Health insurance is a vital component of financial planning, but many individuals are uncertain about its coverage when it comes to critical illnesses. Critical illnesses, such as cancer, heart attacks, or strokes, often require extensive medical treatment and can lead to significant financial strain. While standard health insurance policies typically cover hospitalization, surgeries, and routine medical expenses, their scope may not extend to the comprehensive needs of critical illness patients, including specialized treatments, long-term care, or loss of income during recovery. This raises the question: does health insurance adequately cover critical illness, or are additional safeguards, such as critical illness insurance, necessary to ensure financial protection during life-threatening health events? Understanding the nuances of coverage is essential for making informed decisions about one's healthcare and financial security.

Explore related products

What You'll Learn

![]()

Types of Critical Illnesses Covered

Critical illnesses are severe health conditions that can have a profound impact on an individual's life, often requiring extensive medical treatment and long-term care. Health insurance policies that cover critical illnesses typically include a predefined list of conditions, ensuring financial protection during life-altering health events. Here's an overview of the types of critical illnesses commonly covered:

Life-Threatening Diseases: These are often at the top of the list for critical illness coverage. Major cancers, such as invasive breast, prostate, or lung cancer, are frequently included. For instance, a policy might cover stage 3 or 4 cancers, requiring specific treatments like chemotherapy or radiation therapy. Similarly, heart attacks and strokes are common critical illnesses, with coverage extending to the acute event and subsequent rehabilitation.

Organ-Specific Conditions: Certain insurance plans provide coverage for organ-related critical illnesses. This could include kidney failure requiring dialysis or a transplant, liver cirrhosis, or major organ transplants like heart, lung, or bone marrow transplants. For example, a policy might offer a lump-sum payment upon the diagnosis of end-stage renal disease, enabling the insured to access specialized care and manage the high costs of treatment.

Neurological Disorders: Some critical illness policies extend their coverage to severe neurological conditions. This may encompass diseases like Alzheimer's or Parkinson's, which are progressive and can significantly impact an individual's quality of life. Additionally, coverage for major head traumas or severe brain injuries resulting from accidents might be included, providing financial support during the recovery process.

Infectious Diseases: While less common, certain critical illness insurance plans may cover specific infectious diseases. For instance, some policies might include coverage for HIV/AIDS, providing financial assistance for antiretroviral therapy and ongoing medical care. Other infectious diseases like meningitis or severe cases of COVID-19 could also be considered critical illnesses, especially if they lead to long-term complications.

When considering health insurance with critical illness coverage, it's essential to review the policy's fine print. Each insurance provider may have different definitions and criteria for what constitutes a critical illness. Understanding the specific conditions covered, the severity required for a claim, and any exclusions is crucial. This ensures that individuals can make informed decisions about their health coverage and be prepared for potential medical emergencies.

Industrial Accident Insurance: Protecting Your Business and Employees

You may want to see also

Explore related products

![]()

Policy Exclusions and Limitations

Health insurance policies often tout comprehensive coverage, but critical illness riders or standalone plans come with fine print that can significantly impact your financial security. Understanding policy exclusions and limitations is crucial, as these clauses dictate what illnesses are covered, under what circumstances, and to what extent. For instance, a policy might cover cancer but exclude early-stage cancers or specific types like skin cancer (non-melanoma). Similarly, heart attacks may be covered only if they meet certain clinical definitions, such as requiring hospitalization for 24 hours or more. These exclusions are not merely technicalities—they can determine whether you receive a payout when you need it most.

Consider the waiting period, a common limitation in critical illness policies. Most plans require a 30- to 90-day waiting period before coverage begins, during which any diagnosed critical illness will not be eligible for a claim. Additionally, survival periods are often mandated, meaning you must survive a specified period (e.g., 30 days) after diagnosis to receive the benefit. For example, if you’re diagnosed with a stroke but pass away within 30 days, your beneficiaries may not receive the payout. These limitations highlight the importance of reading the policy document carefully and asking pointed questions during the purchase process.

Pre-existing conditions are another significant exclusion in critical illness coverage. Insurers typically define a pre-existing condition as any illness or symptom for which you’ve received medical advice, diagnosis, or treatment within a specified period (often 2–5 years) before the policy start date. For instance, if you’ve had high blood pressure for years and later suffer a heart attack, the insurer may deny the claim if they deem the heart attack related to your pre-existing condition. Some policies offer coverage for pre-existing conditions after a waiting period (e.g., 2–4 years), but this varies widely, making it essential to compare plans meticulously.

Age and lifestyle-related exclusions also play a critical role in policy limitations. Many critical illness plans have a maximum entry age, often around 60–65 years, beyond which coverage is unavailable or severely restricted. Smokers and individuals with high-risk occupations or hobbies may face higher premiums or specific exclusions. For example, a smoker diagnosed with lung cancer might find their claim denied if the policy excludes smoking-related illnesses. Similarly, extreme sports enthusiasts could be excluded from coverage for injuries sustained during activities like skydiving or rock climbing. Tailoring your policy to your lifestyle and health profile is key to avoiding unpleasant surprises.

Finally, the scope of coverage for specific illnesses can vary dramatically between policies. While most plans cover major conditions like cancer, heart attack, and stroke, the definitions and severity thresholds differ. For instance, some policies cover only advanced-stage cancers, while others include early-stage diagnoses. Kidney failure might be covered only if it requires dialysis or a transplant. To navigate these nuances, create a checklist of your priorities and cross-reference them with policy details. Consulting an insurance advisor can provide clarity, but ultimately, the onus is on you to ensure the policy aligns with your needs. Ignoring these exclusions and limitations could leave you underinsured when facing a critical illness.

Step-by-Step Guide to Applying for Aetna Health Insurance Coverage

You may want to see also

Explore related products

![]()

Claim Process and Documentation

Health insurance policies often include critical illness coverage, but the claim process can be intricate, requiring meticulous documentation to ensure a smooth experience. Understanding the steps involved is crucial for policyholders to navigate this process effectively.

The Claim Journey: A Step-by-Step Guide

- Notification: Upon diagnosis of a critical illness, promptly inform your insurance provider. Most companies have a dedicated claims department or a specific process for critical illness claims. Timely notification is essential, as delays may impact the claim's outcome.

- Claim Form and Medical Reports: Obtain and carefully fill out the critical illness claim form. This document is typically detailed, requiring information about the diagnosis, treatment plans, and medical history. Accompanying medical reports, including test results, doctor's notes, and treatment summaries, are vital. Ensure these reports are comprehensive and up-to-date.

- Additional Documentation: Depending on the illness and policy terms, insurers may request further evidence. This could include specialist consultations, hospital discharge summaries, or proof of specific treatments like chemotherapy cycles or surgical procedures. For instance, a cancer diagnosis might require details of the stage, type, and treatment protocol, including the number of chemotherapy sessions completed.

Cautions and Common Pitfalls

- Incomplete or inaccurate documentation is a frequent issue. Double-check all forms and ensure medical reports are legible and include all necessary details.

- Be mindful of policy exclusions and waiting periods. Some policies may not cover pre-existing conditions or have specific waiting periods before critical illness coverage becomes effective.

- Keep a record of all communication with the insurance company, including dates, names of representatives, and discussion summaries. This can be invaluable if disputes arise.

Streamlining the Process

To expedite the claim, consider the following:

- Maintain a personal health record, especially if you have a family history of critical illnesses. This can provide quick access to relevant medical information.

- Understand your policy's definition of critical illnesses and the required documentation for each. For instance, a heart attack claim might need details of enzyme levels (e.g., troponin values) and ECG reports.

- In the case of a critical illness, focus on gathering the necessary documents early in the treatment process to avoid last-minute hassles.

The Role of Policy Clarity

Policyholders should advocate for transparent and detailed policy documents. Clear definitions of covered critical illnesses, required documentation, and claim procedures empower individuals to take control of their claims. Insurers should provide accessible resources and guidance, ensuring policyholders understand their rights and responsibilities. This transparency fosters trust and reduces the stress associated with claiming during an already challenging time.

In summary, a successful critical illness claim relies on a proactive approach to documentation and a thorough understanding of policy requirements. By following a structured process and being vigilant about details, policyholders can navigate this complex journey with greater confidence.

Ohio State Medical Center: Accepted Insurance Options

You may want to see also

Explore related products

![]()

Waiting Periods and Payout Terms

Critical illness coverage often includes a waiting period, typically 30 to 90 days, during which a diagnosis must survive for a claim to be valid. This survival period ensures the policyholder is truly facing a life-altering condition, reducing the risk of fraudulent claims. For example, if you’re diagnosed with a heart attack, you must live beyond the specified waiting period (e.g., 30 days) to qualify for a payout. This clause protects insurers but also underscores the importance of understanding policy terms before purchasing.

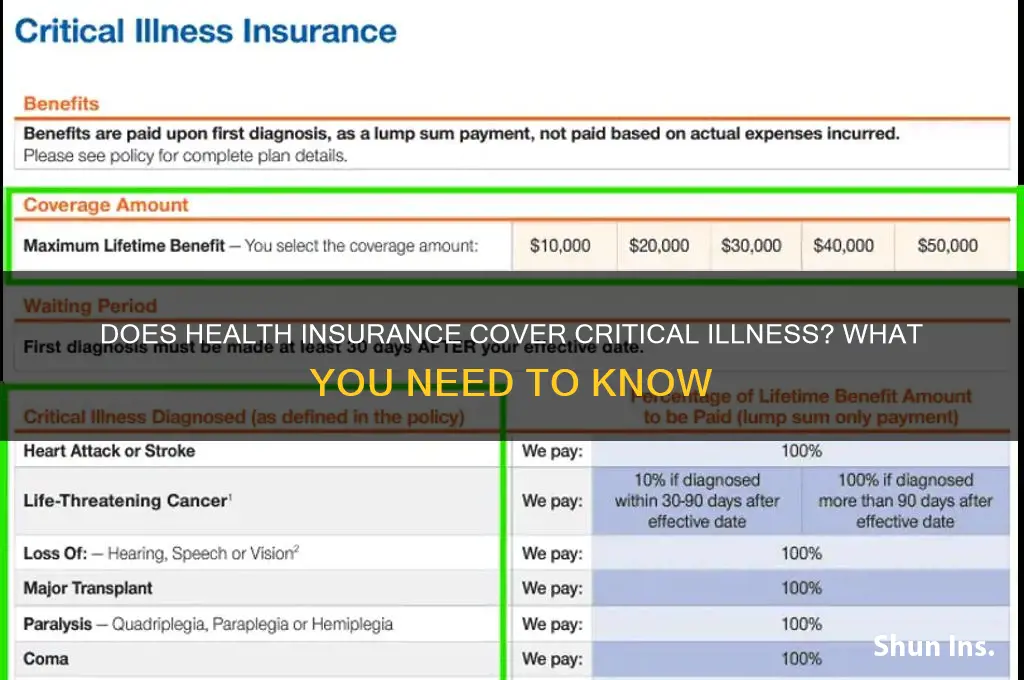

Payout terms vary widely across critical illness plans, with lump-sum payments being the most common. The amount, often ranging from $10,000 to $100,000, is paid directly to the policyholder, not tied to medical expenses. This flexibility allows individuals to use the funds for recovery costs, lost income, or even debt repayment. However, some policies may cap payouts for specific illnesses or age groups. For instance, a 40-year-old might receive the full amount for cancer, while a 65-year-old could receive only 50% due to age-related risk adjustments.

A lesser-known aspect is the partial payout clause, which applies if the illness doesn’t meet the full criteria but qualifies for a reduced benefit. For example, early-stage cancer might trigger a 25% payout, while advanced stages result in 100%. This tiered approach encourages early detection while providing financial support regardless of the illness’s severity. Policyholders should review these terms carefully, as they significantly impact the overall value of the coverage.

Finally, exclusions and limitations in payout terms can render a policy ineffective in certain scenarios. Pre-existing conditions, self-inflicted injuries, or illnesses resulting from hazardous activities (e.g., extreme sports) are often excluded. Additionally, some policies require the illness to be diagnosed by a specialist or within a specific timeframe. For instance, a stroke diagnosed within 7 days of symptoms may qualify, but one diagnosed after 14 days might not. Understanding these nuances ensures you’re not caught off guard when filing a claim.

Smoking's Impact on Health Insurance: Costs, Coverage, and Consequences

You may want to see also

Explore related products

![]()

Add-Ons vs. Standalone Critical Illness Plans

Critical illness coverage often leaves policyholders weighing the merits of add-ons versus standalone plans. Add-ons, typically attached to existing health insurance policies, offer a cost-effective way to include critical illness benefits without purchasing a separate plan. For instance, a 35-year-old non-smoker might add critical illness coverage to their base health plan for an additional $20–$50 monthly, depending on the insurer and coverage amount. This option is ideal for those seeking basic protection without the complexity of managing multiple policies. However, the trade-off lies in limited customization and lower coverage caps, often ranging from $10,000 to $50,000, which may not fully offset the financial burden of a severe illness.

Standalone critical illness plans, on the other hand, provide tailored, comprehensive coverage designed specifically for high-impact conditions like cancer, heart attack, or stroke. These plans often feature higher payout limits, starting at $50,000 and going up to $500,000 or more, depending on the policyholder’s age, health, and chosen coverage level. For example, a 45-year-old with a family history of heart disease might opt for a $250,000 standalone plan, paying $100–$200 monthly for peace of mind. While more expensive than add-ons, standalone plans offer flexibility, such as lump-sum payouts, shorter waiting periods, and coverage for specific stages of illnesses (e.g., early-stage cancer).

Choosing between the two requires a practical assessment of needs and budget. Add-ons are suitable for individuals with limited financial flexibility or those who view critical illness coverage as a secondary safeguard. Conversely, standalone plans appeal to those prioritizing robust protection, especially if they have a higher risk profile due to genetics, lifestyle, or occupation. For instance, a smoker in their 50s might find a standalone plan more beneficial, given their elevated risk of critical illnesses.

A key caution is to scrutinize policy terms, as both options may exclude pre-existing conditions or impose waiting periods before benefits become active. Additionally, standalone plans often require medical underwriting, which can affect premiums or eligibility. Practical tips include comparing multiple insurers, using online calculators to estimate costs, and consulting a financial advisor to align coverage with long-term goals. Ultimately, the decision hinges on balancing affordability with the level of protection needed to navigate the financial challenges of a critical illness.

Why Mortgage Insurers Demand Case Numbers: Understanding the Requirement

You may want to see also

Frequently asked questions

No, standard health insurance plans typically do not automatically cover critical illnesses. Critical illness coverage is usually an add-on or a separate policy that provides a lump-sum payment upon diagnosis of specific severe conditions like cancer, heart attack, or stroke.

Critical illness coverage generally includes major conditions such as cancer, heart attack, stroke, organ transplants, kidney failure, and paralysis. The specific illnesses covered vary by policy and insurer, so it’s important to review the terms carefully.

Yes, the lump-sum payout from critical illness insurance can be used for any purpose, such as medical bills, daily expenses, or debt repayment. It provides financial flexibility during a challenging time, allowing you to focus on recovery rather than finances.