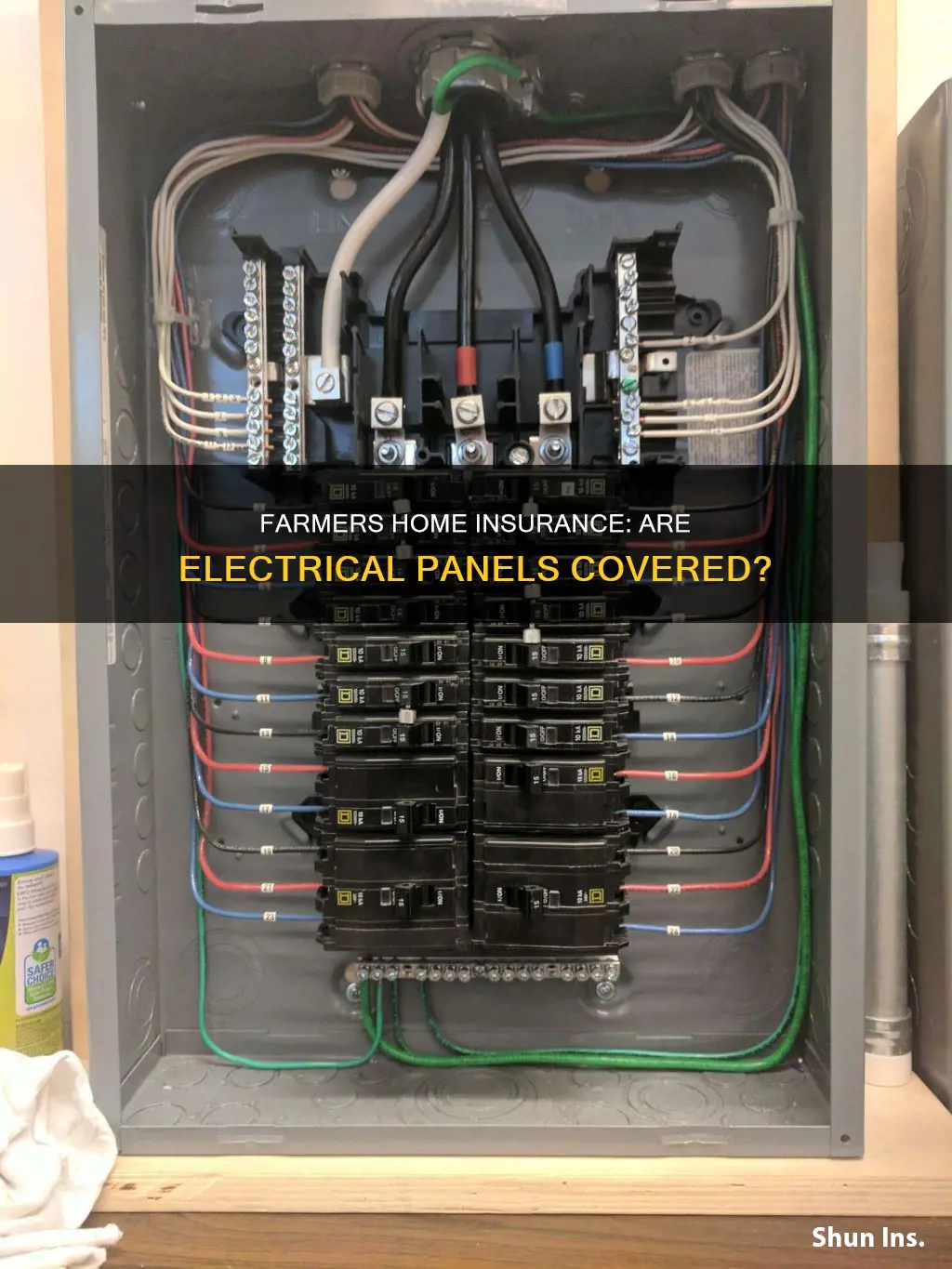

Farmers Insurance Group offers a wide range of coverage options for homeowners, including protection for their personal belongings, liability claims, and additional living expenses if their home becomes uninhabitable. While the company provides coverage for various electrical issues, it is unclear whether electrical panels are specifically included. Home insurance policies vary, with some covering electrical panels only if certain requirements are met, while others may require additional endorsements or riders for such coverage. Therefore, it is essential to carefully review your policy or contact Farmers Insurance directly to understand whether electrical panels are covered and under what circumstances.

| Characteristics | Values |

|---|---|

| Types of Home Insurance | HO-1, HO-2, HO-3, HO-4, HO-5, HO-6, HO-7, HO-8 |

| Homeowner's Insurance Coverage | Electrical issues, appliance breakdowns, power surges, socket malfunctions, broken outlets, light wattage issues, dwelling, personal property, liability, personal liability umbrella insurance, flood insurance, earthquake insurance |

| Farmer's Home Insurance Coverage | Dwelling, personal property, liability, extended replacement cost, additional living expenses, identity theft protection, solar panels |

| Farmer's Home Insurance Exclusions | Flooding, earthquake |

| Factors Affecting Insurance Coverage | Age and kind of wiring, circuit breaker, electrical panel age, electrical code compliance, location, home inspection, building codes |

Explore related products

What You'll Learn

![]()

Homeowner's insurance covers electrical issues

Homeowners insurance generally covers electrical issues, including appliance breakdowns, power surges, and socket malfunctions. However, it's important to note that the coverage depends on the age and type of wiring in your home. Homes with knob-and-tube or aluminum wiring may be denied coverage or require a special rider or endorsement. It is recommended to update your electrical wiring to conform to modern safety regulations.

Electrical panel upgrades are typically covered by homeowner's insurance, but certain requirements must be met. It's important to consult with electricians and insurance providers to understand what types of electrical panels are covered. Some insurance companies may require electrical panels to be replaced after a certain period, such as 40 years, or if there are signs of malfunction, power surges, or electrical fires.

Farmers Homeowners Insurance offers a range of coverage options, including dwelling, personal property, and liability. They also provide additional living expenses if your home becomes uninhabitable due to a covered event. Farmers Insurance specifically covers damage to solar panels caused by perils listed in the policy, such as fire, windstorms, hail, vandalism, and theft. They also offer an optional endorsement for additional coverage for solar photovoltaic electric panels, which includes mechanical breakdown and power surge damage coverage.

When choosing a homeowner's insurance policy, it's important to consider your property type, coverage needs, and budget. There are eight types of home insurance policies, offering different reimbursement rates and coverage levels. HO-3 insurance is the most common type, providing open peril coverage with comprehensive protection against a wide range of risks, except those specifically excluded.

It's always recommended to carefully review your insurance policy and consult with professionals to understand the specific coverage and exclusions related to electrical issues and panels.

Upfront Mortgage Insurance: QM Charges Explained

You may want to see also

Explore related products

![]()

Knob-and-tube and aluminium wiring are exceptions

Homeowner's insurance typically covers electrical issues within the home, including appliance breakdowns, power surges, and socket malfunctions. However, knob-and-tube and aluminium wiring are notable exceptions to this coverage. Homes constructed prior to the 1960s often feature antiquated electrical wiring, which is more susceptible to malfunction and poses a significant safety hazard.

Homeowner's insurance policies generally deny claims related to knob-and-tube and aluminium wiring, or they may require the purchase of a separate rider or endorsement for additional coverage. This distinction is crucial because outdated wiring can lead to severe electrical malfunctions and even house fires. Therefore, it is advisable to update your electrical wiring to meet modern safety regulations and mitigate potential risks.

The type of wiring in your property plays a pivotal role in determining coverage. While knob-and-tube and aluminium wiring are exceptions, other forms of wiring may fall under the purview of your insurance policy. It is essential to consult with a professional electrician to assess the wiring in your home and ensure it complies with current safety standards.

To enhance the safety of your home, consider upgrading to contemporary wiring systems that incorporate GFCI circuit interpreters and three-prong outlets. These modern features help regulate the flow of electricity, reducing the risk of electrical malfunctions and fires. By investing in these upgrades, you can not only improve the safety of your home but also ensure that your electrical system meets the requirements for insurance coverage.

While knob-and-tube and aluminium wiring are exceptions to standard coverage, homeowners can take proactive measures to address these wiring issues. Consult with electricians and insurance professionals to explore options for separate riders or endorsements. By taking these proactive steps, you can enhance the safety of your home and ensure more comprehensive protection in the event of electrical issues.

Mortgage Insurance: Zero Monthly Payment Options

You may want to see also

Explore related products

![]()

Consult an electrician to replace wiring

If you are experiencing electrical issues, it is important to consult a licensed electrician to assess the extent of the damage and recommend appropriate measures for repair or replacement. Electricians can safely repair or replace damaged wires, ensuring that your home's electrical system complies with current safety standards. Regular inspections by qualified professionals are also recommended to prevent wire damage and ensure the longevity and safety of your electrical infrastructure.

One of the signs that you need to consult an electrician for wiring repair or replacement is when power sockets, outlets, or switch plates become unusually warm to the touch. This condition indicates that an excessive amount of current is flowing through the wiring, which can be due to an overload or a short circuit within the electrical system. Such situations pose serious fire risks if left unattended. Upon noticing a warm power socket, it is important to immediately unplug any devices connected to these outlets and consult an electrician.

Another indication that your wiring system needs attention is the presence of frayed wires. Frayed wires can result from age, rodents, or improper installation, posing a significant risk of short circuits and electrical fires. If you notice any wire that appears damaged or worn out, it is critical to address this issue immediately by turning off the power supply to the affected area and consulting a professional electrician.

Consulting an electrician is also important when dealing with unusual odors associated with your electrical system. Burning odors, particularly near outlets or appliances, could indicate overheating wires or other serious issues. Additionally, a persistent ozone or fishy smell can also signal a problem. In such cases, it is crucial to seek immediate attention from a qualified electrician to identify and rectify the issue.

If you have outdated wiring, such as knob-and-tube or aluminum wiring, it is recommended to consult an electrician to discuss replacement options. Outdated wiring may not be covered by your homeowner's insurance, and upgrading to modern wiring will ensure compliance with safety regulations.

Home Insurance: AC Leaks Covered?

You may want to see also

Explore related products

![]()

Homeowner's insurance covers personal belongings

Homeowners insurance covers personal belongings, including furniture, electronics, clothing, appliances, books, music, cell phones, tablets, laptops, dishes, kitchen gadgets, and sporting equipment. Personal property coverage, as it is often called, protects your belongings against fire, theft, and other covered perils outlined in your policy. This coverage includes items stored off-premises, meaning you are covered anywhere in the world.

There are two types of loss settlements for your personal property: replacement cost and actual cash value. Replacement cost covers the item as new at the time of the claim, while actual cash value considers the replacement cost minus depreciation. Most standard policies include coverage for the structure of your home, your personal belongings, liability protection, and additional living expenses.

The type of homeowners insurance determines your covered perils and reimbursement values. Named peril policies cover only those explicitly listed, while open peril policies cover all perils except for listed exclusions. The reimbursement method determines how much you can claim. Actual Cash Value (ACV) is based on the current value, while Replacement Cost Value (RCV) is based on the replacement cost without depreciation.

It is important to note that certain items may not be covered under personal property insurance. For example, a home insurance policy usually won't cover cars or pets. Additionally, if you're a homeowner who rents out space to a tenant, the tenant's belongings won't be covered under your policy.

To ensure adequate coverage for valuable items, you can schedule an item or add an insurance rider to your policy. This allows you to insure items such as jewellery, fine art, or heirlooms. Scheduling items may increase your premium, but it provides peace of mind that these possessions are adequately protected.

In terms of electrical panels, it appears that there is no definitive answer. Homeowners insurance policies vary, and while some may require electrical panel replacement after a certain period (e.g., 40 years), others do not seem to have this requirement. It is always best to refer to your specific policy or consult your insurance provider for clarification.

Home Insurance: Stabilizing Your Sanctuary

You may want to see also

Explore related products

![]()

Flood insurance is not included in standard insurance

Farmers Insurance offers a range of options and features to help tailor your homeowner's insurance policy to your needs. While standard coverage includes dwelling, personal property, and liability, there are several other risks that you may need to purchase separate policies for.

One such risk is flooding. Flood insurance is not included in standard insurance policies and must be purchased separately. Depending on your home's location and the risk of flooding, you may want to consider buying a flood insurance policy. If you have a mortgage in an area with an increased risk of flooding, your mortgage company may even require you to do so.

Another risk that is not covered by standard insurance is earthquakes. Earthquakes can cause widespread damage, but they are not covered by standard homeowners insurance. However, in some cases, earthquake coverage can be added as an optional extra to your homeowners policy.

If you are concerned about having sufficient liability coverage, you may also want to consider purchasing Personal Liability Umbrella Insurance. This provides additional liability coverage beyond the limits of your auto and other personal liability policies. This extra protection can be purchased in $1 million increments up to $10 million, giving you peace of mind.

In addition, if you have solar panels, you should review your policy carefully to understand the specific coverage and any exclusions related to them. Farmers Insurance offers an optional endorsement called "Additional Coverage for Solar Photovoltaic Electric Panels," which provides comprehensive coverage for solar panels, including mechanical breakdown, power surge damage, and the cost of removal and reinstallation during repairs.

Lastly, it is important to note that the type of circuit breaker you have installed in your home may impact whether your homeowner's insurance covers electrical panel upgrades. Be sure to consult with your insurance company and professional electrical contractors to determine if your electrical panel upgrades will be covered.

Other Structures Coverage: Protecting Your Property's Additional Buildings

You may want to see also

Frequently asked questions

Farmers homeowners insurance covers electrical issues within the home, including electrical panels. However, it is important to review your policy to understand the specific coverage and any exclusions.

Farmers homeowners insurance typically covers dwelling, personal property, and liability. It also covers repairing damaged parts of your home and may include additional living expenses if your home becomes uninhabitable.

Yes, Farmers homeowners insurance typically covers damage to solar panels caused by perils listed in the policy, such as fire, windstorms, hail, vandalism, and theft. They also offer an optional endorsement called "Additional Coverage for Solar Photovoltaic Electric Panels," which provides additional coverage for solar panels.

Flooding and earthquakes are generally excluded from standard homeowners insurance policies, including Farmers. However, you may be able to purchase separate policies or add optional coverage for these perils.

It's important to review your policy and contact Farmers directly to understand if your electrical panel is covered. The age of your home, the type of wiring and circuit breaker, and whether your electrical panel is up to code will all be factors in determining coverage.