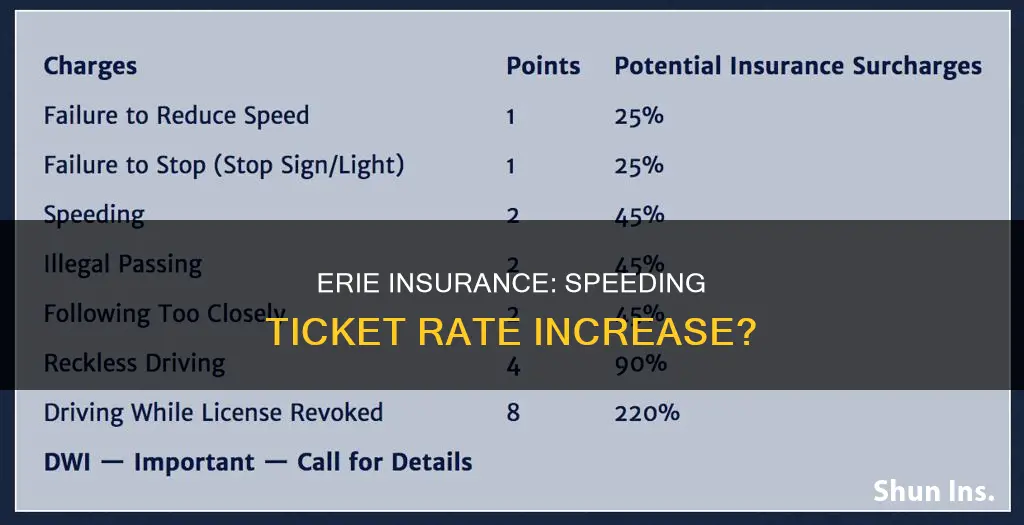

Speeding tickets can have a significant impact on auto insurance rates, with the average increase being around 25% and lasting for up to five years. However, the effect of a speeding ticket on insurance rates depends on various factors, including the driver's history, the insurer's policies, and the state's laws. Erie Insurance, a prominent insurance provider, offers competitive rates for drivers with speeding tickets, and their Rate Lock feature allows customers to avoid rate hikes even with a claim. While Erie's rates are generally affordable for drivers with violations, the extent of the increase caused by a speeding ticket is determined by the company's assessment of the driver's risk.

| Characteristics | Values |

|---|---|

| Average rate increase for drivers with speeding tickets | 26% or $507 more a year |

| Average rate increase for drivers with Erie insurance | 20% or $41 more per month |

| Effect of multiple speeding tickets on insurance rates | 67% to 111% more than drivers with no tickets |

| States with longer records of speeding tickets | Hawaii, Montana, Virginia |

| States with shorter records of speeding tickets | California, New Jersey, Texas |

| Erie Rate Lock feature | Stable insurance rates, no rate increase due to claims |

| Erie YourTurn driving safety app | Helps drivers improve safety by measuring speeding, hard braking and phone usage |

| Erie's claims process | Highly rated by customers and auto body specialists |

Explore related products

What You'll Learn

- The impact of a speeding ticket on your insurance premium depends on your driving history and the insurer

- A speeding ticket will remain on your driving record for up to 5 years, affecting your premium during this time

- A single speeding ticket can increase your insurance rates by 20%-26% on average

- Multiple speeding tickets will cause a significant increase in insurance rates

- You can avoid rate hikes with Erie Rate Lock, which lets you freeze your rate for a year

![]()

The impact of a speeding ticket on your insurance premium depends on your driving history and the insurer

The impact of a speeding ticket on your insurance premium depends on several factors, including your driving history, the insurer's policies, and the state you live in. Here are some key points to consider:

Firstly, insurance companies view past performance as an indicator of future behaviour. This means that recent speeding tickets, accidents, or violations will likely result in higher insurance rates compared to drivers with clean driving records. The number of speeding tickets matters too; multiple tickets will significantly increase your premium.

Secondly, insurance companies determine auto policy rates by assessing the driver's risk. The more violations or points on your record, the higher your premium will likely be. Some insurers may also cancel or decide not to renew your policy following serious violations, such as a suspended or revoked license.

Thirdly, the impact of a speeding ticket on your premium depends on the insurer's policies. Some insurers may offer forgiveness for minor traffic violations or first-time offences, resulting in no rate increase. Others may have specific programs or features, like Erie's Rate Lock®, that allow you to avoid rate increases unless you make certain changes to your policy, such as adding or removing a driver or vehicle.

Additionally, the state you live in plays a role. Speeding tickets and traffic violations can stay on your record for varying lengths of time, typically between three and five years, depending on state laws. Some states, like California, have shorter retention periods, while others, like Hawaii and Montana, may keep them on record for much longer.

Finally, your driving history and specific circumstances are crucial. A single speeding ticket can increase your insurance rate by an average of 23% to 26%, or approximately $41 per month. However, this can vary based on your previous driving record, the severity of the violation, and the insurer's specific calculations.

In summary, while a speeding ticket can impact your insurance premium, the extent of the impact depends on a combination of factors, including your driving history, the insurer's policies, and the state's regulations. It's always a good idea to contact your insurance company and explore options to mitigate any potential increase in your premium.

The Dangers of Faking Car Accidents for Insurance Claims

You may want to see also

Explore related products

![]()

A speeding ticket will remain on your driving record for up to 5 years, affecting your premium during this time

A speeding ticket will typically remain on your driving record for up to five years, although this can vary depending on the state. For example, in California, it stays on your record for 39 months, whereas in Virginia, it remains for five years. In Hawaii, speeding tickets will stick with you for 10 years, and in Montana, they will be on your record forever.

During the time that a speeding ticket is on your record, it is likely to affect your insurance premium. Insurance companies determine auto policy rates by assessing how risky a driver is to insure. The more violations or points you have on your record, the more you can expect to pay in premiums. A speeding ticket is usually considered a "surchargeable" incident, meaning it can raise your rates.

The impact of a speeding ticket on your premium can vary depending on several factors, including your prior driving record, how fast you were going, and your insurance company's policies. On average, a speeding ticket increases rates by around 20-26% or $41 per month. However, multiple tickets can lead to much higher increases, with drivers with three tickets paying twice as much as those with a clean record.

Some insurance companies may be willing to "forgive" minor traffic violations. For example, Erie Insurance offers a "Rate Lock" feature, which allows you to avoid rate increases due to claims or violations unless you make certain changes to your policy, such as adding or removing a driver or vehicle. Additionally, Erie offers competitive rates for drivers with speeding tickets, coming in as the third-cheapest option in one evaluation.

It's important to note that insurance companies have different look-back periods, so be sure to check with your insurer to understand how long a speeding ticket will affect your premium. Your rates will typically go back down after a few years of safe driving.

Teen Driver Insurance: Why It's More Expensive

You may want to see also

Explore related products

![Speeding to Get A Man in Uniform Sticker Speed Driver Bad Driver Funny Sarcastic Humorous Bumper Sticker Adults Joke Prank Uniform Man in Girl Meme Quotes [11.5"x3"]](https://m.media-amazon.com/images/I/51HQK7gH4FL._AC_UY218_.jpg)

![]()

A single speeding ticket can increase your insurance rates by 20%-26% on average

Speeding tickets and other types of moving violations are usually considered a "surchargeable" incident, which means that insurance companies can raise your rates. The average increase in insurance rates for drivers who get a speeding ticket is 26%, or nearly $507 more a year. This can vary depending on the state you live in, with Pennsylvania drivers paying 15% more for insurance after a speeding ticket, and North Carolina drivers paying 50% more for the same offence. The increase in insurance rates can also depend on other factors, such as your prior driving record, including other traffic violations and at-fault car accidents.

The impact of a speeding ticket on your insurance rates can also depend on the severity of the violation. For example, speeding between 6-10 mph over the speed limit will raise your insurance rates by an average of $40 a month, while speeding 21-25 mph over the limit will increase your rates by an average of $54 a month. Additionally, some insurance companies may assign lower penalties or none at all, even for major violations. For example, some companies offer a "Responsible Driver Plan" that forgives minor traffic violations every 36 months, while others may not raise rates after a single speeding violation.

It's important to note that traffic violations can stay on your record for three to five years, depending on your state. During this time, you may not be eligible for "good driver" discounts, which can further increase your insurance costs. Insurance companies typically determine auto policy rates by assessing how risky a driver is to insure, so it's important to maintain a clean driving record to avoid higher insurance rates.

U-Turn: Understanding USAA's Auto Insurance Gap Coverage

You may want to see also

Explore related products

![]()

Multiple speeding tickets will cause a significant increase in insurance rates

Insurance companies determine auto policy rates by assessing how risky a driver is to insure. The more violations or points on your driving record, the higher your insurance premiums are likely to be. Speeding tickets and other types of moving violations are usually considered "surchargeable" incidents, meaning they can raise your rates.

The length of time that a speeding ticket will affect your insurance rates depends on various factors, including your state, driving history, and insurance company. Speeding tickets can stay on your driving record for three to five years, although some states may require them to remain on your record for longer periods. For instance, a speeding ticket in Hawaii will be on your record for ten years, while in Montana, it will stay on your record indefinitely.

The impact of multiple speeding tickets on your insurance rates can be significant. For example, drivers with two speeding tickets may pay 67% more for full coverage, while those with three tickets may pay twice as much as drivers with a clean record. The increase in insurance rates due to multiple speeding tickets can be substantially higher than the average rate increase for a single speeding ticket, which is around 26%.

Additionally, multiple speeding tickets may result in the loss of safe driving discounts offered by insurance companies. This loss of a discount can further contribute to higher monthly payments, even if the base insurance rate does not increase significantly.

Health Insurance Repayment: Unraveling the Auto Accident Conundrum

You may want to see also

![]()

You can avoid rate hikes with Erie Rate Lock, which lets you freeze your rate for a year

While a speeding ticket can increase your insurance rates, Erie Insurance offers a feature called Erie Rate Lock that lets you avoid rate hikes by freezing your rate for a year. This means that even if you have a claim, your rates won't change unless you make certain changes to your policy, such as adding or removing a vehicle or a driver, or changing your primary residence. With Erie Rate Lock, you pay the same premium year after year, providing stable insurance rates and helping you manage your household budget.

It is important to note that insurance companies determine auto policy rates by assessing the risk associated with a driver's history. Speeding tickets and other traffic violations are considered "surchargeable" incidents, which can lead to higher rates. The impact of a speeding ticket on your insurance rates depends on factors such as your driving record, the severity of the violation, and the company insuring your car. On average, a speeding ticket can increase your insurance rates by 23% to 26%, or about $41 per month.

However, with Erie Rate Lock, you can lock in your rate and avoid these rate increases for a year. This feature is especially beneficial if you have a clean driving record, as it allows you to maintain your current rate even if you receive a speeding ticket. By freezing your rate, you can have peace of mind knowing that your insurance costs will remain stable, despite any violations or claims.

Additionally, Erie Insurance offers competitive rates for drivers with speeding tickets, and their rates are one of the lowest for multiple driver profiles, including good drivers, teens, young adults, seniors, and those with accidents on their record. Their excellent claims process has received high satisfaction ratings from customers, making them a reliable choice for insurance services.

Remember, Erie Rate Lock is not available in all states, and there may be limitations on the duration of the rate lock. Be sure to contact a local Erie agent to learn more about the specifics of this feature and how it can benefit you in maintaining stable insurance rates.

Auto Insurance: No-Fault Cover Explained in Simple Terms

You may want to see also

Frequently asked questions

A speeding ticket will almost always raise your insurance rates. The exact amount varies based on your driving history, where you live, and your insurance company's rules. On average, a single speeding ticket will raise your insurance rates by 23% to 26% or $41 per month. However, multiple tickets will cause rates to increase much more.

A speeding ticket will stay on your driving record for around three to five years, depending on your state. Your insurance company will likely consider the last 3-5 years of your driving record when calculating your premium.

You can reduce your insurance rates by shopping around for a cheaper insurance company, taking a driver education or defensive driving course, or comparing quotes from multiple companies. Erie Insurance also offers the ERIE Rate Lock® feature, which lets you avoid rate increases unless you make certain changes to your policy.