All-risk insurance, also known as comprehensive insurance, covers any incident that is not explicitly excluded in the contract. This means that if an all-risk homeowner's policy does not specifically exclude flood coverage, the insurance company will cover flood damage. However, flood insurance is typically a separate policy from homeowners insurance, and it is essential to safeguard against financial losses resulting from flooding. The National Flood Insurance Program (NFIP) offers flood insurance to property owners, renters, and businesses, providing coverage for buildings, contents, or both. FEMA's Standard Flood Insurance Policy (SFIP) defines a flood as the partial or complete submersion of two or more acres of normally dry land or two or more properties by water. Understanding the specifics of your insurance policy and taking proactive measures to reduce flood damage are crucial steps in mitigating the financial impact of potential flooding events.

| Characteristics | Values |

|---|---|

| What does "all risk" insurance cover? | Any incident that isn't explicitly mentioned or omitted in the contract. |

| What is not covered by "all risk" insurance? | Any incident that is explicitly mentioned or omitted in the contract. |

| Can "all risk" insurance cover flood damage? | If the contract does not expressly exclude flood coverage, then the house will be covered in the event of flood damage. |

| What is flood insurance? | A separate policy that can cover buildings, the contents in a building, or both. |

| Who provides flood insurance? | The National Flood Insurance Program (NFIP) provides flood insurance to property owners, renters and businesses. |

| How many NFIP policyholders are there? | 4.7 million. |

| How much coverage does NFIP provide? | Nearly $1.3 trillion. |

| How much do policyholders receive on average? | From 2016-2021, flood insurance policyholders received claim payments averaging $68,000. |

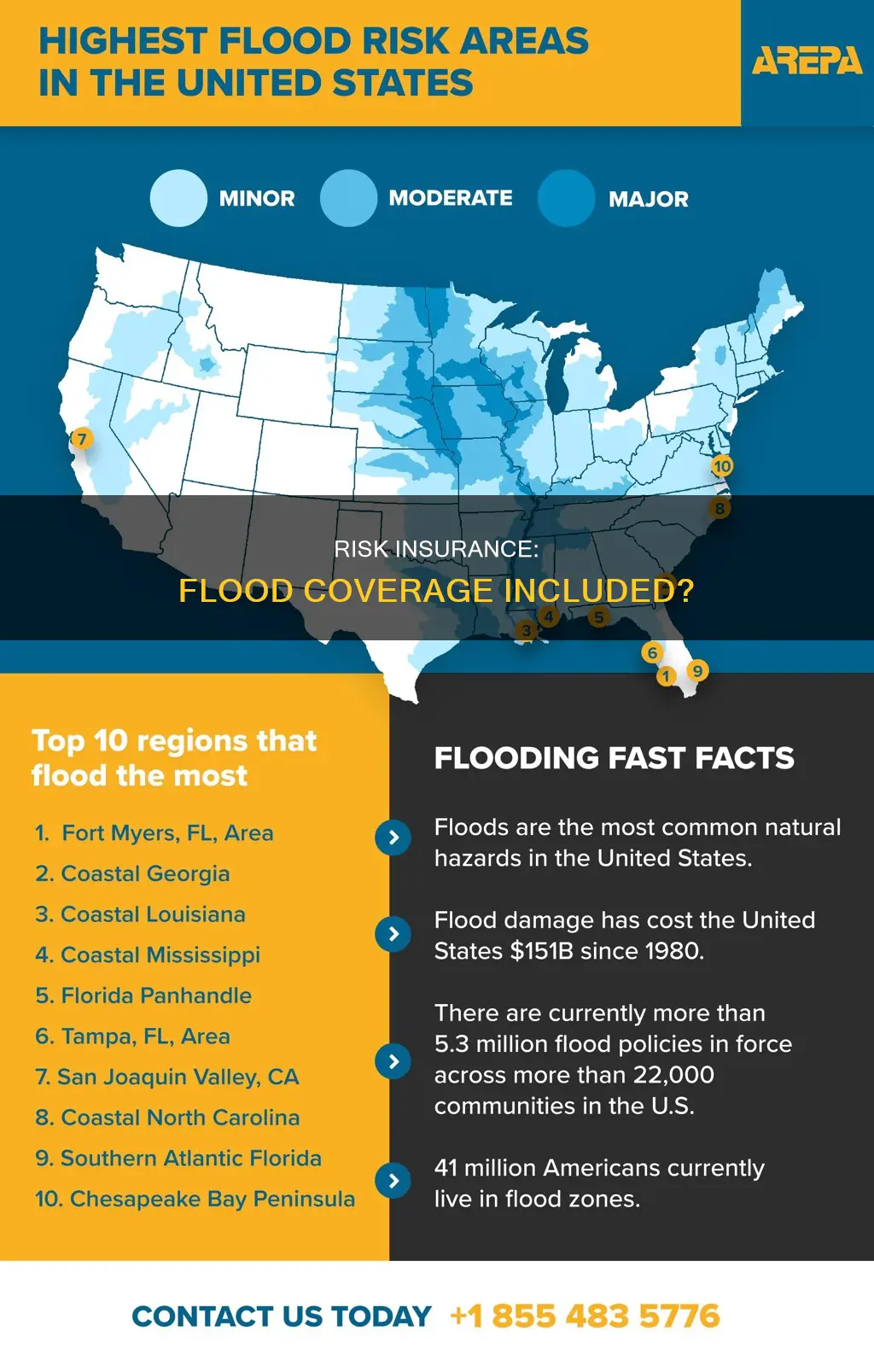

| How often do floods occur? | Flooding is the most common natural disaster. 99% of U.S. counties have seen floods. |

| How does flood insurance help? | Flood insurance helps policyholders recover faster when floodwaters recede. |

Explore related products

What You'll Learn

![]()

Flood insurance is a separate policy

Most homeowners insurance does not cover flood damage, and flood insurance is the only way to help you recover financially after a flood. Flooding is the most common and costly natural disaster, with 90% of presidentially declared US natural disasters involving flooding. Even outside high-risk zones, there is still a risk of flooding, and 40% of all flood claims occur in low- to moderate-risk areas.

The National Flood Insurance Program (NFIP) provides flood insurance to property owners, renters, and businesses, and is the nation's largest single-line insurance program, providing nearly $1.3 trillion in coverage against floods. The NFIP works with communities to adopt and enforce floodplain management regulations that help mitigate flooding effects. Flood insurance is available to anyone living in one of the 22,600 participating NFIP communities.

To purchase flood insurance, individuals can contact their insurance agent or company, or use the NFIP's insurance provider finder to locate an agent. FEMA also provides resources to help policyholders navigate the flood insurance process before, during, and after a disaster.

Avoid Your Parents' Insurance Mistakes

You may want to see also

Explore related products

![]()

All-risk insurance coverage

When it comes to all-risk insurance coverage, it's important to understand the difference between "named perils" and "all risks". A named perils insurance contract only covers the specific risks that are explicitly stated in the policy. For example, a policy might specify that any home loss caused by fire or vandalism will be covered. If a loss or damage is caused by a peril that is not named, the insured cannot file a claim. In contrast, an all-risks insurance contract covers all perils except those that are specifically excluded. This means that any risk not named in the exclusions is automatically covered.

The most common types of perils excluded from "all risks" coverage include earthquake, war, government seizure or destruction, wear and tear, infestation, pollution, nuclear hazard, and market loss. However, it's important to note that the exclusions can vary depending on the specific insurance provider and the type of coverage, such as property insurance or cargo insurance. For example, in the case of cargo insurance, all-risk coverage typically includes protection from financial loss due to the inability to meet contractual obligations, such as late shipments.

While all-risk insurance provides comprehensive coverage, it is important to remember that it does not cover every conceivable risk. There are still exclusions and limitations to this type of policy. Therefore, it is crucial to carefully review the fine print of any insurance agreement to understand what is and is not covered. Additionally, the cost of all-risk insurance should be considered in relation to the probability of making a claim.

In the context of flood insurance, it is important to note that most homeowners and renters insurance policies do not cover flood damage. Flood insurance is typically a separate policy that can be purchased through the National Flood Insurance Program (NFIP) or private insurance companies. While all-risk insurance may provide broader coverage compared to standard policies, it is essential to verify whether flood damage is specifically excluded from the policy.

Insurance Money: Where to Park Your Funds

You may want to see also

Explore related products

![]()

NFIP flood insurance

The National Flood Insurance Program (NFIP) is managed by FEMA and is delivered to the public by a network of more than 47 insurance companies and the NFIP Direct. The NFIP is a partnership between the federal government, the property and casualty insurance industry, states, local officials, lending institutions, and property owners.

The NFIP provides flood insurance to property owners, renters, and businesses, and having this coverage helps them recover faster when floodwaters recede. The NFIP works with communities required to adopt and enforce floodplain management regulations that help mitigate flooding effects. Flood insurance is available to anyone living in one of the 22,600 participating NFIP communities.

Flood insurance covers losses directly caused by flooding. Flood insurance is specific to flooding since most homeowners insurance does not cover flood damage. In simple terms, a flood is defined by FEMA's Standard Flood Insurance Policy (SFIP) as two or more acres of normally dry land or two or more properties that are partially or completely submerged by water. For example, damage caused by a sewer backup is covered if the backup is a direct result of flooding. In the event of a flood, your NFIP policy covers direct physical losses to your structure and belongings. The NFIP offers two types of coverage: building coverage and contents coverage. There are many circumstances that factor into what is covered, such as where you live, the kind of house you live in, the age of your home, and how it's built and arranged.

The NFIP uses many factors to evaluate a property's flood risk. The ground elevation where the building is located relative to the elevation of the surrounding area and nearby flooding sources is considered. Risk is greater for foundations underground or at ground level than those elevated above the ground. Flood risk is lower for buildings with first floors that are higher off the ground. Buildings with more floors spread flood risk over a larger area. Individual units on a building’s higher floors have a lower risk of flooding than units on lower floors. Masonry walls perform better in flooding events than wood frame walls. A building with flood openings can have a lower flood risk by allowing floodwaters to flow through the structure.

There are 4.7 million policyholders nationwide and the NFIP is the nation’s largest single-line insurance program, providing nearly $1.3 trillion in coverage against floods.

Building a Commercial Insurance Book: Strategies for Success

You may want to see also

Explore related products

![]()

Flood insurance claims

Flood insurance is a separate policy from homeowners' insurance and is often essential as flooding can cause thousands of dollars' worth of damage. Flood insurance can cover buildings, possessions within a building, or both. The National Flood Insurance Program (NFIP) provides flood insurance to property owners, renters, and businesses, and nearly one-third of NFIP claims are from outside the high-risk zones.

To purchase flood insurance, you can contact your insurance agent or company, or reach out to the NFIP directly. There is typically a 30-day waiting period for an NFIP policy to go into effect unless it is required immediately due to a government-backed lender or a community flood map change.

When filing a flood insurance claim, it is important to note that it may take longer to process claims and receive payments in cases of major catastrophic flooding due to the high volume of claims submitted. To receive your claim payment, you and the insurer must first agree on the amount of damage and the insurer must have your complete, accurate, and signed Proof of Loss.

FEMA's Standard Flood Insurance Policy (SFIP) defines a flood as "two or more acres of normally dry land or two or more properties that are partially or completely submerged by water". This is also referred to as a Special Flood Hazard Area (SFHA). If you own property in one of these high-risk zones and have a government-backed mortgage, you are required to purchase flood insurance.

Navigating the Path to Becoming an Insurance Adjuster in California: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Flood risk factors

Flooding is more common than many people think, with 99% of U.S. counties experiencing floods. Even those in areas of low risk should consider flood insurance, as 40% of all flood claims occur in low- to moderate-risk areas.

The National Flood Insurance Program (NFIP) uses many factors to evaluate a property's flood risk. These include the ground elevation of the building relative to the elevation of the surrounding area and nearby flooding sources. The risk is greater for foundations that are underground or at ground level, compared to those elevated above the ground. Buildings with more floors spread flood risk over a larger area, and individual units on higher floors have a lower risk of flooding than those on lower floors.

The specific depth and likelihood of flooding expected to reach a property are used to determine the boundaries for each level of flood risk. Properties with at least a 6% chance of flooding over 30 years will have a Flood Factor of 2 or higher. This increases as the chance of flooding increases, with properties with at least a 99% chance of flooding over 30 years having a Flood Factor of 6 or higher.

In communities that participate in the NFIP, flood insurance is mandatory for properties located in high-risk flood zones if mortgages are government-backed. Over a 30-year mortgage, homes in these areas have a 1 in 4 chance of flooding at least once.

Insurance Salesman: Strategies for Earning More

You may want to see also

Frequently asked questions

All-risk insurance, also known as comprehensive insurance, covers any incident that is not explicitly mentioned or omitted in the contract. It is priced higher than other types of policies due to the greater number of possible loss events covered.

All-risk insurance can include flood insurance if the contract does not expressly exclude it. However, it is important to carefully read the fine print of any insurance agreement to understand what is excluded. Most homeowners' insurance does not cover flood damage, so flood insurance is typically purchased separately.

Flood insurance can be purchased through the National Flood Insurance Program (NFIP), which offers policies to property owners, renters, and businesses. You can find an insurance provider through the NFIP website or by contacting an insurance agent. Keep in mind that there is typically a 30-day waiting period for an NFIP policy to take effect.