offer lower premiums compared to PPOs.

Yes, Aetna POS II often has lower premiums compared to PPO plans. Additionally, staying within the network can result in lower copays and coinsurance. However, out-of-network care can be significantly more expensive, so it’s important to weigh your healthcare needs and preferences.

Aetna POS II is ideal for individuals who want the flexibility to see out-of-network providers occasionally but prefer the cost savings of staying in-network most of the time. It’s also a good option for those who are comfortable with having a primary care physician coordinate their care and provide referrals for specialists.