It is important to understand the difference between at-fault and not-at-fault accidents when it comes to insurance rates. While Geico offers accident forgiveness in 47 states and the District of Columbia, it is applicable only to the first accident. Geico considers your claim history to dictate the risk of insuring you, and your rates will likely go up after an accident, regardless of who is at fault. However, an at-fault accident will generally have a greater impact on your insurance premium, and a not-at-fault accident is less likely to increase your insurance rates. Multiple not-at-fault claims can increase your rate depending on the timeframe and number of claims.

| Characteristics | Values |

|---|---|

| Increase in insurance rates | Insurance rates may increase even if the accident is not your fault. |

| Accident forgiveness | Geico offers accident forgiveness in 47 states and the District of Columbia, excluding California, Connecticut, and Massachusetts. Accident Forgiveness applies only to the first accident. |

| Rate hike | A not-at-fault accident is less likely to increase insurance rates but does not guarantee immunity from rate changes. |

| Claim history | Geico considers claim history to dictate the risk of insuring a customer. |

| Number of accidents | The number of accidents will cause insurance rates to go up. |

| Comprehensive claims | Comprehensive claims will not increase insurance rates. |

| State laws | State laws and insurance company policies play a role in determining premium increases. |

| Driving history | A clean driving record may result in a less severe rate hike. |

| Policy renewal | Insurance rates may increase at the time of policy renewal. |

Explore related products

What You'll Learn

![]()

Geico's accident forgiveness policy

Eligibility for accident forgiveness is determined by the specific policy type and state laws and regulations. For example, drivers under 21 years of age may not be eligible for accident forgiveness. Additionally, it may be necessary to meet certain driving record and driving experience requirements to qualify.

Accident forgiveness can be earned or purchased in states where it is available. It can be added to a policy or awarded to those with a good driving record. Having accident forgiveness on your GEICO auto insurance policy can provide peace of mind and financial stability after an unexpected incident, as it protects you from rate increases.

It is worth noting that while GEICO offers accident forgiveness, there are reports from customers claiming that GEICO did not honour their accident forgiveness policy. These customers experienced increased premiums or surcharges after their first accident, despite the accident forgiveness policy stating that rates should not be impacted by the first accident.

Additionally, it is important to understand that even if GEICO's accident forgiveness policy is applied, it may only apply to GEICO-insured drivers. If you are involved in an accident with another driver who is not insured by GEICO, their rates may still increase, and you may still experience repercussions.

Understanding Medication Insurance Claims and Reversals

You may want to see also

Explore related products

![]()

Rate changes after not-at-fault accidents

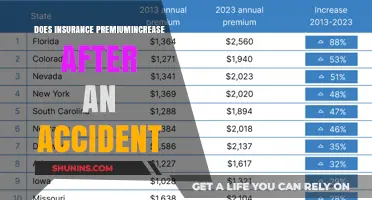

It's important to note that each insurer calculates these potential premium changes differently. The number of accidents, the time frame between claims, and the cost of the claim can all influence rate changes. For example, GEICO insurance rates may increase by about 79% after your first accident resulting in a claim of $750 or more. If this is your second accident in less than three years, your insurance will likely increase even more.

Additionally, state laws and insurance regulations play a significant role in determining premium increases. Certain states, such as California, Connecticut, and Massachusetts, do not offer accident forgiveness, which can further impact rate changes after not-at-fault accidents.

It's worth reviewing your policy and discussing potential impacts with your insurance provider to understand how rate changes are handled in your specific situation. While a single not-at-fault accident may not always increase your rates, multiple claims or a pattern of accidents can be considered a higher risk, resulting in higher premiums.

To avoid unexpected rate increases, it is essential to provide accurate and complete information when obtaining insurance quotes. Being transparent about your driving history and any accidents, even minor ones, can help ensure that you receive an accurate quote and reduce the likelihood of premium increases in the future.

Anxiety and Travel Insurance: What's Covered Medically?

You may want to see also

Explore related products

![]()

Claim history and risk assessment

When setting insurance premiums, GEICO considers the overall group of insured drivers. This means that the risk is shared between the insurance company and a large group of policyholders. The cost of repairs, injuries, and damages is then shared among those policyholders.

GEICO considers claim history when assessing risk and setting insurance premiums. While at-fault accidents are likely to increase insurance premiums as they are often an indicator of increased future risk, not-at-fault accidents may also result in higher premiums. This is because multiple claims, even if they are not the policyholder's fault, indicate higher risk.

The number of claims and the timeframe between them are both considered when assessing risk. For example, GEICO offers accident forgiveness for the first at-fault accident in 47 states and the District of Columbia, with the exceptions of California, Connecticut, and Massachusetts. However, subsequent at-fault accidents do not qualify for accident forgiveness. Additionally, if a policyholder has filed another claim of any kind in the last three years, even a comprehensive claim such as hitting a deer or having a shattered windshield, it may result in higher rates.

It is important to note that GEICO is not the only factor influencing insurance premiums. State laws, insurance company policies, the car make and model, driving frequency, and storage location can all impact premiums.

Understanding Braces Coverage in Medical Insurance Plans

You may want to see also

Explore related products

![]()

State laws and insurance regulations

The impact of not-at-fault accidents on insurance rates also varies by state. Some states may have specific regulations that influence how insurance companies assess and calculate premiums after such accidents. For example, while a not-at-fault accident is generally less likely to increase insurance rates, certain states may have provisions that allow for rate changes under specific circumstances, such as significant damage or injuries.

Additionally, state laws can influence the timeframe for filing a claim after an accident. While it is generally recommended to report accidents as soon as possible, the actual deadline may differ based on individual state regulations. These regulations can also impact how long car insurance rates remain affected by a prior accident, with rates typically impacted for three to five years on average.

Furthermore, state laws and regulations can influence the factors considered when setting insurance premiums. For instance, factors such as the car's make and model, commute distance, driving history, and claims history may be considered in determining rates. However, the weight given to each factor can vary by state, resulting in differences in premium calculations across different states.

It is important to note that insurance companies, including GEICO, consider various factors when determining premium increases, and state laws and regulations are just one aspect of this complex process. Other factors, such as claim history, driving record, and the specific circumstances of the accident, also play a significant role in determining any changes to insurance rates.

Child's Medical Privacy: Using Parent's Insurance

You may want to see also

Explore related products

![]()

Comprehensive claims and rate increases

Comprehensive coverage is a type of auto insurance that pays for car repairs that don't result from a collision with another vehicle. For example, if your car is damaged by hail, you could make a comprehensive claim.

Comprehensive claims will generally increase your auto insurance costs. A survey by The Zebra found that a comprehensive claim increases auto insurance premiums for a standard six-month policy by an average of $36. WalletHub reports that filing a claim will cause your auto insurance premiums to rise by an average of 3% to 32% for three to five years. The Zebra survey also found that the most affordable insurance companies for drivers who have previously filed a comprehensive claim are USAA, GEICO, and State Farm.

According to Progressive, car insurance companies may raise your rates after a claim because they see the driver as a higher risk, which increases the likelihood of future claims. Progressive also notes that accident forgiveness programs can help prevent rate increases after certain types of accidents, such as your first accident or smaller accidents. Similarly, GEICO offers Accident Forgiveness for your first otherwise surchargeable, at-fault accident.

While insurance companies assess accidents differently based on fault, an accident where you are not at fault is less likely to increase your insurance rates. However, it does not guarantee immunity from rate changes. Additionally, some states have specific regulations regarding rate changes after not-at-fault accidents, so it is important to review your policy and discuss potential impacts with your insurance provider.

Medical and Life Insurance: What's the Difference?

You may want to see also

Frequently asked questions

While a not-at-fault accident is less likely to increase your insurance rates, it doesn't guarantee immunity from rate changes. Geico looks at your claim history to dictate the risk of insuring you, and multiple not-at-fault claims can increase your rate depending on the timeframe between claims and the number of them.

If your claim is reimbursed by the other driver or their insurance company, the cost of your insurance will not go up.

Insurance rates typically increase anywhere from 0% to 50% or more after an at-fault accident, though this varies significantly based on factors like the severity of the accident, the claim amount, and your driving history. Geico insurance will go up by about 79% after your first accident resulting in a claim of $750 or more.

The increase typically lasts between 3 and 5 years, depending on the circumstances.