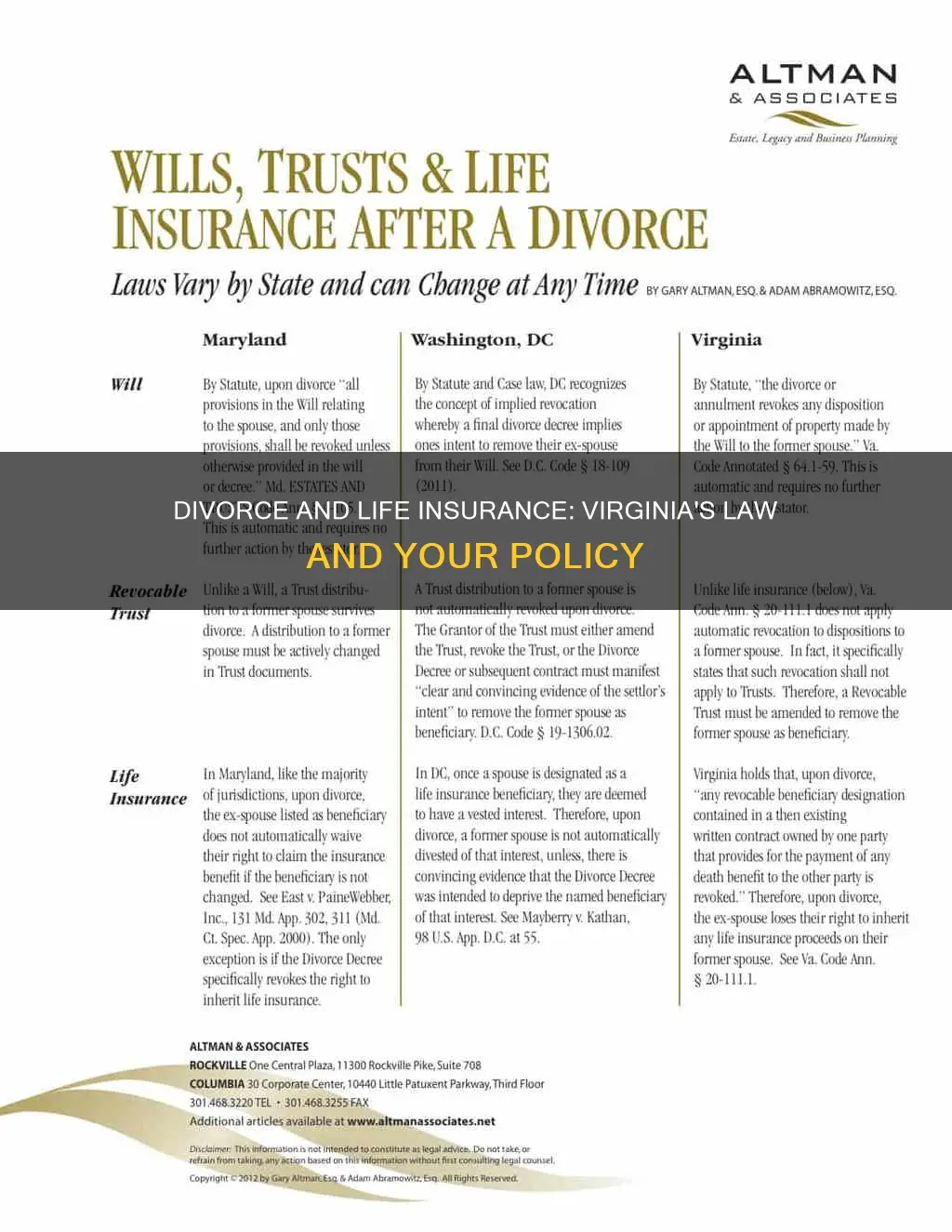

Life insurance is a critical aspect of divorce that can sometimes be overlooked. In Virginia, a life insurance policy is a contract between the insurer and the policy owner, who has the authority to designate the beneficiary. While the policy owner can often change the beneficiaries at any time, divorce can complicate this. Virginia law states that a revocable beneficiary designation naming the other spouse as a beneficiary becomes void upon divorce, unless specified otherwise. However, the court can order the maintenance of a life insurance policy, including the beneficiaries, in cases involving spousal support. This means that divorce may not always invalidate life insurance in Virginia, and the specific circumstances of each case must be considered.

| Characteristics | Values |

|---|---|

| Does divorce invalidate life insurance in Virginia? | No, Virginia does not have automatic revocation on divorce for life insurance policies. |

| Who can be a beneficiary of a life insurance policy after divorce? | The policy owner can designate their minor children as beneficiaries of the policy as part of a child support order. The former spouse can also be designated as a beneficiary in cases where there is a spousal support award. |

| What happens to cash-value life insurance policies during a divorce? | Cash-value life insurance policies are included with marital assets during the divorce process and the cash value is subject to division as part of a divorce settlement. |

| When can a life insurance policy be changed after divorce? | A life insurance policy can be updated or changed during the divorce process, subject to any restrictions placed by the court. After the divorce is complete, changes may need to be made to comply with a court order. |

| What are some potential problems with life insurance during a divorce? | The policyholder may change the beneficiary without informing the other person or stop paying the premiums, resulting in the policy's cancellation. |

Explore related products

What You'll Learn

![]()

Life insurance policies and divorce in Virginia

In Virginia, life insurance policies are a contract between the insurer and the policy owner, and the policy owner typically has the authority to designate beneficiaries and change or terminate the policy. However, in the event of a divorce, the treatment of life insurance policies can become more complex, especially when spousal support or child support is involved.

Life Insurance and Spousal Support

Virginia law allows the Court to mandate a life insurance policy for the entire term of a spouse's support obligation. This ensures that a surviving ex-spouse continues to receive their support obligation even if their former spouse passes away. This law came into effect in July 2017 and applies to both private and employer-provided insurance policies.

Beneficiary Designations

It is important to note that, in Virginia, divorce does not automatically revoke a former spouse's beneficiary status on a life insurance policy. The policy owner must physically change the beneficiary designation if they no longer wish for their ex-spouse to be a beneficiary. However, if there are children involved, they will likely become the beneficiaries, as many divorce decrees require this as a form of child support.

Cash Value Life Insurance Policies

Cash value life insurance policies are considered marital assets during a divorce and may be subject to division as part of a divorce settlement. Alternatively, the policy can be cancelled, and the cash value can be split between the divorcing spouses.

Role of the Court

The court may make rulings regarding life insurance policies during divorce proceedings. If a life insurance policy was purchased during the marriage, the court can order that the policy be maintained, even if the former spouse is listed as the beneficiary. The court will consider various factors when making these decisions, including the age, health, and insurability of both spouses, the cost of the policy, and the ability of either spouse to pay the premiums.

In summary, while divorce does not automatically invalidate life insurance policies in Virginia, it is important to review and make necessary changes to these policies during and after the divorce process, especially when there are children or spousal support obligations involved. Consulting with an experienced divorce lawyer in Virginia can provide valuable insights and help ensure the protection of one's family.

Life Insurance: Dearborn Police's Entitlement and Benefits

You may want to see also

Explore related products

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UL320_.jpg)

![]()

The Court's role in life insurance policies

In Virginia, the court plays a significant role in ensuring the protection of a spouse's interests in the event of a divorce. This is achieved through the court's ability to mandate life insurance policies and make determinations regarding the maintenance of existing policies.

Mandating Life Insurance Policies

In July 2017, a new law came into effect in Virginia that empowers the court to mandate a life insurance policy for the entire term of a spouse's support obligation. This means that the court can order one spouse to maintain a life insurance policy that names the other spouse as the beneficiary, ensuring they receive their support obligation even in the unfortunate event of the insured spouse's death.

Factors Considered by the Court

When making the decision to mandate a life insurance policy, the court takes into account several factors to ensure a fair and appropriate order:

- Age, health, and insurability of the insured spouse.

- Age and health of the beneficiary spouse.

- Cost of the life insurance policy.

- Amount and term of spousal support.

- Insurance rates at the time of the support order.

- Ability of either spouse to pay the insurance premium.

- Other factors deemed necessary by the court.

Maintenance of Existing Life Insurance Policies

Upon the entry of a decree for divorce, the court may also order a spouse to maintain an existing life insurance policy under certain conditions. The court can require the insured spouse to:

- Maintain any existing policy that was purchased during the marriage, is issued through their employment, or is within their effective control, provided they have the right to designate a beneficiary.

- Designate the other spouse as the beneficiary of the death benefit for as long as there is an obligation to pay spousal support, provided they have the right to make such a designation.

- Allocate the premium cost of the policy between the spouses, with all premiums billed to the policyholder.

- Execute the necessary forms or written consents to provide the beneficiary with information about the policy's status and their maintenance as the beneficiary.

It is important to note that any obligations under such an order would cease if the obligation to pay spousal support or separate maintenance ends.

Comcast's Life Insurance Offering: What You Need to Know

You may want to see also

Explore related products

![]()

Changing beneficiaries

In Virginia, a life insurance policy is a contract between the insurer and the policy owner, who generally has the authority to designate beneficiaries.

If you and your ex-spouse have children, they will likely become the beneficiaries of your policy. Many divorce decrees require beneficiary designations for children as a form of child support, although this does not replace child support payments during your lifetime.

If there are no children, you will need to update the beneficiary designation if you do not want your ex-spouse to remain a beneficiary. However, there may be situations where you cannot remove your ex-spouse, such as when:

- Alimony provisions in your divorce decree prohibit you from doing so.

- A prenuptial or divorce agreement requires you to include your ex-spouse as a beneficiary.

Regardless of any changes in beneficiary designations, you should notify your insurance company about your divorce as your new marital status may require updates to the policy.

You can update or change your policy during the divorce process, subject to any restrictions placed by the court. For example, a court might order you not to change any beneficiary designations while the divorce is pending unless it is part of a divorce settlement with your ex-spouse’s agreement. If you make changes to the policy despite a court order, the court could hold you in contempt.

After the divorce is complete, you may need to make changes to your coverage in order to comply with a court order. This might involve changing the beneficiary designations or obtaining new coverage. You can begin this process as soon as you are able.

Combined Insurance: Life Insurance Options and More

You may want to see also

Explore related products

![]()

Cash-value life insurance policies

In Virginia, divorce does not automatically revoke a life insurance policy. This means that if a person forgets to remove their ex-spouse as a beneficiary, they may still be entitled to the benefit. However, Virginia law does outline that a revocable beneficiary designation becomes void upon divorce.

Now, when it comes to cash-value life insurance policies, there are a few things to keep in mind. Firstly, cash-value life insurance is a type of permanent policy that can build funds over time through its cash value component. This cash value can be accessed while the policyholder is still alive and can be used to pay for necessary expenses. The two main components of this type of policy are the death benefit and the cash value. The death benefit is the amount that the beneficiaries will receive, while the cash value can be accessed early by taking out a loan against the policy, surrendering the policy, or making a withdrawal.

There are several types of life insurance policies that offer cash value, including whole life, universal, variable, and indexed life insurance. Each policy type accrues cash value differently, and it's important to understand these differences when making a decision. For example, with whole life insurance, the cash value can grow over time with potential tax savings, and the premiums are usually fixed. On the other hand, universal life insurance offers more flexibility, as it allows the policyholder to change the value of premium payments. The cash value in this type of policy can be used to pay premiums or cover other expenses.

Variable life insurance provides greater access to investment tools, but it also involves more risk since the cash value depends on the performance of the chosen investments. Indexed life insurance, on the other hand, is closely tied to the stock market, and the chosen index will directly impact the rate of return on the cash value.

When considering a cash-value life insurance policy, it's important to weigh the benefits and drawbacks. One advantage is that it offers lifelong coverage, ensuring that your loved ones will receive a death benefit payout regardless of when you pass away. Additionally, the cash value can be used to pay for future expenses, such as college tuition or retirement costs. However, cash-value life insurance typically comes with higher premiums compared to term life insurance, and it may take a significant amount of time to build up a substantial cash value.

CVS and Tricare: Insurance and Life Coverage Options

You may want to see also

Explore related products

![]()

Health insurance after divorce

In Virginia, while divorce proceedings are ongoing, the law protects both spouses from losing their health insurance benefits. This means that if one spouse tries to end coverage for their dependent spouse while the divorce is pending, the court may make the violating spouse liable for the uninsured medical costs incurred by the dependent spouse. However, if there is a good reason to remove the dependent spouse from the health insurance policy, the insured spouse may petition the court for permission.

Once the divorce is finalized, the two parties are no longer legally related, and the dependent ex-spouse can no longer remain on their ex's health insurance policy. This means that the dependent spouse will need to look for alternative health coverage options. Here are some options for health insurance after divorce:

- Health insurance through their own employer: Divorce is a life-changing event that allows individuals to sign up for health insurance outside of the usual open enrollment period. The window to sign up is typically around 30 days after the divorce is finalized.

- Temporary COBRA coverage: Under the Consolidated Omnibus Budget Reconciliation Act (COBRA), a person can keep their ex-spouse's policy for up to 36 months. They must notify the administrator of their ex-spouse's health insurance plan within 60 days of the divorce. However, employers typically do not subsidize this additional coverage, so the full premium must be paid.

- Private health insurance: Private health insurance plans can be very expensive, especially with pre-existing conditions. The cost of private insurance should be considered when determining spousal support.

If the couple has children, their health insurance coverage should be included in the child support agreement. The Virginia Child Support Guidelines Worksheet is used to calculate child support payments and specifically includes healthcare coverage in the computation. If the dependent spouse opts for COBRA coverage, their children may also be included.

Citibank's Life Insurance Offer: What You Need to Know

You may want to see also

Frequently asked questions

No, Virginia is one of the few states that does not have an automatic revocation on divorce for life insurance policies. However, the policyholder can change the beneficiary or revoke the policy themselves.

Yes, the court can order a policyholder to maintain an existing life insurance policy and designate their minor children as beneficiaries as part of a child support order. The court can also require the maintenance of life insurance policies and beneficiaries, including a former spouse, in cases where spousal support is awarded.

A cash-value life insurance policy is included with marital assets during the divorce process and the cash value is subject to division as part of a divorce settlement. Alternatively, the policy can be cancelled, and the cash value can be split between the former spouses.