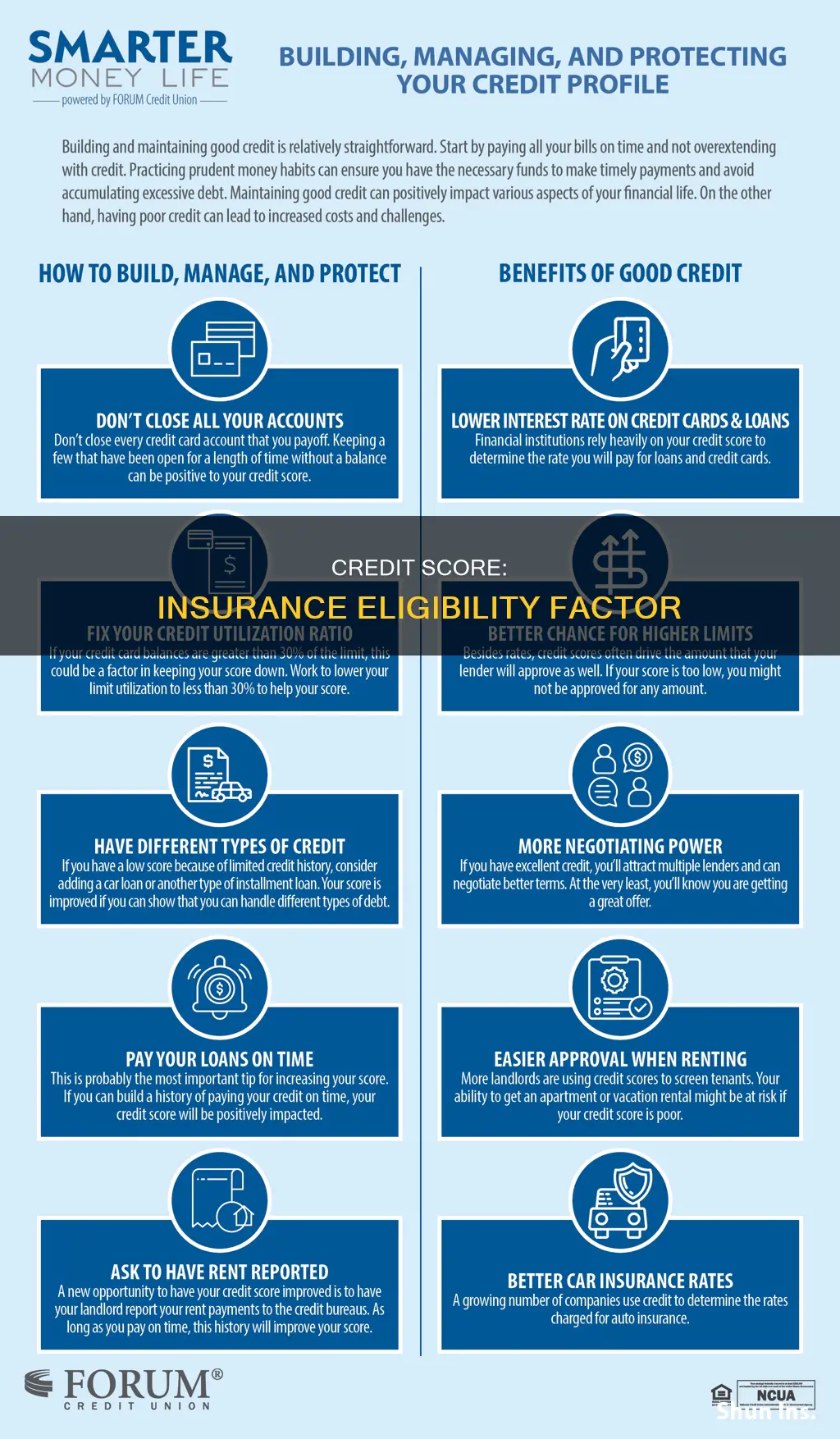

Credit scores are calculated based on multiple factors, including bankruptcies, debt, bill-paying habits, how long accounts have been open, and the amount of credit used on credit cards. A credit score predicts how likely you are to pay back a loan. Credit-based insurance scores are calculated using information from your credit report, but they are different from credit scores. Insurance companies use these scores to determine eligibility and premiums. While a low credit-based insurance score may not lead to a rejected application, it may result in a higher premium or monthly rate.

| Characteristics | Values |

|---|---|

| Credit score's impact on insurance eligibility | In most states, credit-based insurance scores can affect eligibility and premiums. |

| Factors insurance companies consider | How many open accounts you have, how much you owe compared to your available credit, any past due payments, how often you apply for new lines of credit, medical debts that went to collection, credit checks related to insurance coverage, credit checks from unsolicited businesses. |

| Improving credit score | Paying down debt, paying bills on time, reviewing credit report and reporting errors, automatic payments, careful spending |

| Credit-based insurance score | Calculated using information from your credit report but is different from your credit score. |

| Credit score range | Most credit scores range from 300-850. A higher score is better. |

| Obtaining credit report | The Fair and Accurate Credit Transaction Act of 2003 (FACT Act) allows consumers to obtain a free credit report once every 12 months from each of the three nationwide consumer credit reporting companies (Equifax, Experian, and TransUnion). |

Explore related products

What You'll Learn

![]()

Credit-based insurance scores are different from credit scores

Credit-based insurance scores are designed to predict the risk of loss for the insurer, while credit scores predict the likelihood of a borrower missing a bill payment. Credit-based insurance scores are used in the underwriting and rating of consumers. Underwriting is the process of determining eligibility for coverage, and rating is deciding how much premium to charge. Credit scores, on the other hand, are used to assess the likelihood of a borrower defaulting on a payment within the next 24 months.

The range of scores also differs between the two. Credit scores typically range from 300 to 850, while credit-based insurance scores can vary significantly, such as the LexisNexis Attract score, which ranges from 200 to 997.

The factors that influence these scores also differ. Credit-based insurance scores consider payment history, outstanding debt, credit history length, pursuit of new credit, and credit mix. They may also include non-credit data, such as information from public records. Credit scores also consider payment history and outstanding debt but may place more emphasis on negative information on credit reports, such as missed payments or defaults.

It's important to note that credit-based insurance scores and credit scores are both influenced by information in an individual's credit report. Therefore, maintaining a positive credit history and timely bill payments can positively impact both scores.

Understanding Commercial Auto Insurance: Who's Covered and Who's Not?

You may want to see also

Explore related products

![]()

Credit-based insurance scores determine premiums

In most states, insurance companies can use credit-based insurance scores to determine an individual's premiums. However, it is important to note that credit-based insurance scores are not the same as regular credit scores. While FICO, a data and analytics company that measures credit risk, states that many insurers use credit-based insurance scores in states where it is legally allowed, not all states permit their use in determining premiums. Some states only allow them as one factor for property insurance, such as auto and homeowners insurance, while others permit their use with any type of insurance. Thus, it is advisable to check with your state insurance department to understand the specific laws and regulations in your state.

Credit-based insurance scores are used by insurers primarily in the underwriting and rating of consumers. Underwriting is the process by which an insurer determines whether a consumer is eligible for coverage, while rating decides the premium amount to be charged. The credit-based insurance score models used by insurers are designed to predict the risk of loss. Insurers use these scores for underwriting to assign consumers to risk pools and then for rating to adjust the premium accordingly.

When determining an individual's credit-based insurance score, FICO considers five general areas that reflect how well an individual manages risk. These areas include payment history (40%), outstanding debt (30%), credit history length (15%), pursuit of new credit (10%), and credit mix (5%). Payment history evaluates an individual's track record of making payments on outstanding debts. Outstanding debt refers to the total amount of debt currently held. Credit history length considers the duration an individual has had access to credit. Pursuit of new credit examines recent applications for additional lines of credit. Finally, credit mix looks at the variety of credit types an individual possesses, such as credit cards, mortgages, or auto loans.

It is worth noting that insurance companies can only use credit-based insurance scores as one factor in their underwriting process. Several other factors come into play and vary depending on the type of insurance. For example, with auto insurance, insurers may also consider factors such as the age of the drivers, the make and model of the car, the annual mileage, and even the ZIP code. Additionally, insurance companies must disclose within 30 days if they deny coverage or charge higher premiums due to an individual's credit report. If your credit has been impacted by significant life events like illness, job loss, divorce, or identity theft, you can request the insurance company to reconsider and make an exception.

Auto Insurance Coverage for RVs: What You Need to Know

You may want to see also

Explore related products

![]()

Credit-based insurance scores affect eligibility

Credit-based insurance scores are not the same as a credit score. Insurers use this number because policyholders with good credit-based insurance scores generally file fewer or less expensive claims. In most states, insurers can use your credit-based insurance score to determine your premiums. It is worth noting that insurance companies cannot charge you more or deny you coverage if your credit score was hurt by events such as a major illness or injury, the death of a spouse, child, or parent, temporary job loss, a recent divorce, or identity theft.

Credit-based insurance scores are only one of many factors in these decisions, but they can sometimes have a significant impact. For example, with auto insurance, other factors could be your ZIP code, the age of the operators, the make, model, and age of your car, and even the miles you drive annually.

In the case that you receive an insurance quote and the insurance company does not offer you a policy or charges you a higher premium because of your credit, you should receive an adverse action notice. This notice might include the credit-based insurance score that the company used, along with the main factors that affected your score.

If you wait for at least one year following a bankruptcy, you may be able to get a better rate. Also, if you focus on improving your credit score by paying down debt and paying bills on time, you may also be able to improve your credit score and your insurance rates.

Gap Insurance: Protecting Your Auto Loan

You may want to see also

Explore related products

![]()

Credit-based insurance scores are one of many factors

Credit-based insurance scores are not the same as a credit score. They are one of many factors that insurance companies use to determine your eligibility for insurance and the amount of premium to be charged. Insurers use this number because policyholders with good credit-based insurance scores generally file fewer or less expensive claims.

In most states, insurers can use your credit-based insurance score to determine your premiums. However, insurance companies cannot charge you more or deny you coverage if your credit score was hurt by events such as a major illness or injury, the death of a spouse, child, or parent, temporary job loss, a recent divorce, or identity theft. You should receive an adverse action notice if you get an insurance quote and the insurance company doesn't offer you a policy or charges you a higher premium because of your credit.

Your credit-based insurance score can be affected by errors in your credit report. You can check your credit report annually for free on www.annualcreditreport.com. If you find any errors, you should contact the credit reporting company to have them corrected.

Other factors that insurance companies consider when determining your eligibility and premium include your ZIP code, the age of the operators, the make, model, and age of your car, and the miles you drive annually.

Hartford Auto Insurance: Claims Address and Process Explained

You may want to see also

Explore related products

![]()

Improving credit scores can lower insurance rates

While credit-based insurance scores are not the same as regular credit scores, improving your credit score can positively impact your insurance rates. In most states, insurers can use your credit-based insurance score to determine your premiums. This score is designed to predict the risk of loss and is used in the underwriting and rating processes. Underwriting assesses eligibility, while rating determines the premium charged.

A low credit score can significantly increase your insurance rates. For instance, drivers with poor credit scores pay, on average, $1,500 more in insurance annually than those with perfect scores. In addition, drivers with poor credit histories may face challenges in securing insurance coverage, as they are often viewed as high-risk.

However, improving your credit score can help lower your insurance rates. Here are some strategies to achieve this:

- Make timely payments on outstanding debts, bills, taxes, and fines/fees.

- Keep credit card balances low relative to your credit limit to demonstrate good credit utilization habits.

- Minimize hard inquiries on your credit report.

- Diversify your credit by responsibly managing a mix of credit accounts, such as credit cards, loans, and mortgages.

- Request a credit limit increase from your credit card issuer to decrease your utilization ratio without reducing your spending budget.

By implementing these strategies, you can improve your credit score, which may lead to lower insurance rates and better financial health.

High Blood Pressure: Heart Condition for Insurance Claims?

You may want to see also

Frequently asked questions

It depends. Insurance companies don't use credit scores directly. Instead, they use a credit-based insurance score, which is calculated using information from your credit report. This number is different from your credit score. In most states, your credit-based insurance score can affect your eligibility and premiums. However, insurance companies generally can't refuse to insure you or cancel your policy based solely on your credit.

A credit-based insurance score is calculated using information from your credit report. It is not the same as your regular credit score. FICO, one of the companies that creates credit-based insurance scores, looks at five general areas: payment history (40%), outstanding debt (30%), credit history length (15%), pursuit of new credit (10%), and credit mix (5%).

You can improve your credit-based insurance score by paying down debt and paying your bills on time. You should also review your credit report carefully and report any errors immediately.