Health insurance is primarily designed to cover medical expenses, treatments, and preventive care, but it typically does not include burial or funeral costs. These expenses are generally considered separate from healthcare and fall under the purview of life insurance, burial insurance, or pre-need funeral plans. While health insurance focuses on managing illnesses, injuries, and wellness, burial expenses are often addressed through specialized policies or personal savings. Individuals seeking coverage for end-of-life costs should explore options like life insurance or burial insurance, which are specifically tailored to provide financial assistance for funeral arrangements and related expenses.

| Characteristics | Values |

|---|---|

| Does Health Insurance Cover Burial? | No, health insurance typically does not cover burial or funeral costs. |

| Purpose of Health Insurance | Covers medical expenses, hospitalization, treatments, and preventive care. |

| Burial/Funeral Costs Coverage | Usually covered by separate policies like life insurance, burial insurance, or pre-need funeral plans. |

| Exceptions | Some life insurance policies may include a burial benefit rider. |

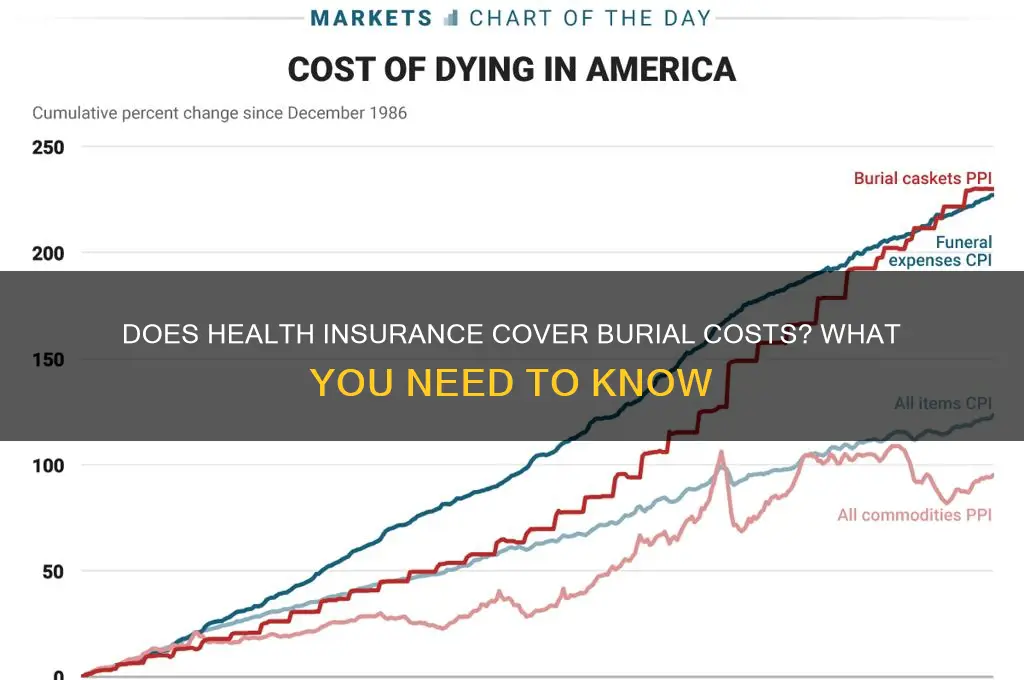

| Average Funeral Costs (2023) | $7,000–$12,000 (varies by location and services). |

| Alternative Options | Final expense insurance, savings accounts, or crowdfunding. |

| Medicare/Medicaid Coverage | Does not cover funeral expenses; only covers specific medical services. |

| State-Specific Programs | Some states offer limited assistance for indigent burials. |

| Importance of Planning | Recommended to plan separately for burial costs to avoid financial burden on family. |

Explore related products

$2.99 $9.97

What You'll Learn

![]()

Types of Policies Covering Burial Costs

Health insurance typically does not cover burial costs, as its primary focus is on medical expenses. However, several specialized policies and financial products are designed to address end-of-life expenses, including burial or cremation. Understanding these options can help individuals and families plan effectively without relying on health insurance.

Burial Insurance (Final Expense Insurance):

This is a whole life insurance policy with a small death benefit, usually between $5,000 and $25,000, specifically intended to cover funeral and burial costs. Premiums are often affordable, and the application process is simplified, sometimes requiring no medical exam. For example, a 60-year-old might pay $50–$100 monthly for a $10,000 policy. The key advantage is that the payout is guaranteed, ensuring funds are available when needed. However, premiums can increase with age, and the coverage amount may not keep pace with rising funeral costs.

Pre-Need Funeral Insurance:

This policy is purchased directly from a funeral home and locks in the cost of specific services at current prices. For instance, if a traditional burial costs $8,000 today, the policy ensures that price won’t increase, even if funeral costs rise in the future. While this provides certainty, it lacks flexibility—the funds can only be used at the designated funeral home. It’s ideal for those who have already chosen their arrangements and want to avoid inflationary risks.

Life Insurance Policies:

Traditional term or whole life insurance policies can also cover burial costs, as beneficiaries receive a lump sum upon the policyholder’s death. A 20-year term life policy with a $50,000 benefit, for example, might cost a 40-year-old nonsmoker around $20–$30 monthly. The advantage is higher coverage amounts, which can address burial costs alongside other debts or family needs. However, these policies often require medical underwriting and may be more expensive than burial-specific insurance.

Annuities with Death Benefits:

Some annuities include a death benefit rider, ensuring a minimum payout to beneficiaries if the annuitant dies before receiving the full value. While not specifically for burial, this can provide funds for end-of-life expenses. For instance, a fixed annuity with a $25,000 death benefit could supplement other savings. The drawback is that annuities are primarily retirement income tools, and their complexity may not suit everyone’s needs.

Practical Tips:

Compare policies based on premiums, coverage limits, and payout terms. Consider inflation—funeral costs rise about 3% annually, so ensure your chosen policy keeps pace. Review beneficiary designations regularly, especially after life changes like marriage or divorce. Finally, discuss your plans with family to avoid confusion and ensure your wishes are known.

By exploring these options, individuals can secure burial cost coverage independently of health insurance, providing peace of mind for themselves and their loved ones.

Mastering Sunrise Lab: A Guide to Filling Health Insurance Details

You may want to see also

Explore related products

![]()

Life Insurance vs. Health Insurance Differences

Health insurance and life insurance serve fundamentally different purposes, yet confusion often arises when considering end-of-life expenses like burial costs. Health insurance is designed to cover medical expenses incurred during your lifetime, such as hospital stays, surgeries, and prescription medications. It does not, however, cover burial or funeral expenses, which are typically excluded from its scope. Life insurance, on the other hand, provides a financial payout to beneficiaries upon the insured’s death, which can be used to cover burial costs, outstanding debts, or other financial needs. Understanding this distinction is critical for planning both your healthcare and your legacy.

Consider a scenario where a 45-year-old individual with a family history of heart disease purchases a comprehensive health insurance plan. While this plan will cover cardiac treatments, emergency procedures, and preventive care, it will not provide funds for funeral arrangements if the individual passes away. To address this gap, they might opt for a term life insurance policy with a $250,000 death benefit, ensuring their family has the financial means to handle burial expenses, typically ranging from $7,000 to $12,000, without added stress. This example highlights the complementary roles of health and life insurance in a holistic financial strategy.

From a persuasive standpoint, relying solely on health insurance for end-of-life planning is a risky oversight. Health insurance premiums, deductibles, and copays are structured to manage medical costs, not to provide a lump-sum payout for non-medical expenses. Life insurance, particularly whole life or term policies, offers predictable coverage tailored to your family’s needs. For instance, a 30-year-old non-smoker might secure a 20-year term policy for as little as $20–$30 per month, providing peace of mind at a fraction of the cost of potential out-of-pocket burial expenses.

Comparatively, the two insurances differ in their triggers and beneficiaries. Health insurance activates during your lifetime, benefiting you directly by reducing medical costs. Life insurance, however, benefits your loved ones after your death, offering financial stability during a vulnerable time. For example, a $10,000 life insurance policy could cover a modest funeral, cremation, and even leave a small inheritance, whereas health insurance would only offset medical bills incurred before death. This comparison underscores the importance of pairing both types of coverage for comprehensive protection.

Finally, a descriptive approach reveals the emotional and practical implications of these differences. Imagine a family grieving the loss of a loved one, only to face the burden of unexpected funeral costs. Without life insurance, they might resort to crowdfunding or debt to cover expenses, adding financial strain to emotional grief. In contrast, a well-structured life insurance policy ensures the family can focus on honoring their loved one’s memory without financial worry. Health insurance, while essential for managing illness and injury, simply does not fill this role. By recognizing these distinctions, individuals can make informed decisions to safeguard both their health and their family’s future.

Oregon's Free Health Insurance: A Step-by-Step Application Guide

You may want to see also

Explore related products

![]()

Out-of-Pocket Funeral Expenses Explained

Health insurance policies typically exclude funeral expenses, leaving families to navigate these costs independently. This gap in coverage means that out-of-pocket funeral expenses can quickly become a financial burden, often at an emotionally challenging time. Understanding these costs is the first step in preparing for them. Funeral expenses can range from $7,000 to $12,000 on average, depending on the type of service, location, and personal preferences. Cremation, for instance, is generally less expensive, averaging around $6,000, while traditional burials can exceed $10,000 when factoring in caskets, burial plots, and memorial services.

To manage these expenses, consider pre-planning as a proactive strategy. Pre-planning allows individuals to lock in current prices, avoiding future inflation, and provides peace of mind for loved ones. Many funeral homes offer pre-arrangement packages, which can be paid in installments. Additionally, final expense insurance, also known as burial insurance, is a specialized policy designed to cover funeral costs. These policies typically range from $5,000 to $25,000 and require no medical exam, making them accessible for older adults or those with health issues.

Another practical approach is to explore cost-saving options without compromising dignity. Opting for a direct cremation, which excludes a formal service, can significantly reduce expenses. Similarly, choosing a simple urn or casket, using an existing family plot, or holding a memorial service at home can lower costs. Crowdfunding platforms like GoFundMe have also become a viable option for families seeking financial assistance from their community.

Despite these strategies, it’s crucial to be aware of hidden costs that can inflate out-of-pocket expenses. For example, embalming, which is often optional, can add $700 to $1,000 to the total bill. Transportation fees, death certificates, and obituary notices are additional expenses that are frequently overlooked. Creating a detailed budget and asking funeral providers for an itemized price list can help avoid unexpected charges.

In conclusion, while health insurance does not cover burial expenses, understanding and planning for out-of-pocket funeral costs can alleviate financial stress. By pre-planning, exploring cost-saving options, and being mindful of hidden fees, individuals can ensure their final arrangements are both dignified and affordable. Taking these steps not only protects personal finances but also eases the burden on loved ones during a difficult time.

Why Insurance Companies Issue Debt: Financial Strategies Explained

You may want to see also

Explore related products

![]()

Pre-Need Funeral Plans Overview

Health insurance typically does not cover burial expenses, leaving families to navigate funeral costs independently during an already difficult time. This gap in coverage has given rise to pre-need funeral plans, a proactive approach to managing end-of-life expenses. These plans allow individuals to pre-arrange and pre-pay for their funeral services, ensuring their wishes are honored and alleviating financial burdens on loved ones. By locking in current prices, pre-need plans also protect against inflation, which can significantly increase funeral costs over time.

Consider the steps involved in setting up a pre-need funeral plan. First, research reputable funeral homes or providers that offer these plans. Next, consult with a funeral director to discuss your preferences, from burial or cremation to specific services or memorials. Once you’ve finalized the details, you’ll enter into a contract and choose a payment method, whether a lump sum or installments. It’s crucial to review the plan’s terms, including refund policies and portability, to ensure it aligns with your needs. For instance, some plans allow transfers to different funeral homes if you relocate.

One of the key advantages of pre-need funeral plans is their ability to provide peace of mind. Knowing that your arrangements are in place can relieve emotional and financial stress for your family. Additionally, these plans often include legal protections, such as placing funds in a trust or insurance policy, ensuring they are used solely for funeral expenses. However, it’s essential to verify the provider’s credibility and check for any hidden fees or limitations. For example, some plans may not cover additional costs like cemetery fees or transportation, so clarify all inclusions upfront.

Comparing pre-need funeral plans to other options highlights their unique benefits. Unlike life insurance, which provides a lump sum to beneficiaries, pre-need plans are specifically tailored to cover funeral expenses. They also differ from final expense insurance, which may offer insufficient coverage for comprehensive funeral services. Pre-need plans stand out for their customization and direct application to funeral costs, making them a practical choice for those seeking control over their end-of-life arrangements.

In conclusion, pre-need funeral plans offer a structured, forward-thinking solution to the question of whether health insurance covers burial. By planning ahead, individuals can secure their funeral arrangements, protect against rising costs, and spare their families from additional stress. While health insurance remains focused on medical expenses, pre-need plans fill a critical gap, ensuring that end-of-life wishes are both honored and affordable.

Does VA Health Insurance Cover ER Visits? What Veterans Need to Know

You may want to see also

Explore related products

![]()

Government Assistance for Burial Costs

Health insurance typically does not cover burial costs, leaving many families scrambling to manage funeral expenses during an already difficult time. Fortunately, government assistance programs can provide a financial safety net for those who qualify. These programs vary by country and region, but they generally aim to alleviate the financial burden of burial or cremation for low-income individuals and families. Understanding the available options and eligibility criteria is crucial for accessing this support.

In the United States, for example, the Social Security Administration (SSA) offers a lump-sum death benefit of $255 to eligible survivors. While this amount may seem modest, it can help offset some funeral expenses. To qualify, the deceased must have worked long enough under Social Security, and the benefit is payable only to a spouse or child who meets specific criteria. Additionally, some states have their own burial assistance programs, often administered through local social services or public health departments. These programs may provide direct financial aid or connect families with affordable funeral providers.

Another avenue for government assistance is through federal programs like Temporary Assistance for Needy Families (TANF) or Supplemental Security Income (SSI). While not specifically designed for burial costs, these programs can sometimes allocate funds for funeral expenses if they are deemed essential. Veterans and their families may also qualify for burial benefits through the Department of Veterans Affairs (VA), which includes a burial allowance, a plot allowance, and a headstone or marker. These benefits can significantly reduce out-of-pocket costs for eligible individuals.

To navigate these programs effectively, families should gather necessary documentation, such as proof of income, death certificates, and identification. Applying for assistance promptly is key, as some programs have strict deadlines. For instance, the SSA death benefit must be claimed within two years of the deceased’s passing. Additionally, reaching out to local social service agencies or nonprofit organizations can provide further guidance and support. While government assistance may not cover all burial costs, it can offer much-needed relief during a challenging time.

Comparatively, countries like the UK and Canada also have government schemes to assist with funeral costs. In the UK, the Funeral Expenses Payment can help low-income individuals cover burial or cremation expenses, while Canada’s Last Post Fund provides financial support for veterans’ funerals. These international examples highlight the global recognition of the need for such assistance. By exploring available resources and acting swiftly, families can mitigate the financial strain of burial costs and focus on honoring their loved ones.

Understanding Medical Insurance Caps: Are There Limits to Coverage?

You may want to see also

Frequently asked questions

No, health insurance does not cover burial expenses. Health insurance is designed to cover medical costs, not funeral or burial-related expenses.

Yes, burial insurance or final expense insurance is specifically designed to cover burial and funeral costs. These policies provide a lump sum to beneficiaries to handle such expenses.

Yes, life insurance can be used to cover burial expenses. The death benefit from a life insurance policy can be allocated by beneficiaries to pay for funeral and burial costs.

No, Medicare and Medicaid do not cover burial costs. They are health insurance programs focused on medical care, not funeral or burial expenses.

You can plan for burial expenses by purchasing burial insurance, setting up a savings account, or pre-paying for funeral arrangements directly with a funeral home.