Health insurance coverage for extreme sports is a critical consideration for enthusiasts who engage in high-risk activities such as skydiving, rock climbing, or white-water rafting. While standard health insurance policies typically cover medical expenses resulting from everyday accidents and illnesses, they often exclude injuries sustained during extreme sports due to the elevated risk involved. Some insurers may offer specialized plans or riders that provide coverage for these activities, but these usually come with higher premiums or specific exclusions. Understanding the terms of your policy and exploring options tailored to your lifestyle is essential to ensure adequate protection while pursuing adrenaline-fueled adventures.

| Characteristics | Values |

|---|---|

| Coverage for Extreme Sports | Varies by policy and provider; some insurers exclude extreme sports entirely, while others offer limited coverage or require additional premiums. |

| Common Exclusions | Activities like skydiving, rock climbing, bungee jumping, scuba diving, and BASE jumping are often excluded from standard health insurance policies. |

| Specialized Policies | Some insurers offer specialized policies or riders that cover extreme sports, but these typically come with higher premiums and specific conditions. |

| Pre-Existing Conditions | Injuries sustained while participating in extreme sports may be considered pre-existing conditions, affecting future claims or coverage. |

| Geographic Restrictions | Coverage may be limited or excluded for extreme sports activities performed in certain high-risk locations or countries. |

| Medical Evacuation | Some policies may cover emergency medical evacuation during extreme sports accidents, but this is not standard. |

| Disability and Life Insurance | Extreme sports participants may face higher premiums or exclusions for disability and life insurance policies. |

| Travel Insurance | Travel insurance policies may cover extreme sports, but coverage limits and exclusions vary widely; always check policy details. |

| Disclosure Requirement | Insurers often require policyholders to disclose participation in extreme sports, which may affect premiums or coverage eligibility. |

| Claim Denial Risk | Claims related to injuries from extreme sports are at higher risk of denial if the activity was not disclosed or is explicitly excluded. |

Explore related products

What You'll Learn

![]()

Coverage for skydiving accidents

Skydiving accidents, while rare, can result in severe injuries such as fractures, spinal damage, or traumatic brain injuries. Health insurance policies often exclude coverage for injuries sustained during high-risk activities like skydiving, classifying them as "hazardous recreational activities." Before assuming your plan will cover skydiving-related injuries, carefully review the exclusions section of your policy. Look for specific language mentioning parachuting, aerial sports, or extreme activities. If excluded, the financial burden of medical treatment—which can range from $10,000 for a minor injury to over $100,000 for critical care—falls entirely on you.

To bridge this coverage gap, consider purchasing specialized insurance tailored to skydiving. Companies like the United States Parachute Association (USPA) offer policies that cover medical expenses, emergency evacuations, and even liability claims. These plans typically cost between $100 and $300 annually, depending on coverage limits and deductibles. For instance, a USPA policy might provide up to $250,000 in medical coverage with a $1,000 deductible. If you’re an occasional skydiver, opt for a short-term policy covering specific jumps rather than an annual plan.

Even with specialized insurance, prevention remains the best strategy. Ensure you’re jumping with a certified instructor, using properly maintained equipment, and adhering to safety protocols. For example, always perform a gear check before each jump and avoid skydiving in adverse weather conditions. Additionally, maintain a good level of physical fitness, as stronger muscles and better coordination can reduce the risk of injury during landing.

Comparatively, some health insurance providers may offer partial coverage if the injury is deemed accidental rather than a direct result of skydiving. For example, if you suffer a heart attack during a jump, your health insurance might cover treatment for the cardiac event but not the injuries sustained from the fall. However, this is rare and depends on the insurer’s interpretation of policy terms. To maximize your chances of coverage, document the incident thoroughly, including witness statements and medical records, and consult with an insurance attorney if your claim is denied.

In conclusion, while health insurance typically excludes skydiving accidents, proactive steps like purchasing specialized coverage and adhering to safety measures can mitigate financial and physical risks. Treat skydiving insurance as an essential investment, not an optional add-on, and always prioritize prevention over reaction. By doing so, you can enjoy the thrill of the sport with greater peace of mind.

Understanding Medical Insurance Coverage During Unemployment

You may want to see also

Explore related products

$19.49 $29.99

$29.99 $32.99

![]()

Rock climbing injury policies

Rock climbing, with its inherent risks of falls, fractures, and soft tissue injuries, demands specialized insurance coverage. Standard health insurance policies often exclude or limit coverage for injuries sustained during high-risk activities like climbing. This leaves climbers vulnerable to significant out-of-pocket expenses in the event of an accident.

A dedicated rock climbing injury policy bridges this gap, offering tailored protection for climbers of all levels. These policies typically cover medical expenses related to climbing-specific injuries, including emergency evacuation from remote locations, a common necessity in outdoor climbing scenarios.

Consider a scenario: a climber experiences a severe ankle fracture while bouldering. Standard health insurance might cover basic treatment, but a specialized policy could provide additional benefits like coverage for physical therapy specifically tailored to climbing recovery, ensuring a return to the sport. Some policies even offer income protection if the injury results in temporary inability to work.

When selecting a rock climbing injury policy, carefully review the fine print. Pay close attention to exclusions, coverage limits, and definitions of "rock climbing." Some policies may exclude certain disciplines like ice climbing or high-altitude mountaineering. Additionally, consider your climbing frequency and experience level, as these factors can influence premiums.

For instance, a weekend warrior tackling indoor climbing walls may require less comprehensive coverage than a professional climber scaling multi-pitch routes in remote locations. Ultimately, investing in a rock climbing injury policy is a proactive decision that prioritizes both your health and your passion for the sport. It provides peace of mind, allowing you to focus on the climb, not the potential financial consequences of an accident.

Does Farm Bureau Offer Health Insurance? Exploring Coverage Options

You may want to see also

Explore related products

$19.71 $29.99

![]()

Scuba diving medical exclusions

Scuba diving, while exhilarating, carries inherent risks that can trigger medical exclusions in health insurance policies. Insurers often view it as an extreme sport due to the potential for decompression sickness, arterial gas embolism, and other diving-related injuries. These conditions require specialized treatment, such as hyperbaric oxygen therapy, which can be costly. As a result, many standard health insurance plans exclude coverage for injuries sustained while scuba diving, leaving divers financially vulnerable.

To navigate these exclusions, divers must scrutinize their insurance policies for specific clauses related to high-risk activities. Some policies may offer partial coverage for diving-related injuries but exclude complications like decompression sickness. Others might require additional premiums for a rider that explicitly covers scuba diving. For instance, a policy might cover emergency room visits but exclude the hyperbaric chamber treatment often needed for diving accidents. Understanding these nuances is critical to avoiding unexpected out-of-pocket expenses.

Age and certification level can also influence coverage. Insurers may impose stricter exclusions for divers over 50 or those without advanced certifications, as they are statistically at higher risk. For example, a 55-year-old diver with only an Open Water certification might face broader exclusions compared to a 30-year-old with a Rescue Diver certification. Divers in higher-risk categories should consider specialized dive accident insurance, which typically covers medical expenses, evacuation, and repatriation, regardless of their primary health insurance policy.

Practical steps to mitigate exclusion risks include maintaining detailed dive logs and staying within certification limits. Dive logs can serve as evidence of responsible diving practices, potentially influencing insurers’ decisions in case of a claim. Additionally, divers should undergo regular medical check-ups to ensure they meet the physical requirements for diving, reducing the likelihood of accidents that could trigger exclusions. Combining these strategies with the right insurance coverage ensures that the thrill of scuba diving isn’t overshadowed by financial uncertainty.

Medical Insurance Coverage for Chicken Pox Testing Explained

You may want to see also

Explore related products

![]()

Base jumping insurance limits

Base jumping, a sport that involves leaping from fixed structures and deploying a parachute, carries an inherent risk that few activities can match. This extreme sport’s fatality rate is estimated at 1 in 2,317 jumps, making it a high-stakes pursuit. For participants, understanding insurance coverage is critical, as standard health insurance policies often exclude high-risk activities like base jumping. Most insurers classify it as an "excluded activity," meaning injuries sustained during a jump may not be covered under your policy. This leaves base jumpers with limited options: either self-insure, which is financially perilous, or seek specialized policies designed for extreme sports enthusiasts.

Specialized insurance for base jumpers exists but comes with strict limits and conditions. Policies typically cap coverage amounts, often ranging from $50,000 to $250,000, depending on the provider and the jumper’s experience level. Premiums are significantly higher than standard health insurance, reflecting the elevated risk. Additionally, insurers may require proof of certification, a minimum number of logged jumps, or adherence to safety protocols, such as jumping with a backup parachute. Some policies exclude coverage for jumps from certain heights or locations deemed excessively dangerous, further narrowing the scope of protection.

For those considering base jumping, the financial implications of an injury cannot be overstated. A single accident can result in medical bills exceeding $100,000, including emergency care, surgery, and rehabilitation. Without adequate insurance, these costs fall entirely on the individual. To mitigate risk, jumpers should carefully review policy exclusions and consider supplemental coverage, such as disability or life insurance. Joining organizations like the United States Base Association (USBA) can also provide access to group insurance plans with more favorable terms.

Comparatively, base jumping insurance is less accessible and more restrictive than coverage for other extreme sports, such as skydiving or rock climbing. While skydiving is often covered under specialized policies with fewer limitations, base jumping’s higher fatality rate makes insurers more cautious. This disparity highlights the importance of researching and comparing policies tailored to your specific activity. For base jumpers, the takeaway is clear: standard health insurance is insufficient, and specialized coverage, though expensive and limited, is a necessary investment in personal safety and financial security.

Finally, a practical tip for base jumpers is to document every jump meticulously. Maintaining a detailed log of jumps, including dates, locations, and equipment used, can strengthen your case when applying for insurance or filing a claim. Some insurers may also offer discounts or higher coverage limits to jumpers with a proven track record of safe practices. While no insurance policy can eliminate the risks of base jumping, informed decisions and proactive measures can minimize the financial fallout of an accident.

Best Insurance Providers for Sprint Phones: Top Companies Compared

You may want to see also

Explore related products

![]()

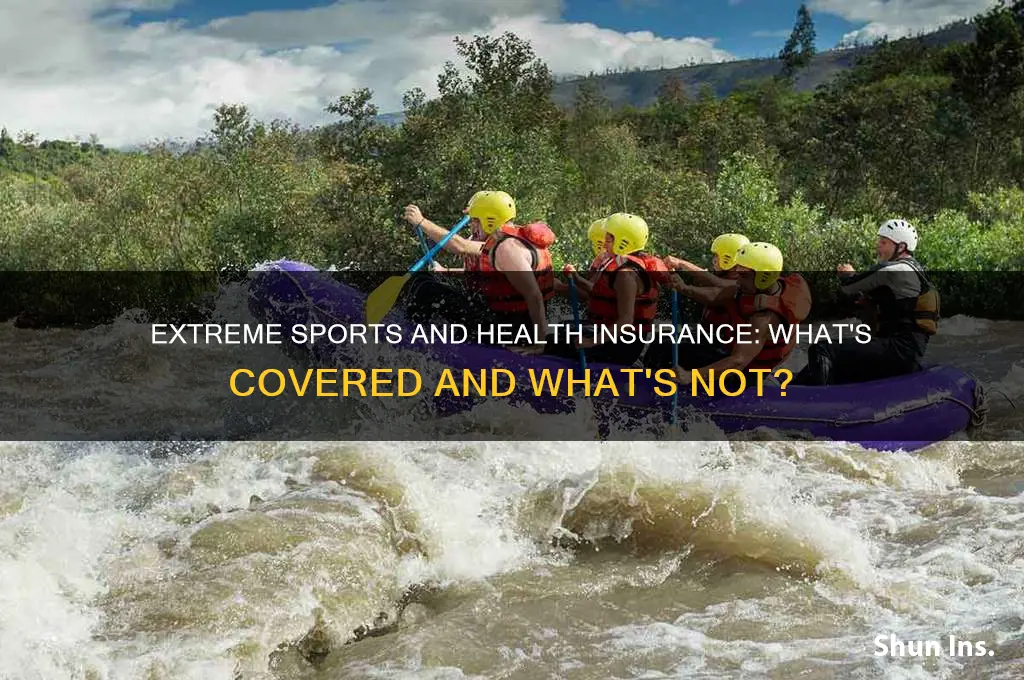

Whitewater rafting claim eligibility

Whitewater rafting, with its adrenaline-pumping rapids and unpredictable currents, is undeniably an extreme sport. But what happens when the thrill turns into a spill? Understanding whether your health insurance covers injuries sustained during such activities is crucial. Most standard health insurance policies exclude high-risk sports due to their increased likelihood of injury. Whitewater rafting often falls into this category, leaving enthusiasts vulnerable to out-of-pocket medical expenses. Before embarking on your next river adventure, scrutinize your policy’s exclusions and consider supplemental coverage options like adventure sports riders or specialized travel insurance.

To determine claim eligibility for whitewater rafting injuries, start by identifying the specific activities covered under your policy. Some insurers differentiate between rafting grades, with Class I-III rapids potentially covered under standard plans, while Class IV-V rapids may require additional coverage. Documenting the rafting trip details, such as the river difficulty level and safety measures taken, can strengthen your claim. For instance, if you wore a certified life jacket and helmet, insurers may view your case more favorably, as these precautions demonstrate a commitment to risk mitigation.

A common pitfall in whitewater rafting claims is the assumption that all injuries are automatically covered. Insurers often investigate whether negligence or disregard for safety guidelines contributed to the incident. For example, rafting without a licensed guide or ignoring weather warnings could void your claim. To avoid this, adhere strictly to safety protocols and ensure all equipment is in optimal condition. Additionally, keep records of any safety briefings or certifications obtained, as these can serve as evidence of responsible participation.

If your health insurance explicitly excludes whitewater rafting, explore alternative coverage options. Adventure sports riders, available as add-ons to existing policies, can fill this gap. Travel insurance with extreme sports coverage is another viable option, especially for international rafting trips. When comparing plans, pay attention to coverage limits, deductibles, and pre-existing condition clauses. For instance, a policy with a $10,000 coverage limit may suffice for minor injuries but fall short for severe trauma requiring hospitalization. Always read the fine print to ensure the policy aligns with your rafting habits and risk tolerance.

In conclusion, whitewater rafting claim eligibility hinges on policy specifics, safety adherence, and supplemental coverage. Proactive measures, such as reviewing exclusions and investing in additional insurance, can safeguard your financial well-being. Remember, the goal is not just to enjoy the rapids but to navigate the aftermath with confidence, knowing you’re protected.

Are Part D Costs Tax-Deductible for Health Insurance Businesses?

You may want to see also

Frequently asked questions

Health insurance coverage for extreme sports injuries varies by policy. Some plans may cover injuries, but many exclude high-risk activities like skydiving, rock climbing, or bungee jumping. Always check your policy’s exclusions or consider supplemental coverage.

Yes, some insurers offer specialized plans or riders that cover extreme sports. These plans often come with higher premiums due to the increased risk. Research providers that cater to adventure enthusiasts.

If your policy excludes extreme sports, consider purchasing separate accident insurance or a specialized extreme sports insurance plan. These policies can help cover medical expenses, evacuation, or other costs related to injuries.

Pre-existing conditions may impact your eligibility for extreme sports coverage or result in higher premiums. Insurers often assess risk based on your health history, so disclose all conditions when applying for coverage.