Life insurance is a valuable benefit for employees, but it's important to understand the tax implications. If your employer provides group term life insurance as part of your benefits package, the first $50,000 of coverage is typically excluded from taxable income. However, if the coverage exceeds $50,000, the additional amount becomes taxable income, often resulting in higher taxes. This is known as phantom income because it increases your tax liability without providing you with any tangible funds. The details of employer-paid life insurance and its tax consequences are essential for employees to understand, especially when considering their compensation and overall financial situation.

Explore related products

What You'll Learn

![]()

The first $50,000 of employer-paid life insurance is not taxed

If your employer provides you with group term life insurance, you may consider it a desirable fringe benefit. However, while the first $50,000 of employer-paid life insurance is not taxed, coverage above this amount can have undesirable income tax consequences.

IRC section 79 states that the first $50,000 of group-term life insurance coverage provided under a policy carried directly or indirectly by an employer is excluded from taxable income. This means that if your employer pays for your group term life insurance, the first $50,000 of coverage will not be taxed, and will not add anything to your income tax bill.

However, if your employer-provided coverage exceeds $50,000, the cost of coverage above this amount is considered taxable income and must be included in your taxable wages reported on Form W-2. This is known as "phantom income" because it increases your taxable income even though you never actually receive the money. The cost of coverage is determined by a table prepared by the IRS, and this amount is used to calculate your taxable income, even if your employer's actual cost is lower.

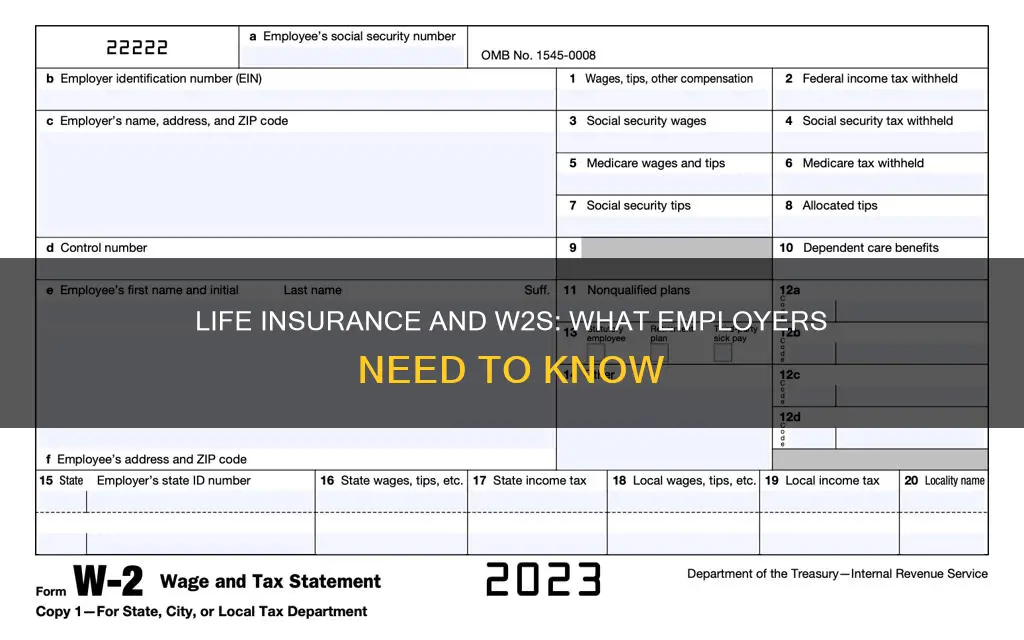

If you are concerned about the tax implications of your employer-provided life insurance, you can check Box 12 of your Form W-2 for a specific dollar amount with code "C". This amount represents your employer's cost for providing you with group-term life insurance coverage in excess of $50,000, minus any amount you paid for the coverage. You will be responsible for paying federal, state, and local taxes on this amount, as well as associated Social Security and Medicare taxes.

It is important to note that the amount in Box 12 is already included in your total "Wages, tips and other compensation" in Box 1 of the W-2, and it is the Box 1 amount that is reported on your tax return. If you feel that the tax cost of your employer-provided life insurance is too high, you may want to explore options such as carve-out" plans or purchasing an individual policy.

CVS and Tricare: Insurance and Life Coverage Options

You may want to see also

Explore related products

![]()

Taxable income above $50,000 is phantom income

If your employer provides life insurance as part of your benefits package, it's likely a welcome fringe benefit. However, if the coverage is above $50,000, there may be some undesirable tax implications. The first $50,000 of group term life insurance coverage that your employer provides is excluded from taxable income and won't affect your tax bill. But if your employer-provided coverage exceeds $50,000, this is where the concept of "phantom income" comes into play.

Phantom income is taxable income that you've been allocated but haven't physically received. In the context of employer-paid life insurance, if your coverage exceeds $50,000, the excess coverage cost is considered taxable income and is included in the taxable wages on your W-2 form. This amount is determined by an IRS Premium Table, and even if your employer's actual cost is lower, your taxable income is based on the predetermined table value. This predetermined value often results in a higher taxable income amount than what you would have paid for similar coverage under an individual term policy.

Implications of Phantom Income

The inclusion of this phantom income in your taxable wages can have several consequences. Firstly, it increases your taxable income, which can push you into a higher tax bracket and result in a higher tax liability. Secondly, you become responsible for paying federal, state, and local taxes on this phantom income, as well as associated Social Security and Medicare taxes. This situation can become more challenging as you get older and your compensation increases, making it a worsening tax trap.

Managing Phantom Income

If you find yourself facing a high tax cost due to employer-provided life insurance, there are a few strategies you can consider:

- Carve-out Plans: Ask your employer if they have or would be willing to create a carve-out plan, which excludes selected employees from group term coverage above $50,000. This way, you still get the benefit of the first $50,000 of coverage without the tax implications of excess coverage.

- Individual Policy: Your employer could provide you with an individual policy for the balance of the coverage above $50,000. This separates the taxable portion and helps mitigate the tax burden.

- Cash Bonus: Alternatively, your employer could give you a cash bonus equivalent to the amount they would have spent on the excess coverage. You can then use this bonus to pay the premiums on an individual policy.

Drug Use and Life Insurance: What's the Connection?

You may want to see also

Explore related products

![]()

This is reported in Box 12 of the W-2 form

If your employer provides you with life insurance, it is likely considered a fringe benefit. The first $50,000 of group term life insurance coverage that your employer provides is excluded from taxable income and won't add anything to your income tax bill. However, if the cost of your employer-provided group term life insurance coverage exceeds $50,000, this additional amount is considered taxable income and must be included in the taxable wages reported on your Form W-2. This is often referred to as "phantom income" because it increases your tax liability even though you never actually receive the money.

The taxable amount is reported in Box 12 of the W-2 form, with a specific code (usually "C"). This dollar amount represents your employer's cost of providing you with group term life insurance coverage in excess of $50,000, less any amount you paid for the coverage. It is important to note that this amount is already included in your total "Wages, tips and other compensation" in Box 1 of the W-2, and it is the Box 1 amount that is reported on your tax return.

The cost of group term life insurance coverage for tax purposes is determined by a table prepared by the IRS, even if your employer's actual cost is lower. As a result, older employees may find that the amount of phantom income they are taxed for is higher than what they would pay for similar coverage under an individual term policy.

If you believe that the tax cost of your employer-provided group term life insurance is too high, you can explore the option of a "carve-out" plan. A carve-out plan allows selected employees to opt-out of the group term coverage and choose an individual policy or receive a cash bonus to pay the premiums for an individual policy.

It is always a good idea to review your W-2 form carefully and consult with a tax professional if you have any questions or concerns about the tax implications of your employer-provided benefits.

Chest Pain: Can It Impact Your Life Insurance Eligibility?

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UL320_.jpg)

![]()

Employers can offer carve-out plans to reduce employee tax burden

Life insurance provided by an employer is generally considered a desirable fringe benefit. However, if the coverage provided exceeds $50,000, it may lead to undesirable income tax implications for the employee. This is because the cost of coverage above $50,000 is considered taxable income and is included in the employee's Form W-2, even though they did not actually receive this amount. This is often referred to as "phantom income". As a result, employees may end up paying higher taxes than they would have if they had purchased an individual term policy.

To address this issue, employers can offer "carve-out" plans, which are designed to reduce the tax burden on employees while still providing valuable life insurance benefits. A carve-out plan allows employers to select certain employees to be excluded from group term coverage. Here are two common ways in which a carve-out plan can be structured:

- The employer continues to provide group term insurance coverage up to $50,000, which is the maximum amount that is not considered taxable income for the employee. For the remaining coverage amount, the employer provides the employee with an individual policy. This individual policy is typically portable and can accumulate cash value over time, offering additional benefits to the employee.

- The employer provides the employee with a cash bonus equivalent to the amount they would have spent on the excess coverage. The employee can then use this bonus to pay the premiums for an individual policy of their choice.

By implementing a carve-out plan, employers can help their employees reduce their tax liability while still offering attractive life insurance benefits. This can be a valuable tool for retaining key employees and ensuring they feel valued by the company. Additionally, employers may also receive tax deductions for the premiums they pay for the group term life insurance and, in some cases, for the employee's individual policy as well.

Life Insurance and DSHS: Counting Assets and Impact

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

$114.99

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)

![]()

Group insurance is less expensive than individual policies

Group insurance is typically offered by employers to their employees and eligible dependents. It is often more affordable than individual policies due to several factors. Firstly, group insurance leverages economies of scale by spreading the risk across a larger pool of participants, resulting in lower premiums for each member. This risk pool comprises a diverse group of individuals with varying health profiles, ages, and job types, which helps to distribute the overall risk.

Secondly, employers often contribute a significant portion of the premium costs in group insurance plans, reducing the financial burden on employees. This employer contribution is considered a tax-deductible expense, providing further financial benefits. In contrast, individual policies are purchased directly by individuals, and they bear the full cost without the benefit of shared expenses.

Another advantage of group insurance is the absence of medical underwriting. This means that employees with pre-existing health conditions cannot be denied coverage or charged higher premiums solely based on their medical history. Group insurance plans also offer comprehensive benefits, often including dental, vision, and additional coverage options that may not be available with individual policies.

While group insurance has its advantages, it is important to consider potential drawbacks. One disadvantage is the limited customization of group plans, which may not align perfectly with the specific healthcare needs of every individual. Additionally, employees have less control over the selection of the insurance provider and plan design, as these decisions are typically made by the employer.

In summary, group insurance is generally more affordable than individual policies due to shared risks, employer contributions, tax benefits, and the absence of medical underwriting. However, it is important to weigh these benefits against the potential limitations in terms of customization and control.

Depression and Life Insurance: Does Diagnosis Impact Coverage?

You may want to see also

Frequently asked questions

If your employer provides group term life insurance as part of your benefits package, the first $50,000 of coverage is excluded from taxable income and won't be added to your W-2. However, if the coverage exceeds $50,000, the excess is considered taxable income and will be included in the taxable wages reported on your W-2 in Box 12 with code "C". This is often referred to as "phantom income".

Check Box 12 of your W-2 form for a specific dollar amount with code "C". This amount represents your employer's cost for providing you with group term life insurance coverage above $50,000, minus any amount you paid for the coverage. This amount is already included in your total "Wages, tips and other compensation" in Box 1 of the W-2, which is the figure reported on your tax return.

If you feel that the tax cost outweighs the benefits you're receiving, you can ask your employer if they have a "carve-out" plan or if they would be willing to create one. A "carve-out" plan allows selected employees to opt out of the group term coverage. Your employer could continue providing $50,000 of group term insurance (which is tax-free) and then offer you an individual policy for the remaining coverage. Alternatively, they could give you the excess amount as a cash bonus to purchase an individual policy.

![[OLD VERSION] TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71QcK4dsRbL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/512dhP2BIfL._AC_UL320_.jpg)