Health insurance is a critical component of financial planning, but its role in tax credits, particularly those related to education, is often misunderstood. Many taxpayers wonder whether their health insurance expenses can be leveraged to qualify for school tax credits, which are designed to offset educational costs. While health insurance itself typically does not directly count toward school tax credits, certain related expenses, such as those for dependent care or specific educational programs tied to health needs, might be eligible under specific circumstances. Understanding the intersection of health insurance and educational tax benefits requires careful examination of tax laws and the types of credits available, such as the Lifetime Learning Credit or the American Opportunity Tax Credit, to determine if any health-related expenses can be applied toward these incentives.

| Characteristics | Values |

|---|---|

| Eligibility for Tax Credit | Health insurance premiums generally do not qualify for school tax credits. |

| Type of Tax Credit | School tax credits typically apply to education-related expenses, not health insurance. |

| Federal vs. State | Federal tax credits (e.g., Lifetime Learning Credit) do not include health insurance. State-specific credits vary; some may allow health insurance if tied to education (e.g., student health plans). |

| Student Health Plans | Some states may allow student health plan premiums as part of education expenses for tax credits. |

| Dependent Care vs. Education | Health insurance is often categorized under dependent care, not education, unless specifically tied to educational programs. |

| Documentation Required | If health insurance is eligible, detailed documentation linking it to education expenses is typically required. |

| Annual Limits | Tax credits have annual caps; health insurance premiums rarely count toward these limits. |

| Examples of Eligible Expenses | Tuition, books, supplies, and certain fees, but not health insurance in most cases. |

| Recent Legislative Changes | As of 2023, no major federal changes include health insurance in school tax credits. State laws may vary. |

| Consultation Needed | Tax professionals or state revenue departments should be consulted for specific eligibility. |

Explore related products

What You'll Learn

- Eligibility criteria for health insurance in school tax credit programs

- Types of health insurance plans accepted for tax credits

- Documentation required to claim health insurance for school tax credits

- Impact of health insurance premiums on tax credit calculations

- State-specific rules for health insurance in school tax credits

![]()

Eligibility criteria for health insurance in school tax credit programs

Health insurance eligibility for school tax credit programs hinges on meeting specific criteria, often tied to income thresholds and plan adequacy. These programs, designed to offset educational expenses, typically require families to demonstrate financial need. For instance, the federal Lifetime Learning Credit mandates that your modified adjusted gross income (MAGI) falls below certain limits—$69,000 for single filers and $138,000 for joint filers as of 2023—to qualify for the full credit. Health insurance premiums may factor into your MAGI calculation, indirectly influencing eligibility by affecting your taxable income.

To qualify, your health insurance plan must meet minimum essential coverage (MEC) standards, as defined by the Affordable Care Act (ACA). This includes employer-sponsored plans, individual market plans, and government-sponsored programs like Medicaid. However, short-term health plans or health-sharing ministries often fail to meet MEC requirements, disqualifying them from consideration. For example, if you’re claiming the American Opportunity Tax Credit (AOTC), ensuring your health insurance complies with MEC is crucial, as it indirectly supports your eligibility by maintaining your overall financial standing.

Age and enrollment status also play a role. Dependents under 25 may remain on their parents’ health insurance plan, which can impact the family’s MAGI and, consequently, their eligibility for school tax credits. For instance, a college student covered under their parents’ ACA-compliant plan could help the family meet income thresholds for credits like the AOTC. Conversely, students with their own health insurance must ensure their plan meets MEC and report premiums accurately to optimize their tax credit eligibility.

Practical tips include reviewing your health insurance plan annually to confirm MEC compliance and calculating your MAGI with and without premium deductions to assess potential tax credit impacts. For families near the income threshold, consider contributing to a Health Savings Account (HSA) if eligible, as HSA contributions reduce taxable income and may improve your chances of qualifying for school tax credits. Always consult IRS guidelines or a tax professional to navigate these complexities effectively.

Using Insurance with Medicaid in Illinois: What's Possible?

You may want to see also

Explore related products

![]()

Types of health insurance plans accepted for tax credits

Health insurance plans that qualify for tax credits are primarily those purchased through the Health Insurance Marketplace, also known as the exchange. These plans must meet specific criteria to be eligible for the Premium Tax Credit (PTC), a subsidy designed to help lower-income individuals and families afford coverage. The types of plans accepted include Bronze, Silver, Gold, and Platinum categories, each differing in cost-sharing levels and monthly premiums. Silver plans are particularly noteworthy because they are the only ones that can be paired with Cost-Sharing Reduction (CSR) subsidies, which further reduce out-of-pocket expenses like deductibles and copayments.

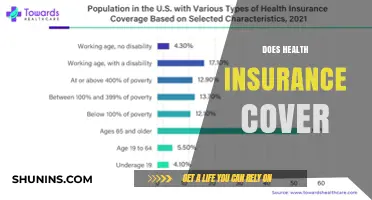

To qualify for these tax credits, your income must fall between 100% and 400% of the Federal Poverty Level (FPL). For example, in 2023, a single individual earning between $13,590 and $54,360 annually would be eligible. Families of four with incomes between $27,750 and $111,000 also qualify. It’s crucial to note that if you have access to affordable employer-sponsored insurance or government programs like Medicaid, you may not be eligible for Marketplace subsidies. Always verify your eligibility using the Marketplace’s application tool to avoid surprises.

Not all health insurance plans are created equal when it comes to tax credits. Plans purchased outside the Marketplace, such as short-term health insurance or health-sharing ministry plans, do not qualify. Similarly, catastrophic health plans, which are available to individuals under 30 or those with hardship exemptions, are ineligible for subsidies. If you’re considering a plan, ensure it’s labeled as a “Qualified Health Plan” (QHP) on the Marketplace to confirm its eligibility for tax credits.

Practical tip: When selecting a plan, consider your healthcare needs and budget. Silver plans, while slightly more expensive in premiums than Bronze, often provide better value due to CSR subsidies. For instance, a Silver plan with CSR might have a $500 deductible instead of $6,000, making it more cost-effective for frequent medical users. Use the Marketplace’s preview tool to estimate your total annual costs, including premiums and out-of-pocket expenses, before enrolling.

Finally, timing matters. Tax credits can be applied directly to your monthly premiums if you enroll during the Open Enrollment Period (typically November 1 to January 15) or during a Special Enrollment Period triggered by life events like marriage or job loss. If you choose to claim the credit when filing taxes, you’ll need to reconcile any advance payments received during the year. Keep detailed records of your income and premium payments to ensure accurate reporting and avoid penalties.

Understanding Medical Insurance Options After Turning 65

You may want to see also

Explore related products

![]()

Documentation required to claim health insurance for school tax credits

Health insurance can indeed be a qualifying expense for school tax credits, but claiming it requires meticulous documentation. The IRS and state tax agencies demand proof that your health insurance payments are directly tied to educational expenses, such as student health plans or premiums covering dependents enrolled in school. Without the right paperwork, your claim may be denied, leading to lost savings.

Essential Documents to Gather

Start by collecting your health insurance policy statements, which should detail monthly premiums and coverage periods. If your child’s school offers a health plan, obtain invoices or receipts showing payments made during the tax year. For dependents covered under your policy, ensure their enrollment status is verified through school records or transcripts. Additionally, if you’re self-employed and deduct health insurance premiums, include Form 1040 Schedule 1 to link these expenses to your tax credit claim.

Organizing Your Evidence

Create a dedicated folder for all health insurance-related documents, both physical and digital. Label each item clearly with dates and descriptions, such as “January 2023 Health Insurance Premium Receipt” or “Student Health Plan Invoice – Fall Semester.” If your insurer provides end-of-year summaries, include these to demonstrate consistent coverage. For dependents, pair insurance documents with school enrollment forms to establish eligibility.

Common Pitfalls to Avoid

One frequent mistake is claiming general health insurance premiums without proving their connection to education. For instance, if your child’s school requires health insurance as part of enrollment, include the school’s policy statement or a letter confirming this requirement. Avoid submitting incomplete forms or omitting dates, as these can trigger audits. If you’re unsure whether a document qualifies, consult IRS Publication 970 or a tax professional for clarity.

Finalizing Your Claim

Once your documentation is complete, review it against the tax credit criteria for your state and federal filings. Use Form 8863 for federal education credits and attach supporting documents as needed. Keep copies of everything submitted, as tax agencies may request further verification. By staying organized and thorough, you maximize your chances of successfully claiming health insurance as part of your school tax credits.

Get Cash Payouts from Supplemental Accident Insurance Policies

You may want to see also

Explore related products

![]()

Impact of health insurance premiums on tax credit calculations

Health insurance premiums can significantly influence tax credit calculations, particularly when considering education-related credits like the Lifetime Learning Credit or the American Opportunity Tax Credit. These credits are designed to offset the costs of higher education, but their eligibility and amounts are often tied to adjusted gross income (AGI). Premiums for health insurance, especially those paid with after-tax dollars, can reduce AGI, potentially increasing eligibility for these credits. For instance, if a family’s AGI is slightly above the threshold for a tax credit, deducting health insurance premiums might lower their income enough to qualify. This interplay highlights the importance of understanding how health insurance expenses are treated in tax calculations.

Consider a practical example: a single taxpayer earning $85,000 annually pays $3,000 in health insurance premiums. Without deducting these premiums, their AGI remains at $85,000, which may disqualify them from certain education tax credits due to income limits. However, if they can reduce their AGI to $82,000 by deducting the premiums (e.g., through self-employed health insurance deductions), they might fall within the eligibility range. This scenario underscores the need to strategically account for health insurance costs when planning for education-related tax benefits.

From a comparative perspective, the treatment of health insurance premiums differs depending on the type of tax credit and the taxpayer’s filing status. For example, the Premium Tax Credit, which subsidizes health insurance purchased through the Marketplace, operates independently of education credits but shares the common thread of income-based eligibility. In contrast, deductions for health insurance premiums (such as those available to self-employed individuals) directly reduce AGI, indirectly boosting eligibility for education credits. Understanding these distinctions is crucial for maximizing both health and education tax benefits.

To navigate this complexity, taxpayers should follow a structured approach. First, identify all health insurance premiums paid with after-tax dollars, as these are most likely to impact AGI. Second, consult IRS guidelines or a tax professional to determine which deductions or credits apply to your situation. Third, use tax software or worksheets to model different scenarios, such as the impact of deducting premiums on AGI and subsequent eligibility for education credits. Finally, keep detailed records of health insurance payments and education expenses to support your claims during tax filing.

A cautionary note: not all health insurance premiums qualify for deductions or credits that affect AGI. Premiums paid by employers on behalf of employees, for instance, are typically excluded from taxable income and thus do not reduce AGI. Additionally, overestimating deductions or misapplying credits can lead to audits or penalties. Taxpayers should exercise diligence and seek professional advice when in doubt. By carefully integrating health insurance costs into tax planning, individuals can optimize their eligibility for education tax credits and maximize their financial benefits.

Missed Open Enrollment? Here’s What to Do Next for Health Insurance

You may want to see also

Explore related products

![]()

State-specific rules for health insurance in school tax credits

Health insurance eligibility for school tax credits varies dramatically by state, with no federal mandate dictating uniformity. This patchwork of rules means families in Arizona might qualify for credits if their insurance covers specific school-related health services, while in New York, only plans meeting certain minimum essential coverage (MEC) standards apply. Understanding these nuances is crucial for maximizing potential tax benefits.

Research your state’s Department of Revenue website for specific guidelines, as they often outline qualifying insurance types (e.g., employer-sponsored, individual market, Medicaid) and required coverage areas like vision, dental, or mental health services directly tied to educational needs.

Consider Illinois, where the state’s Education Expense Credit allows a 25% credit for qualified education expenses, including health insurance premiums if the policyholder is a dependent student. However, this credit caps at $500 per dependent annually, and the insurance must be itemized on Schedule M of the IL-1040 form. In contrast, Texas offers no direct credit for health insurance premiums but allows deductions for contributions to Health Savings Accounts (HSAs) linked to high-deductible plans, indirectly benefiting families with school-aged children. These examples highlight the importance of scrutinizing both credit amounts and eligibility criteria.

States like California take a more inclusive approach, allowing health insurance premiums to count toward the state’s College Access Tax Credit if the student is enrolled in a qualifying institution and the insurance meets MEC requirements. Meanwhile, Florida’s Family Empowerment Scholarship Program requires proof of health insurance but does not offer a direct tax credit for premiums, instead prioritizing coverage as a condition for scholarship eligibility. Such variations underscore the need to align insurance choices with both state tax laws and educational funding programs.

To navigate these complexities, families should first identify their state’s specific tax credit programs related to education. Next, review the fine print on qualifying health insurance plans, focusing on coverage periods, provider networks, and excluded services. For instance, some states may disqualify plans with high out-of-pocket maximums or limited mental health coverage. Finally, consult a tax professional or utilize state-provided worksheets to ensure accurate reporting and maximize potential credits. Proactive planning and attention to detail can turn health insurance from a necessary expense into a strategic financial tool.

Intercoastal Medical Group: Insurance Coverage and You

You may want to see also

Frequently asked questions

No, health insurance itself does not qualify you for a school tax credit. School tax credits are typically tied to education-related expenses or donations to eligible educational organizations, not health insurance coverage.

No, health insurance premiums cannot be used as a deduction for school tax credits. These credits are generally based on qualified education expenses or contributions to specific educational programs, not healthcare costs.

No, there are no tax credits that directly combine health insurance and education expenses. Health insurance-related credits (like the Premium Tax Credit) and education-related credits (like the American Opportunity Credit) are separate and cannot be combined for a school tax credit.